Summary (10 sentences)

- The S&P 500 is not just an American stock index—it’s a global “risk appetite gauge.”

- Korea’s stock market tends to react strongly because foreign participation is meaningful and capital flows are sensitive to global sentiment.

- When the S&P 500 turns volatile, investors often rotate toward safety, which can strengthen the U.S. dollar.

- A stronger dollar frequently shows up as higher USD/KRW, changing the return profile for foreign investors in Korean assets.

- USD/KRW also impacts corporate earnings channels, especially for export-heavy sectors, but effects vary by cost structure.

- U.S. Treasury yields—often proxied by the 10-year—affect equity valuation via discount rates and growth sensitivity.

- Korea’s index composition (notably semiconductors and tech) amplifies transmission from U.S. tech cycles and global demand narratives.

- “S&P down = KOSPI down” is an oversimplification that hides the real drivers and leads to late decisions.

- The more reliable lens is a three-factor bundle: S&P 500 + USD (USD/KRW, DXY) + U.S. rates (10Y/TNX).

- In practice, the combination—not the S&P move alone—determines whether Korea feels a mild pullback or a sharper shock.

One-paragraph overview

If you invest in Korean equities, the S&P 500 often functions less like “foreign news” and more like a dashboard for global positioning. When U.S. risk appetite shifts, it transmits into Korea through a chain reaction: dollar strength/weakness (USD/KRW), U.S. rates (discount rate pressure), and foreign investor flows (risk budgeting). This post breaks that chain into observable signals, provides scenario tables for faster diagnosis, and ends with a practical checklist you can use when the KOSPI feels “out of sync” with local headlines.

1) Why Korea “feels” U.S. equity moves so strongly

Korea is an open economy and the KOSPI is a globally traded market. That combination makes it naturally sensitive to global risk cycles—especially when positioning shifts quickly. In many episodes, Korea doesn’t move simply because “America moved,” but because global portfolios are rebalancing and Korea sits on the receiving end of that adjustment.

There’s also a structural angle: Korea’s index is heavily tilted toward sectors that sit near the center of global supply chains (semiconductors, hardware, export manufacturing). When the S&P 500 turns because the market is repricing growth, tech, or demand expectations, Korea often absorbs those changes with higher beta.

If you want a broader “dashboard” view of how global indicators interact with Korean markets, this internal post helps frame the big picture:

