Summary (10 sentences)

- A “3–6 months” emergency fund rule breaks because people have different risks, not different calendars.

- The right target starts with your essential burn rate (must-pay expenses), not your total lifestyle spend.

- Then you apply a risk multiplier based on job stability, dependents, and how fragile your income is.

- Debt changes everything: high-interest payments can turn a small shock into a spiral.

- Emergency savings should be held in tiers so you don’t sell long-term assets in panic.

- Your fund is “complete” when it protects decisions: you can wait for a good job, avoid forced selling, and keep bills current.

- The biggest mistake is storing the fund in volatile assets and calling it “savings.”

- Another mistake is over-saving cash while ignoring toxic-interest debt that guarantees losses.

- You can build a fund faster by setting a fixed monthly contribution and a realistic deadline.

- Review the fund whenever your job, family, or debt profile changes—not once a year.

This post is Korea-context, so some examples may mention KRW-style realities (housing deposits, loan structures). The framework works globally; the numbers are placeholders.

1) Why “3–6 Months” Fails in Real Life

Two households can both earn the same income and still need completely different emergency funds.

- Household A: stable job, no dependents, low fixed costs, no expensive debt.

- Household B: variable income, dependents, high housing costs, and debt payments that cannot pause.

The calendar rule treats them as identical. Reality doesn’t.

What you’re really buying with an emergency fund is not “months.”

You’re buying decision time—the ability to respond without panic.

2) Define the Only Number That Matters: Your Essential Burn Rate

Start here:

Essential Burn Rate (monthly) = Must-pay expenses that keep life functioning

Include:

- Housing (rent/loan interest + building fees)

- Utilities + phone/internet

- Minimum debt payments (the “can’t miss” amount)

- Food basics

- Insurance premiums

- Transportation for work/school

- Child-related essentials (if applicable)

Exclude (for this purpose):

- Dining out, subscriptions, shopping

- Optional travel/entertainment

- “Nice-to-have” upgrades

If you don’t have this number yet, read:

- The Three Pillars of Personal Finance: Budgeting, Emergency Funds, and Long-Term Investing

- Household Survival in an Inflation Era: Cut Fixed Costs, Control Spending, and Protect Cash Flow

3) A Simple Risk-Based Formula (No Fancy Math)

Use a two-step target:

Emergency Fund Target = Essential Burn Rate × Risk Months

Where Risk Months is not a default 3–6. It is chosen using your risk profile:

- Job/income stability

- Dependents and obligations

- Debt burden + interest sensitivity

Step A — Choose Your Baseline Risk Months

A practical baseline:

- Low risk: 2–3 months

- Medium risk: 4–6 months

- High risk: 7–12 months

Step B — Apply “Risk Modifiers” That People Usually Ignore

Add risk months when:

- Your income is commission-based, freelance, or business-linked.

- Your household has dependents or caregiving responsibilities.

- Your fixed costs are high and hard to cut quickly.

- You carry debt that becomes dangerous if income drops.

4) Risk-Based Emergency Fund Guide (Job / Family / Debt)

| Profile factor | Low risk | Medium risk | High risk |

|---|---|---|---|

| Job stability | Tenured/secure role, predictable pay | Stable but replaceable, industry cyclical | Contract/freelance/commission, unstable industry |

| Dependents | None | 1 dependent or shared support | Multiple dependents / sole provider |

| Fixed costs | Low and flexible | Moderate | High and sticky (housing, education, care) |

| Debt pressure | Low-interest, manageable | Mix of loans, some pressure | High-interest debt or high monthly obligations |

| Recommended “Risk Months” | 2–3 | 4–6 | 7–12 |

| Main goal | Convenience & buffer | Stability through moderate shocks | Survival through long shocks |

How to use the table:

Pick the column that matches the weakest link in your household. If your debt pressure is “High risk,” you don’t get to call the whole plan “Low risk.”

5) The “Debt–Interest” Trap: Why Some Households Need More Cash (or a Different Order)

Emergency funds and debt payoff compete for the same money, so you need a rule that avoids both extremes:

- saving too little cash and collapsing during a shock, or

- saving too much cash while paying toxic interest every month.

