PERSONAL FINANCE · HIGH-RATE DECISIONS

In a high-rate era, the hardest part isn’t math. It’s decision consistency. “Should I kill my debt first?” “Am I falling behind if I don’t invest?” These questions repeat because you don’t have a rule that fits your cash flow, not because you’re missing one more chart.

This post gives you a simple system: the Interest-Rate Threshold Rule. You’ll convert debt payoff into a “risk-free return,” adjust investing expectations for taxes, fees, and behavior, and then turn the result into a paycheck allocation you can keep for 90 days at a time.

- Debt payoff as a guaranteed return (and why that matters)

- A realistic investing return: after tax, after fees, after panic

- The 3% / 6% / 9% thresholds that produce clear rules, not vibes

Scope: No product recommendations. This is about prioritization, rules, and execution.

Quick map: what you’ll do in 10 minutes

Here’s the “no-overthinking” path. If you only do one thing, do this.

- Write down each debt’s interest rate (APR) and whether it’s variable or fixed.

- Define your “behavior-adjusted” investing return (a conservative number you can live with).

- Apply the threshold rule: ≥9% pay down fast, 6–9% pay down more, 3–6% split, <3% invest more.

- Keep investing something (even small) to protect the habit and avoid future regret spirals.

- Build/maintain an emergency buffer so one surprise bill doesn’t reset your entire plan.

- Freeze the plan for 90 days; then review once (don’t renegotiate weekly).

- Use a simple automation: transfers on payday, not “when you feel ready.”

- Track only two things: debt rate bucket and monthly free cash flow.

The core idea: debt payoff is a guaranteed return

Paying down debt is not just “reducing bills.” It’s also an investment with a special feature:

- If your APR is 8%, paying it down is like earning an 8% guaranteed, risk-free return on that money.

That guarantee is rare. Most investments can beat 8% sometimes—but they can also underperform it for years, and behavior (panic selling, stopping contributions) often turns “expected return” into “lived return.”

So the decision isn’t “debt vs investing.” It’s:

Guaranteed return today vs uncertain return over time

(adjusted for taxes, fees, and whether you’ll actually stick with it).

If that framing already reduces your anxiety, good. It means you’re switching from “hope” to “comparison.”

Why high-rate eras break people: three predictable mistakes

1) Using optimistic market returns as if they were personal returns

People quote long-run averages and forget the lived experience includes: drawdowns, job changes, family expenses, and the temptation to stop.

2) Treating “same percentage” as the same thing

8% debt APR is not the same as “8% expected market return.” One is guaranteed; the other is probabilistic.

3) Ignoring cash flow fragility

Most plans fail because a surprise expense forces you to borrow again, or because the monthly payment stress makes you abandon the plan.

In other words: you don’t fail at math. You fail at survivability.

Step 1: convert each debt into a “return you can’t ignore”

Make a simple list:

- Credit card APR: ___%

- Personal loan APR: ___%

- Auto loan APR: ___%

- Mortgage APR: ___%

- Student loan APR: ___%

- Any variable-rate debt: ___% (and how quickly it can reset)

Then ask one practical question:

“If I invest $1,000 instead of paying this down, am I confident I’ll beat this APR after tax, after fees, and after stress?”

If the honest answer is “not sure,” you just found your threshold.

Step 2: define your behavior-adjusted investing return

A realistic personal return is not the market’s return. It’s what you will capture.

A simple way to estimate:

- Start with a conservative long-run equity return assumption

- Subtract: fees, taxes (or tax drag), and “behavior drag” (the cost of stopping in bad years)

You don’t need perfection. You need a number you can defend emotionally in a bad month.

A practical default

For many retail investors, a conservative behavior-adjusted range is:

- 4–6% for diversified investing (after fees and realistic taxes, assuming you stay invested)

Could it be higher? Yes. But the threshold rule works best when it prevents plan collapse.

If you want more detail on why “policy cuts” don’t always translate to cheaper real-world borrowing costs, this helps build your rate intuition:

(That link is optional reading—today’s post is about your household decision rule.)