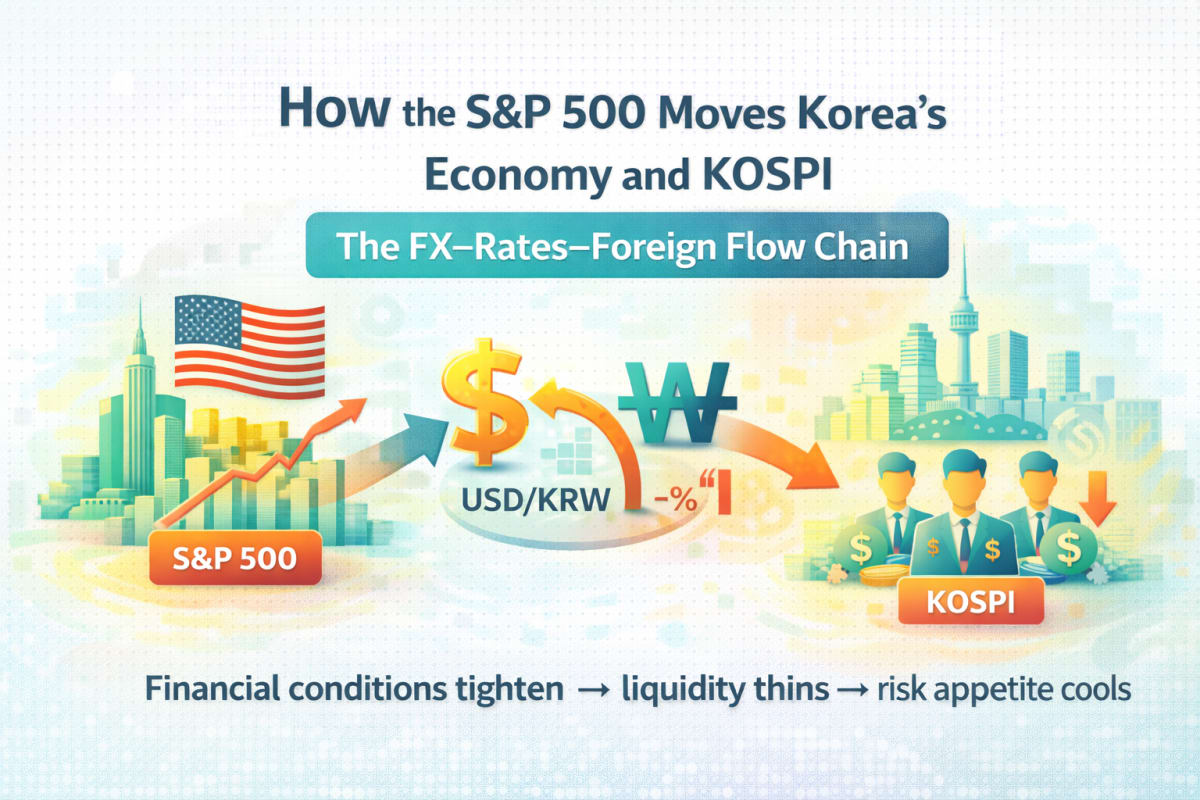

2) Hero Layout: The core mechanism is a 3-step chain

Core framework

The S&P 500 impacts Korea primarily through three connected channels: (1) risk sentiment and global positioning, (2) the U.S. dollar and USD/KRW (which changes foreign investor returns and local financial conditions), and (3) U.S. rates (which move discount rates and valuation sensitivity, especially for growth-heavy segments). The KOSPI tends to suffer most when these channels align in the same direction—risk-off + USD strength + rates pressure.

Three signals to bundle

- S&P 500 = global risk appetite (risk-on / risk-off)

- USD (USD/KRW, DXY) = FX and cross-border flow pressure

- U.S. 10Y / TNX = discount rate and valuation sensitivity

3) Channel A: Risk sentiment → global positioning → KOSPI flow impact

When the S&P 500 trends up smoothly, global portfolios usually tolerate more risk. That can mean higher equity allocation, stronger appetite for cyclical assets, and steadier flows into non-U.S. markets. When the S&P turns sharply lower—especially with rising volatility—investors often shift toward capital preservation and reduce exposure to markets perceived as higher beta.

In Korea, that often shows up as:

- faster changes in foreign investor net buying/selling

- a wider risk premium demanded for holding equities

- “liquidity thinning” episodes where price moves feel exaggerated

This doesn’t mean the KOSPI is “weak.” It means that global flows can dominate local narratives, particularly during transitions (from calm to stress, or vice versa).

If you want a portfolio-level “risk budget” lens (how much equity/bond/FX risk you are implicitly carrying), this connects cleanly to the same framework:

4) Channel B: The dollar and USD/KRW → foreign returns and “financial conditions”

A big reason Korea cares about U.S. risk cycles is that stress often coincides with USD strength. When the dollar strengthens broadly, USD/KRW tends to rise (KRW weakens), which changes the equation for foreign investors:

- Even if Korean stocks hold up in KRW terms, a weaker KRW can reduce returns in USD terms.

- When FX moves are fast, investors may reduce exposure to avoid compounding equity drawdowns with FX losses.

FX also influences corporate profitability—but not uniformly. Export-heavy firms may benefit from a weaker KRW in revenue translation, while cost inflation (imports, components, energy) can offset that benefit. So “KRW weak = exporters up” is not a rule; it’s a hypothesis that depends on margins and pricing power.

If you want a dedicated foundation for reading USD/KRW and its market implications, these internal posts are useful:

If you want a more “investor-useful” extension of this FX channel, link the story to who actually benefits when KRW weakens:

And when FX moves are driven by headline risk (geopolitics/tariffs), USD liquidity and positioning often dominate “export logic.” These two posts connect that mechanism:

- Geopolitics → USD liquidity → FX: why stress can lift the dollar

- Tariffs, growth, margins, and FX: how a policy shock can transmit

5) Channel C: U.S. rates (10Y / TNX) → discount rates → valuation sensitivity

U.S. Treasury yields—especially the 10-year—affect global equity valuation via discount rates. When yields rise, the present value of distant cash flows typically falls, which can pressure growth-heavy segments. Korea’s market composition can amplify this because valuation-sensitive sectors (tech, growth) are a meaningful slice of index performance.

But rate moves need interpretation:

- Rates up because growth is strong can sometimes support cyclicals even as it pressures long-duration growth.

- Rates up because inflation is sticky can tighten conditions and weigh on both growth and risk appetite.

- Rates down because recession fear rises may help discount rates but hurt earnings expectations.

If you want a clean foundation for understanding TNX and how rate mechanics translate into markets, these are helpful:

- TNX explained: why the 10Y yield drives markets

- How interest rates work: from policy rates to loans and bonds

If you want to go one step deeper than “rates up/down” and read the shape of rates (inversion/steepening) without overreacting:

6) The “DXY layer”: why broad USD strength matters for Korea

Sometimes USD/KRW rises due to Korea-specific dynamics, but during global risk events it often moves with the dollar broadly—captured by DXY. Broad USD strength can coincide with tighter global financial conditions, reduced appetite for EM risk, and more cautious cross-border positioning.

