Summary (10 sentences)

- Most people try to invest first, but the real win is building a system that survives bad months.

- Your “return” is meaningless if one unexpected bill forces you to sell at the worst time.

- Budgeting is not restriction—it’s visibility and control over cash flow.

- An emergency fund is insurance that protects your investing plan from life events.

- Long-term investing works best when it runs on autopilot and doesn’t depend on motivation.

- The correct order is usually Budget → Emergency Fund → Long-Term Investing, with overlap once stable.

- The three pillars reinforce each other: clearer spending, fewer panic decisions, better compounding.

- Your goal is not perfect optimization; it’s consistency for years.

- A “simple” plan that you actually follow beats a complex plan you abandon in three months.

- Once the foundation is stable, CAGR and goal simulations become realistic tools—not fantasies.

One-paragraph takeaway

If you want investing to feel calm (instead of stressful), you need a foundation that absorbs shocks. That foundation is a clear budget, an emergency fund sized to your life, and a long-term investing system that runs even when you’re busy, tired, or the market is ugly. This guide shows how to build that foundation with practical steps, checklists, and pitfalls—so your money plan keeps working in the real world.

The right order changes everything

If you build the “engine” first (cash flow + safety buffer), investing stops feeling like gambling and starts behaving like a routine. The goal is not to predict markets—it’s to stay invested long enough for compounding to matter.

Core points to remember

- Budget = control and visibility (not punishment)

- Emergency fund = prevents forced selling

- Investing = automated, long-term, boring by design

- Stability beats intensity

1. Why “investing first” often fails in real life

A lot of personal finance advice sounds logical in theory: “Start investing early. Maximize returns. Don’t waste time.”

But in practice, people don’t quit investing because they hate it—they quit because life interrupts it.

A surprise medical bill. A car repair. A job transition. A family event. A rent spike.

If you don’t have a buffer, you’re forced to do the worst possible thing: sell investments when you don’t want to.

That’s why the three pillars exist. They solve different real-world problems:

- Budgeting prevents silent leakage (the “Where did my money go?” problem).

- Emergency fund prevents panic (the “I must sell now” problem).

- Long-term investing turns surplus into growth (the “How do I build wealth over years?” problem).

When the pillars are built in the right sequence, your plan becomes durable.

2. The “three pillars” framework (and the order that actually works)

People sometimes argue about whether investing should come first. The answer depends on your situation, but the default order is:

- Budgeting (cash flow stability)

- Emergency fund (shock absorber)

- Long-term investing (compounding engine)

This is not a motivational slogan. It’s risk management.

If you invest without budgeting, you often invest inconsistently.

If you invest without an emergency fund, you often invest until the first crisis.

If you invest without both, your “strategy” is basically hope.

3. Pillar #1 — Budgeting that doesn’t feel miserable

Budgeting fails when it’s built like a punishment.

Budgeting succeeds when it’s built like a dashboard.

