Summary (10 bullet points)

- Korea ETFs are among the world’s most sensitive equity markets to TNX movements.

- The reason isn’t “just because Korea has many tech stocks.”

- Korea’s ETF structure is unusually concentrated in semiconductors, internet, and battery growth sectors.

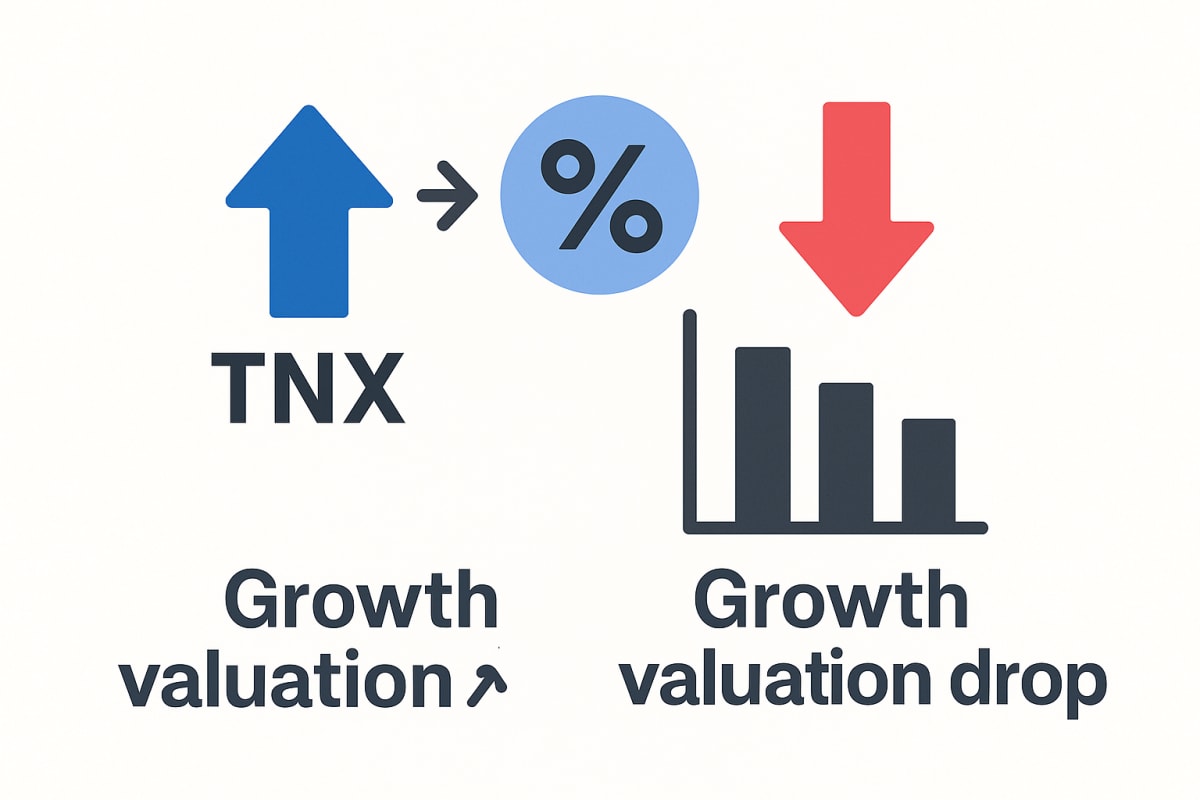

- When TNX rises, discount rates surge → growth valuations contract → ETFs fall sharply.

- TNX ↑ usually triggers USD strength → KRW weakness → foreign outflows.

- Korea is one of the most FX-sensitive markets due to extremely high export dependency.

- Foreign investors hold a large share of KOSPI, making KRW volatility a direct ETF risk factor.

- Korea is classified as MSCI EM, so global liquidity cycles hit faster and harder.

- Semiconductor cycle volatility amplifies the response to TNX/FX shifts.

- Conclusion: Korea ETFs = TNX + USD + KRW + Semiconductor cycle (all must be analyzed together).

Korea ETF movements follow a chain reaction: TNX → USD → KRW → Foreign flows → Growth valuation → ETF performance.

1. Introduction — “Why does Korea fall harder than the U.S.?”

Many investors wonder:

“Why do Korean ETFs drop more than the U.S. when TNX rises?”

The answer is structural, not emotional.

Korea ETFs have several built-in sensitivities:

- Very high growth-stock concentration (semiconductors, internet, EV batteries)

- Extremely strong FX dependency (export-driven economy)

- Foreign ownership controlling market direction

- MSCI EM classification → passive flows react to USD liquidity

- Semiconductor-centric profit model

In short: Korea ETFs are a triple-levered play on global rates, FX, and growth cycles.

