Your first salary needs a simple order of operations: identify take-home pay, lock in fixed costs, build a starter emergency fund, set a debt rule, then invest a sustainable monthly amount toward clear goals. This guide is an educational planning framework, not personal financial advice.

Related reads: The three pillars of personal finance, Emergency fund by risk, and High-rate debt vs investing threshold rule. When you want to turn a goal into a monthly number, start with the Goal Simulator.

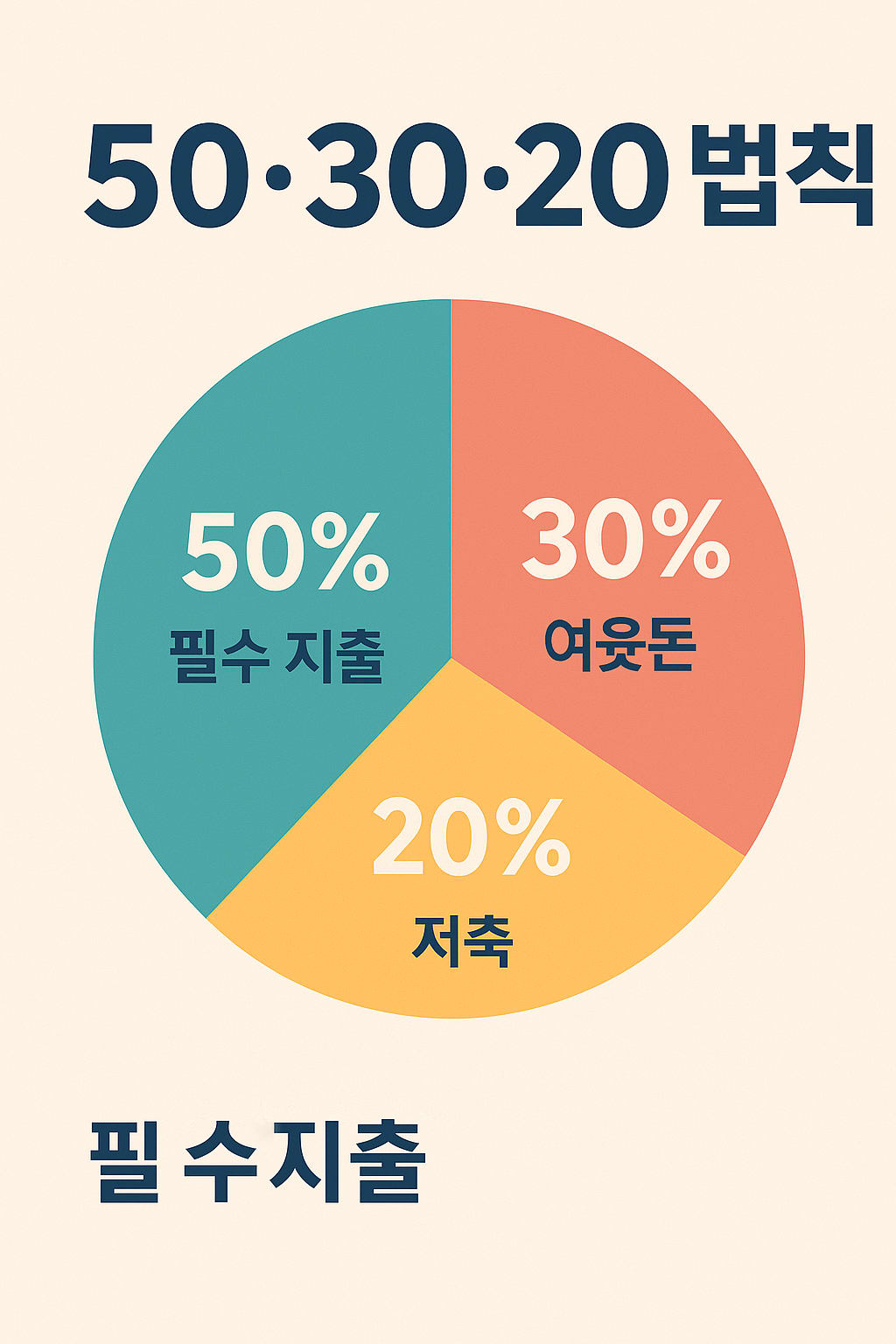

Quick Answer

If you are budgeting your first paycheck, do not begin with a perfect spreadsheet. Begin with a repeatable salary system.