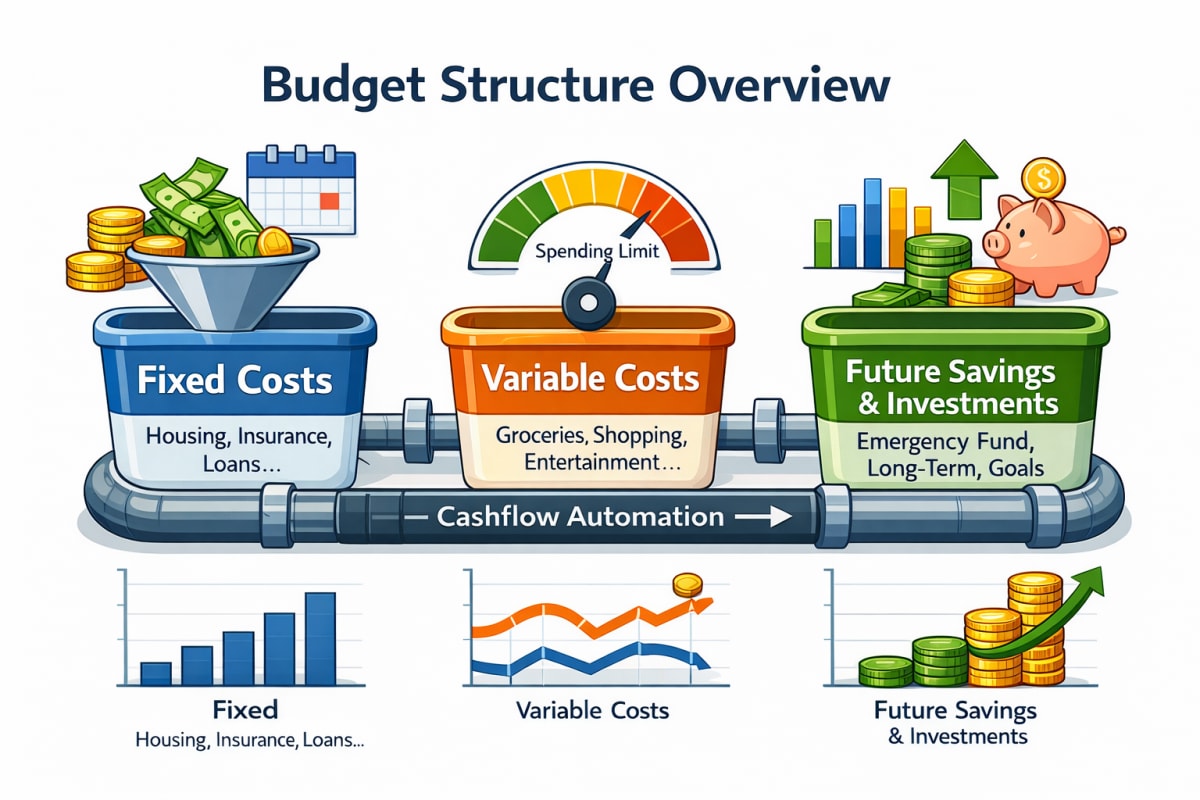

3-1. A practical budgeting method: “Fixed → Flexible → Growth”

A clean way to structure your money is to divide it into three buckets:

- Fixed costs: housing, insurance, subscriptions you truly use, minimum debt payments

- Flexible costs: groceries, transport, eating out, shopping

- Growth: savings + investing + skill building

Your goal is to create a stable monthly baseline.

Even if income fluctuates, you want the plan to “snap back” quickly.

3-2. The simplest rule that works: one “spending ceiling”

You don’t need 20 categories.

You need one number you can control.

Example:

- Fixed costs are mostly non-negotiable in the short term.

- You pick one variable number: “Flexible spending ceiling.”

- Anything above that becomes your “leak” target.

Over time, most people find 1–2 leak categories:

- delivery apps

- impulse online shopping

- subscription pileup

- convenience spending

Fixing a leak once is worth more than debating portfolio allocations for weeks.

4. Pillar #2 — Emergency fund: the anti-panic asset

An emergency fund is not an investment.

It’s insurance that keeps your investment plan alive.

4-1. How much emergency fund is “enough”?

A common guideline:

- 3 months: stable job, low fixed costs, strong family support

- 6 months: typical household, moderate risk, normal fixed costs

- 9–12 months: unstable income, self-employed, high fixed costs, dependents

The key is not the exact number—it’s whether your buffer matches your risk.

4-2. Where to keep it (so you don’t sabotage yourself)

Emergency funds should be:

- liquid (available fast)

- low volatility (no market drawdowns)

- boring (that’s the point)

If your “emergency fund” can drop 20% in a bad month, it’s not a fund.

It’s another risk asset.