When headlines are geopolitical, the market impact often comes through USD liquidity + positioning more than through “who wins” narratives:

7) Table 1 — The transmission map (what to watch, and why)

| Channel | What you often see in KOSPI | Companion indicators | Practical interpretation |

|---|---|---|---|

| Risk sentiment | foreign selling, volatility spikes | S&P 500, volatility | Fast declines often cause “flow shocks” |

| FX / USD | USD/KRW jump amplifies stress | USD/KRW, DXY | FX speed matters more than level short-term |

| U.S. rates | growth-heavy segments pressure | U.S. 10Y / TNX | Rising yields can compress valuations |

| Earnings narrative | sector divergence (export vs domestic) | guidance, cycle data | Separate “flow” from “earnings reprice” |

| Commodities | inflation re-acceleration risk | Oil shock → USD/KRW transmission | Can feed back into rates and USD |

8) Common mistake vs safer framework

Common mistake

- Reacting to the S&P headline alone

- Explaining every KOSPI move as “America did it”

- Ignoring cases where USD and rates diverge

- Overfitting to one news item

Safer framework

- Bundle: S&P 500 + USD/KRW (and DXY) + U.S. 10Y (TNX)

- Separate “speed shock” from “trend reprice”

- Diagnose whether it’s flow-driven or earnings-driven

- Watch sector behavior, not just the index

9) Table 2 — The same S&P pullback can feel very different in Korea

| S&P 500 move | USD/KRW & USD tone | U.S. rates (TNX) | Likely KOSPI “feel” | First things to check |

|---|---|---|---|---|

| Sharp drop | USD strong, KRW weak | yields elevated or rising | heavier flow pressure + valuation stress | FX speed, foreign flows |

| Gradual dip | USD stable or softer | yields falling | can look like “normalization” | rate trend, sector leadership |

| Rally | USD stable | yields stable | supportive risk tone | persistence of foreign buying |

| Rally | USD strong | yields rising | U.S. strong but Korea muted | FX drag vs earnings uplift |

10) Visual Overview

11) A practical diagnostic checklist (9 items)

Use this checklist when KOSPI moves feel “bigger than the news.”

Is the S&P move a fast shock or a slow drift?

Did USD/KRW spike, or is FX stable?

Is DXY strengthening (broad USD strength) or not?

Is TNX rising, falling, or stuck at highs?

Are foreign flows negative in both cash and futures (if you track them)?

Is weakness concentrated in semis/tech, or broad across domestic sectors too?

Is this primarily a flow event or an earnings narrative reset?

Are commodities/energy adding inflation pressure that could push rates up again? (See: oil shock → USD/KRW transmission)

Are you trying to explain everything with a single headline?

12) Table 3 — Classify the episode: flow shock vs rate shock vs earnings reprice

| Type | Typical trigger | Common co-moves | How it feels | Personal investor approach |

|---|---|---|---|---|

| Flow shock | volatility + risk-off | USD/KRW jump, DXY up | fast and heavy | follow pre-set sizing/limits; avoid chasing |

| Rate shock | yields repricing higher | TNX up, growth underperforms | valuation squeeze | reduce “duration” exposure; be patient |

| Earnings reprice | demand/guidance reset | sector divergence | selective pain | focus on margins and cycle sensitivity |

13) Conclusion (3 lines)

- The KOSPI is not a simple mirror of the S&P 500—it is the S&P move filtered through USD, rates, and foreign flows.

- The same U.S. pullback can feel mild or brutal in Korea depending on whether USD strength and rate pressure are present.

- If you bundle S&P 500 + USD/KRW (and DXY) + TNX, your read of Korea’s market gets faster and more consistent.

14) CTA — Plan beats timing (especially for index exposure)

Prefer a rules-based approach?

For index-style investing, “perfect timing” is less reliable than a durable plan. A simple DCA simulation can help you define contribution size and horizon so volatility becomes a process—not a surprise.

Build a monthly DCA plan15) A good piece of writing to read together

- Global market environment that most affects KOSPI (overview)

- How USD/KRW influences Korea and KOSPI

- FX basics: what really moves USD/KRW

- How interest rates work: from policy rates to loans and bonds

- DXY and market impact (stocks, FX, KOSPI)

- TNX explained: why the 10Y yield drives markets

- The Modern 60/40: risk budget framework

- How to read the yield curve (2s10s & 3m10y)

- Geopolitics → USD liquidity → FX

- Oil shock → USD/KRW transmission

FAQ

Q1) Does the S&P 500 always lead the KOSPI?

Not always. Korea can react earlier when FX and foreign positioning change first. In some episodes, USD/KRW and flows “announce” stress before U.S. equities fully reprice.

Q2) Is a weaker KRW always good for exporters?

Not necessarily. Exporters may benefit from translation effects, but input costs, hedging, and pricing power can offset it. The net outcome depends on margin structure and demand.

Q3) If U.S. yields fall, is that automatically bullish for Korea?

No. Yields can fall for “good” reasons (easing inflation) or “bad” reasons (growth fear). The difference shows up in earnings expectations and sector leadership.

Q4) What’s the minimum setup for daily monitoring?

If you keep only three: (1) S&P direction and volatility, (2) USD/KRW, (3) TNX (U.S. 10Y yield). Add DXY when you want to confirm broad USD strength.