| Setup step | What to decide | Simple starting rule |

|---|---|---|

| Take-home pay | Net income after tax and payroll deductions | Budget from take-home pay, not gross salary |

| Fixed costs | Rent, utilities, transport, phone, insurance | Keep them visible before lifestyle spending |

| Emergency fund | Cash buffer for job, health, moving, or family shocks | Start with 1 month of essentials, then expand |

| Debt rule | Whether extra cash goes to debt or investing | Prioritize high-interest debt first |

| Monthly investing | A sustainable automatic amount | Start small enough to continue for 12 months |

| Goal planning | Target amount and timeline | Convert goals into monthly targets with calculators |

The best first salary budget is not the one with the highest savings rate. It is the one you can repeat through busy months, unexpected expenses, and changing goals.

Step 1: Map Take-Home Pay and Fixed Costs

Your first number is take-home pay: the amount that actually arrives in your account. A common beginner mistake is planning from headline salary and then wondering why the monthly budget feels tight.

Use this fixed-cost checklist before setting any savings or investing target.

| Fixed-cost item | Include it? | Why it matters |

|---|---|---|

| Rent or housing payment | Yes | Usually the largest monthly constraint |

| Utilities and internet | Yes | Often changes by season or contract |

| Phone plan | Yes | Easy to overlook because it is automatic |

| Transportation | Yes | Commute costs can reshape the budget |

| Insurance | Yes | Protects cash flow from large surprises |

| Subscriptions | Yes | Small items become meaningful in total |

After listing them, calculate your fixed-cost ratio:

| Take-home pay | Fixed costs | Fixed-cost ratio | Readout |

|---|---|---|---|

| $3,200 | $1,450 | 45.3% | Manageable, but lifestyle spending needs limits |

| $3,200 | $1,900 | 59.4% | Tight; avoid aggressive investing targets too early |

| $3,200 | $2,200 | 68.8% | Fixed costs are the main budget problem |

If fixed costs are too high, improving them may matter more than finding a complicated investing strategy.

Step 2: Build a Starter Emergency Fund

Before maximizing investing, create a cash buffer that prevents one unexpected bill from forcing credit-card debt or early investment selling.

A full emergency fund may eventually reach 3 to 6 months of essential expenses, but a first-salary setup can start smaller.

| Stage | Target | Purpose |

|---|---|---|

| Starter buffer | $500 to $1,000 | Small medical, travel, or repair costs |

| First milestone | 1 month of essential expenses | One month of breathing room |

| Stronger buffer | 3 months of essential expenses | Job change or larger family events |

| Full buffer | 6 months or more | Higher uncertainty, variable income, or dependents |

For a deeper risk-based framework, see Emergency fund by risk.

Step 3: Set a Debt Rule Before Investing More

Debt does not always mean you should stop every investment. But high-interest debt can overwhelm reasonable market returns, so your first salary plan needs a rule.

| Debt type | Example rate | First-salary rule |

|---|---|---|

| Credit-card balance | 18% to 25%+ | Prioritize payoff before extra investing |

| Personal loan | 7% to 15% | Compare rate, repayment term, and cash buffer |

| Student loan | 3% to 8% | Keep required payments, then evaluate extra payoff |

| Mortgage or low-rate loan | Varies | Usually a longer-term planning decision |

The decision is not only mathematical. Liquidity, job stability, and mental stress matter too. Use High-rate debt vs investing threshold rule as a companion framework.

Step 4: Start Monthly Investing with a Sustainable Amount

Once fixed costs and starter cash are under control, begin monthly investing at an amount you can keep through normal life changes. Consistency usually beats an ambitious plan that stops after three months.

| Monthly investing amount | 10-year contribution | What to test next |

|---|---|---|

| $100 | $12,000 | Habit building and account setup |

| $250 | $30,000 | Basic long-term wealth routine |

| $500 | $60,000 | Stronger accumulation, but cash flow must support it |

| $750 | $90,000 | Useful only if fixed costs and emergency fund are stable |

Use the DCA Calculator to test how recurring contributions can behave under different return assumptions. For a longer explanation, read Monthly DCA 10-year result.