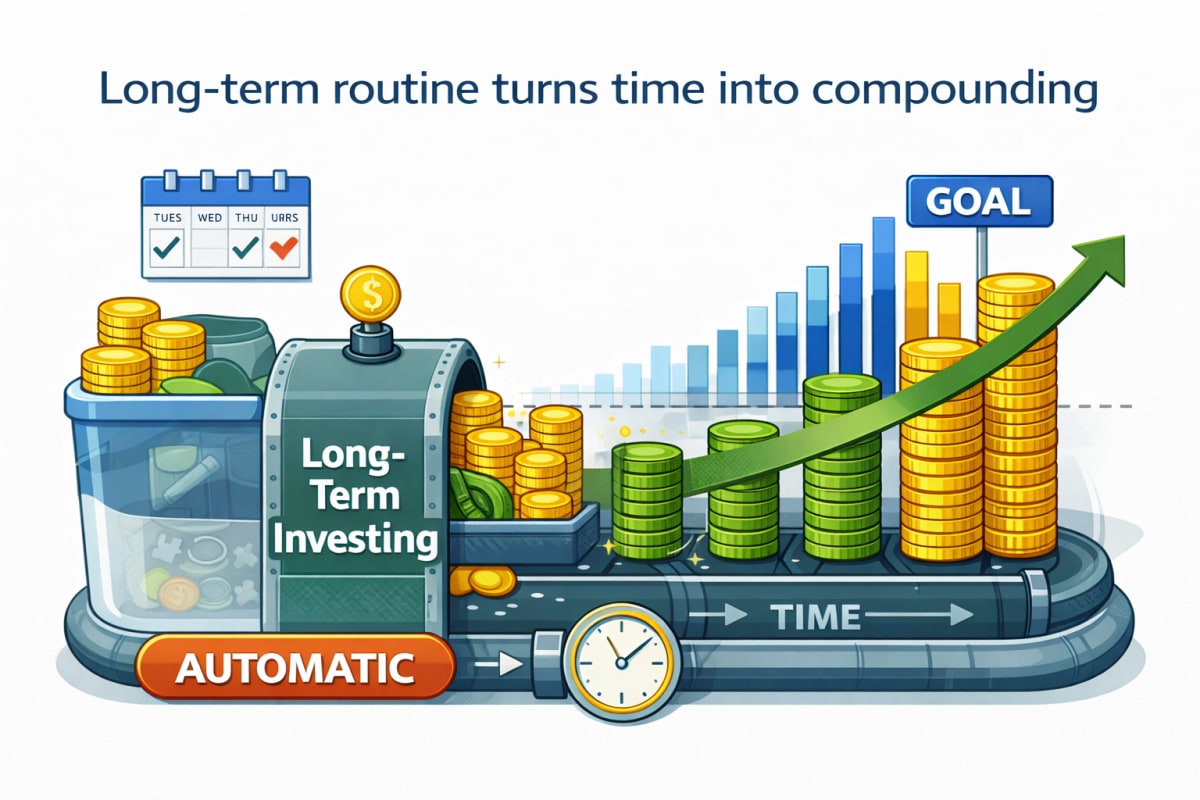

5. Pillar #3 — Long-term investing: the boring system that wins

Long-term investing works best when it becomes automatic.

The biggest personal finance unlock is this: Your portfolio should not require weekly emotional decision-making.

5-1. Build automation before you build complexity

A durable default:

- monthly automatic contribution

- simple portfolio (broad funds/ETFs)

- periodic review (quarterly or semiannually)

You don’t need to “feel confident” every month.

You need the system to keep running even when confidence is low.

5-2. Why compounding feels slow at first

Compounding is not linear.

Early on, it feels like nothing is happening, because the base is small.

Later, growth becomes visible because the base is bigger.

That’s exactly why the first two pillars matter: they keep you from quitting too early.

6. The reality check: “High return” is not a plan

Many people build plans like this:

“I’ll invest aggressively, earn 10–12% annually, and it’ll work out.”

But real investing includes:

- drawdowns

- volatility

- sequences of bad years

- life interruptions

- behavioral mistakes

So the foundation needs to protect you from the worst timing mistakes.