A practical ordering:

- Mini buffer first (e.g., 2–4 weeks of essentials)

- Stop the bleeding if you have high-interest debt (attack the worst APR)

- Build the full risk-based emergency fund

- Then invest long-term consistently

If you want the rate logic behind “toxic interest,” see:

- Understanding Interest Rates: Policy Rates, Market Rates, and How They Influence Deposits, Loans, and Bonds

- A Rate Cut Doesn’t Guarantee Lower Borrowing Costs: How to Read Policy Rates vs Market Rates

6) Compare: “Months Rule” vs “Risk Rule”

The “Months” Rule (generic)

- Assumes everyone has the same income risk

- Often uses total spending, not essential burn

- Ignores dependents and debt fragility

- Encourages false confidence (“I have 3 months, I’m safe”)

The “Risk” Rule (personalized)

- Starts with essential burn rate

- Scales with job stability and dependents

- Explicitly includes debt pressure

- Creates a fund that survives real shocks

7) Build It in Tiers (So You Don’t Liquidate Investments in Panic)

Emergency money should be accessible, safe, and boring.

A clean tiering approach:

- Tier 0 (Immediate): a small cash buffer for same-day issues

- Tier 1 (Near-term): 1–2 months of essentials in high-liquidity cash-like instruments

- Tier 2 (Full protection): the remaining target in low-volatility, liquid options

Where to Store Emergency Funds (Tier by Tier)

| Tier | Purpose | Liquidity need | Typical options | What to avoid |

|---|---|---|---|---|

| Tier 0 | Same-day emergencies | Instant | checking balance, small cash | anything with lock-up |

| Tier 1 | 1–2 months essentials | 1–3 days | high-yield savings, money-market style cash | stocks/crypto, long-duration bonds |

| Tier 2 | full risk coverage | within a week | conservative cash management, short-duration instruments | “investment accounts” that can drop 20% |

The rule: If it can fall sharply when you need it, it’s not an emergency fund.

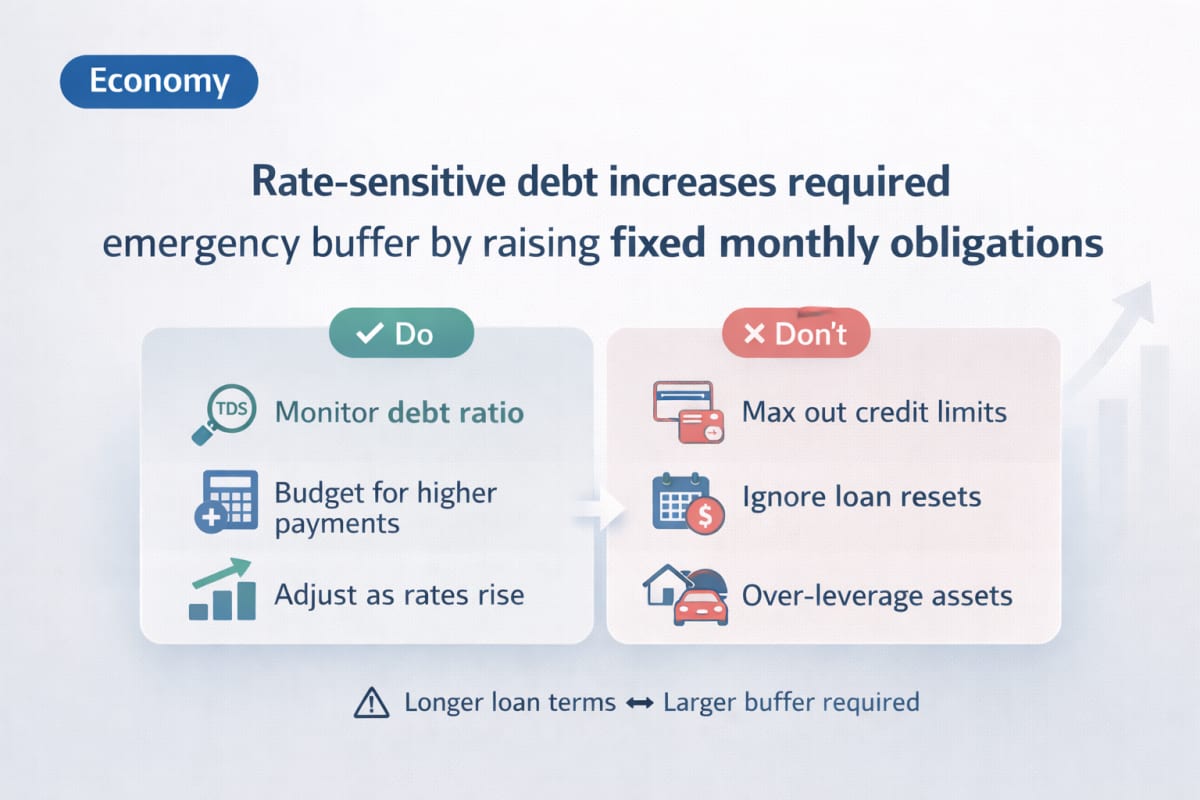

8) Summary Images — The 3 Visual Rules That Anchor the Whole Strategy

9) Beginner Version: A Fast Setup You Can Finish This Week

If you want the simplest “done in a weekend” version:

- List essential expenses only (housing, utilities, minimum debt, food, transport, insurance).