Step 5: Turn Goals Into Calculator-Based Monthly Targets

Goals become useful only when they turn into a monthly action. "I want to save more" is vague; "I need $420 per month for a $20,000 goal over 4 years at a 3% assumption" is actionable.

| Goal type | Inputs to define | FinMap workflow |

|---|---|---|

| Cash reserve | Target cash amount, months to build | Use the Goal Simulator |

| Portfolio target | Target amount, years, return assumption | Compare with Goal Simulator and DCA Calculator |

| Compounding plan | Starting amount, monthly contribution, annual return | Test in the Compound Interest Calculator |

| Long-term independence | Spending, savings rate, assets, return assumption | Use the FIRE Calculator as a secondary planning tool |

If you want a broader target-portfolio guide, read How much to invest monthly for a target portfolio.

Example First Salary Budget Table

This example uses $3,200 of monthly take-home pay. The exact percentages are less important than making every dollar's role visible.

| Category | Example amount | Share of take-home pay | Purpose |

|---|---|---|---|

| Fixed essentials | $1,450 | 45.3% | Rent, utilities, phone, transport, insurance |

| Flexible spending | $550 | 17.2% | Food, leisure, shopping, social life |

| Starter emergency fund | $350 | 10.9% | Build the first cash buffer |

| Debt payoff | $250 | 7.8% | Extra payment toward high-interest debt |

| Monthly investing | $350 | 10.9% | Recurring DCA contribution |

| Goal sinking funds | $250 | 7.8% | Travel, moving, education, large purchases |

| Total | $3,200 | 100.0% | Full salary allocation |

After the starter emergency fund reaches the first milestone, some of that monthly amount can move toward debt payoff, investing, or a specific goal.

Calculator Workflow

Use calculators in this order so the plan moves from cash flow to long-term goals.

- Open the Goal Simulator and enter a target amount, starting balance, timeline, and expected return.

- Use the DCA Calculator to compare monthly investing amounts and return assumptions.

- Use the Compound Interest Calculator to see how time and reinvested growth can change the long-term result.

- Treat the FIRE Calculator as a later-stage tool after your emergency fund, debt rule, and monthly investing habit are stable.

Calculator outputs are estimates for education and planning. Actual investment results can differ because returns, inflation, taxes, fees, and personal circumstances change.

Common Mistakes

| Mistake | Why it hurts | Better move |

|---|---|---|

| Budgeting from gross salary | Deductions make the plan too optimistic | Use take-home pay |

| Investing before any cash buffer | One surprise bill can break the plan | Build a starter emergency fund first |

| Ignoring high-interest debt | Interest cost may exceed likely returns | Create a debt rule |

| Starting with an unrealistic DCA amount | The plan stops when life gets expensive | Choose a repeatable amount |

| Copying someone else's ratio | Rent, family support, debt, and country rules differ | Test your own numbers |

Bottom Line

A strong first salary setup does not require a complex system. Map take-home pay, control fixed costs, build a starter emergency fund, set a debt rule, start a sustainable monthly investing habit, and convert goals into calculator-based targets.

Once the system is running, improve it gradually: reduce fixed costs, increase monthly contributions, and revisit your goals whenever salary, rent, debt, or family responsibilities change.

FAQ

How should I split my first salary?

Start by separating take-home pay into fixed essentials, flexible spending, emergency fund contributions, debt payoff, monthly investing, and goal sinking funds. A percentage rule can help, but your actual rent, debt, and job stability should decide the final split.

How much emergency fund should I build first?

Begin with a starter buffer of $500 to $1,000, then work toward 1 month of essential expenses. After that, many people expand the fund toward 3 to 6 months depending on income stability, family responsibilities, and risk level.

Should I pay off debt or start investing?

High-interest debt should usually be prioritized before extra investing because the interest cost can exceed a reasonable expected return. For lower-rate debt, compare the rate, liquidity needs, job stability, and your long-term investing habit.

How much should a beginner invest monthly?

Choose an amount you can repeat for at least 12 months without breaking your emergency fund or relying on credit cards. Even $100 or $250 per month can build the habit, and you can increase it after your cash flow becomes more stable.

Which FinMap calculator should I use first?

Start with the Goal Simulator if you have a target amount and timeline. Use the DCA Calculator for monthly investing assumptions, the Compound Interest Calculator for long-term growth, and the FIRE Calculator only as a secondary long-term planning tool.