Investing first (without foundation)

- Inconsistent contributions

- Forced selling during emergencies

- Stress-driven timing decisions

- Higher chance of quitting

Foundation first (then investing)

- Stable monthly plan

- Emergency fund absorbs shocks

- Investing becomes routine

- Higher chance of compounding working

7. Two core tables you can actually use

7-1. Setup roadmap by phase (what to do first)

| Phase | Main goal | What “done” looks like | Typical mistake | Fix |

|---|---|---|---|---|

| Phase 1 | Budget visibility | You know fixed costs + monthly spending ceiling | Too many categories | Use 1 spending ceiling + fixed cost list |

| Phase 2 | Emergency buffer | 3–6 months of essential expenses saved | Investing aggressively before buffer | Pause extra investing until buffer is stable |

| Phase 3 | Automation | Monthly auto-invest runs regardless of mood | Manual timing decisions | Automate + review quarterly |

| Phase 4 | Optimization | Rebalancing, tax/fee awareness | Over-optimizing early | Optimize only after consistency |

| Phase 5 | Scale | Increase contributions as income grows | Lifestyle inflation absorbs raises | “Raise → invest more” rule |

7-2. The “three pillars” checklist table

| Pillar | Purpose | Minimum target | Strong target | Warning sign |

|---|---|---|---|---|

| Budget | Control cash flow | fixed costs mapped + spending ceiling | monthly surplus is consistent | “I don’t know where my money went” |

| Emergency fund | Prevent forced selling | 3 months essentials | 6–12 months depending on risk | selling investments to pay bills |

| Investing | Grow wealth long-term | automated monthly contributions | increasing contributions annually | investing only when “market feels safe” |

8. Beginner vs advanced: how the same framework scales

8-1. For beginners: focus on survival and consistency

If you’re early in your journey, the main objective is not optimization.

It’s avoiding “blow-ups” that reset your progress.

A practical beginner approach:

- make the budget simple

- build 3 months buffer

- start auto-investing small

- increase gradually

This reduces anxiety and builds the habit muscle.

8-2. For experienced investors: the foundation becomes a performance tool

When your base is stable, you can start improving:

- contribution rate

- portfolio simplicity vs factor exposure

- fee control

- tax efficiency (depending on your situation)

But the principle stays the same:

You only optimize what you can maintain.

Even sophisticated investors get wrecked by weak cash flow.

A strong system isn’t “beginner”—it’s professional.

9. visualize the three pillars

10. A simple “start today” checklist (7 items)

- Write down all fixed costs (housing, insurance, debt minimums, essential subscriptions)

- Pick one flexible spending ceiling you can follow

- Identify your biggest leak category and set a weekly cap

- Decide your emergency fund target (3/6/9 months) based on risk

- Open a dedicated emergency fund account (separate from spending money)

- Turn on monthly auto-investing (small is fine)

- Set one review day each quarter (not weekly)

11. Conclusion (3 lines)

A stable money system is built, not wished for.

Budgeting and an emergency fund protect your investing behavior.

Once the foundation is in place, long-term investing becomes calm—and compounding can finally do its job.

Use FinMap tools to make the plan real

If you already have a baseline monthly surplus, you can simulate the long-term outcome. Use a goal simulator to turn “someday” into a number—and a timeline.

Open Goal SimulatorWant to test realistic return assumptions?

Before you set a target, check how sensitive your plan is to return rates and time. Small return changes can shift your timeline more than people expect.

Open Compound Interest Calculator12. A good piece of writing to read together

- Simple vs. Compound Interest — The Most Important Finance Principle for Beginners

- How Much Should You Invest Each Month to Reach $100,000?

- Annual vs Monthly Compounding: How Much Faster Can You Reach Your Goal?

- A 5-Step Salary Management Guide for Young Professionals

- Currency Basics: What Really Moves the USD/KRW Exchange Rate

FAQ

Q1) Should I invest if I have no emergency fund yet?

If you’re starting from zero, it’s usually better to build at least a small buffer first. A tiny automatic investment is fine, but avoid building a plan that collapses the moment life happens.

Q2) Is budgeting still necessary if I have a high income?

Yes. High income without control can still produce low savings. Budgeting is not about income level—it’s about visibility and repeatability.

Q3) What if my income is unstable?

Then your emergency fund target should typically be larger, and your budget should be built around “minimum viable months.” The goal is to survive low months without liquidation.

Q4) How do I avoid giving up after two months?

Make the plan smaller. Reduce friction. Automate. The best plan is the one you can keep running when motivation disappears.

Q5) When should I start optimizing my portfolio?

After you’ve proven consistency for several months and your emergency buffer is stable. Optimization is useful, but only after the system exists.