- Pick your risk months:

- stable job + no dependents + low debt → 3 months

- dependents or high fixed costs → 6 months

- unstable income or high interest burden → 9–12 months

- Create one dedicated account for Tier 1/2 so the money doesn’t leak.

- Automate a monthly transfer right after payday.

You don’t need perfect tools to start. You need a rule that runs without motivation.

10) Advanced Version: Make It Robust Against “Compound Shocks”

Real life often stacks shocks:

- job loss + medical cost

- rate reset + currency volatility + slow hiring market

- business downturn + delayed receivables

Advanced improvements:

- Separate the fund by purpose (household vs business vs medical buffer).

- Add “income replacement” logic if your job search cycle is long.

- Stress-test your burn rate: “What if income is 0 for 3 months?”

- Reduce fixed costs before you increase investment risk.

If your risk is macro-sensitive (rates/FX), add these to your reading list:

- Currency Basics: What Really Moves the USD/KRW Exchange Rate

- USD/KRW and KOSPI: What the Exchange Rate Signals for Foreign Flows and Valuations

11) Checklist: Emergency Fund That Actually Works (7+ items)

Use this as a pass/fail checklist:

- I know my essential burn rate (monthly must-pay).

- My target is based on job + dependents + debt, not a generic “months” rule.

- At least one month of essentials is in a safe, liquid place.

- My emergency money is not invested in volatile assets.

- I can access Tier 1 within a few days without selling stocks.

- I have a rule for high-interest debt (mini buffer → payoff → full fund).

- My household can survive a short shock without borrowing.

- My household can survive a long shock without forced selling.

- I review the plan when job/family/debt changes.

- I have a clear “fund complete” definition (a number + where it lives).

12) Conclusion (3 lines)

- Your emergency fund is not a “months” slogan—it’s a risk-based system.

- Size it from essential burn rate and your job/family/debt reality, then store it in tiers.

- When the fund is correct, your investments stop being fragile.

13) FinMap Tool CTA

Want a clear monthly plan to reach your emergency fund target?

Set a target amount and timeline, then reverse-calculate how much to save each month. A plan that runs automatically is more powerful than motivation.

Open FinMap Goal Simulator14) A good piece of writing to read together — Read These Next to Build the Full Household “Safety System”

- The Three Pillars of Personal Finance: Budgeting, Emergency Funds, and Long-Term Investing

- Household Survival in an Inflation Era: Cut Fixed Costs, Control Spending, and Protect Cash Flow

- Understanding Interest Rates: Policy Rates, Market Rates, and How They Influence Deposits, Loans, and Bonds

- A Rate Cut Doesn’t Guarantee Lower Borrowing Costs: How to Read Policy Rates vs Market Rates

- Currency Basics: What Really Moves the USD/KRW Exchange Rate

- Simple vs. Compound Interest — The Most Important Finance Principle for Beginners

FAQ

Q1) Is it okay to invest my emergency fund to “beat inflation”?

A true emergency fund is designed to be there during bad markets, which is exactly when risky assets can drop. If you invest it, you’re changing its job. Keep emergency money safe and liquid; invest long-term money with long-term rules.

Q2) Should I build the emergency fund first or pay off debt first?

Do both in order: build a mini buffer first, then attack high-interest debt, then complete the risk-based fund. Skipping the buffer often forces you back into debt during the first surprise expense.

Q3) What expenses should be counted in the essential burn rate?

Count what keeps your household stable: housing, utilities, minimum debt payments, food basics, insurance, and work/school transport. Exclude lifestyle spending because that’s what you can cut during a shock.

Q4) How often should I review the emergency fund?

Whenever your risk profile changes: job change, new dependent, new loan, rate reset, moving, or a major income shift. The fund should track your reality, not your past.

Q5) When do I know the emergency fund is “done”?

It’s done when you can survive your chosen shock window (risk months) without forced selling and without missing essential payments—while staying calm enough to make good decisions.