2. “It’s not sentiment. It’s structure.”

Korea ETFs = High Growth + High FX Sensitivity + High Foreign Ownership

Korea’s ETF volatility is not a coincidence. TNX moves affect discount rates, USD strength, KRW levels, and foreign capital flows — all of which directly determine ETF performance.

Top 4 Sensitivity Drivers

- Extreme growth-stock concentration

- High FX (USD/KRW) dependency

- Foreign ownership dominance

- Semiconductor cycle volatility

3. Structural Breakdown: Why Korea is uniquely growth-heavy

3-1. KOSPI = Semiconductor-dominated growth market

Korea’s top market-cap companies share common traits:

- Future cash flows dominate valuation

- Sensitive to global demand + export cycles

- Highly sensitive to discount rate changes

Even a 0.1% rise in TNX can meaningfully contract valuations.

3-2. Korea vs U.S. vs Japan vs Europe

| Country | Major Sectors | Rate Sensitivity | Volatility |

|---|---|---|---|

| U.S. | IT + Financials + Healthcare | Medium | Low |

| Japan | Autos + Manufacturing | Low | Low |

| Europe | Financials + Industrials | Low | Medium |

| Korea | Semiconductors + Internet + EV Batteries | Very High | Very High |

This is why TNX becomes a direct directional signal for Korea ETFs.

4. “Why Korea reacts harder to rising TNX”

TNX Rising → Negative for Korea ETFs

- Growth-stock valuation pressure

- USD strength → KRW weakness

- Foreign investor outflows

- MSCI EM passive selling

TNX Falling → Positive for Korea ETFs

- Growth valuation recovery

- KRW appreciation → foreign inflows

- Semiconductor cycle optimism

- Lower liquidity risk premium

5. Callout — Essential Insight

6. Three visual pillars of Korea ETF sensitivity

7. Two essential tables for understanding Korea ETFs

7-1. Growth concentration across major Korea ETFs

| ETF | Growth Exposure | Rate Sensitivity | FX Sensitivity | Volatility |

|---|---|---|---|---|

| KODEX 200 | High | ★★★★★ | ★★★★☆ | High |

| TIGER Secondary Battery | Very High | ★★★★★ | ★★★☆☆ | Very High |

| KODEX Semiconductor | Very High | ★★★★★ | ★★★★☆ | Very High |

| KODEX Leverage | Extreme | ★★★★★ | ★★★★★ | Highest |

7-2. Combined impact of TNX + USD/KRW

| TNX | USD/KRW | Foreign Flow | ETF Direction |

|---|---|---|---|

| ↑ | ↑ | Outflows | Strong decline |

| ↑ | ↓ | Mixed | Sector-dependent |

| ↓ | ↓ | Inflows | Strong rally |

| ↓ | ↑ | Weak | Limited upside |

8. Why foreign flows dominate Korea ETFs

Korea’s foreign ownership is ~30%+ and even higher in large caps.

Thus:

- USD strength → automatic foreign selling

- USD weakness → automatic foreign buying

- Passive funds sell or buy based on MSCI EM weights

- KRW volatility directly changes ETF performance

Therefore, monitoring TNX + USD/KRW is essential for any Korea ETF investor.

9. Checklist — Before investing in Korea ETFs

- Is the ETF growth-heavy?

- Does it include sectors with high rate sensitivity?

- What is its FX exposure?

- How dependent is it on foreign flows?

- Is it in MSCI EM?

- Is it tied to the semiconductor cycle?

- Is global liquidity improving?

- What are TNX, DXY, and KRW doing right now?

10. Conclusion (3 lines)

- Korea ETFs are structurally sensitive to TNX and USD liquidity.

- Growth-heavy concentration amplifies rate shocks.

- TNX·USD·KRW·Semiconductor cycle must be analyzed together for accurate ETF timing.

11. CTA

Compare Korea ETF performance with CAGR

When TNX and FX drive the cycle, annualized returns and disciplined contributions matter more than one-period gains.

Open CAGR CalculatorUseful next reads:

- How U.S. 10Y Yield (TNX) Affects ETFs

- What Is DXY? A Beginner-Friendly Explanation for Investors

- USD/KRW Exchange Rate: What It Means for Korea's Economy and the KOSPI

12. FAQ

Q1. Why are Korea ETFs more volatile than U.S. ETFs?

Because of growth-heavy composition, FX exposure, and foreign ownership.

Q2. Does TNX always cause Korea ETFs to fall?

Mostly, but early tightening cycles sometimes boost financial ETFs.

Q3. Is FX really that important?

Yes. KRW weakness directly triggers foreign selling.

Q4. How important is the semiconductor cycle?

Extremely. Korea’s index is structurally tied to semiconductor earnings.