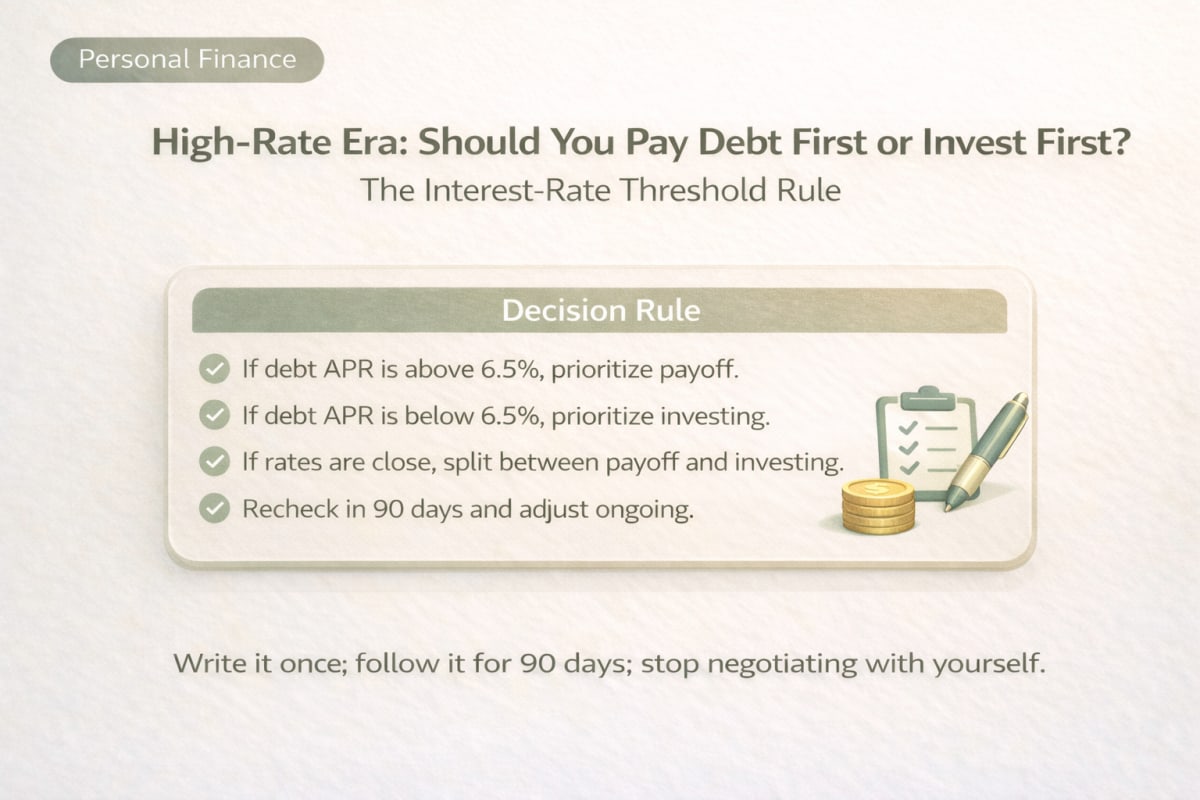

The Interest-Rate Threshold Rule: 3% / 6% / 9%

The goal is not a perfect answer. The goal is a rule you’ll execute.

Table: simple buckets that reduce decision fatigue

| Debt APR (rough) | Default priority | Paycheck split (example) | Why this works |

|---|---|---|---|

| ≥ 9% | Pay down fast | Pay down 70–90% / Invest 10–30% | The guaranteed return is hard to beat and stress risk is high |

| 6–9% | Pay down more (keep investing) | Pay down 60–70% / Invest 30–40% | Payoff is attractive; keep the investing habit alive |

| 3–6% | Balanced split | Pay down 40–60% / Invest 40–60% | The “right” answer is unclear; survivability matters most |

| < 3% | Invest more | Pay down 20–40% / Invest 60–80% | Cheap debt has opportunity cost; liquidity and investing momentum matter |

Important: the split is not the point. The point is you can apply it without a weekly debate.

Debt type matters: the same APR can still behave differently

Credit cards and revolving debt: treat as emergency-level risk

Even “moderate” APR here can be destructive because it compounds fast and encourages reuse. If you’re carrying revolving balances, you’re usually in the pay down first camp.

Personal loans: watch refinancing and payment stress

Even if the APR is not extreme, high monthly payments can create cash flow fragility. If your payment stress is high, you tilt toward payoff earlier than the threshold suggests.

Mortgages: don’t accidentally destroy your liquidity

Many people overpay a low-rate mortgage and then face a life event and borrow again at a worse rate. If your mortgage is low-rate and stable, be careful: liquidity can be more protective than prepayment.

Variable-rate debt: add a “rate shock premium”

If the rate can reset higher, treat it as if it’s already somewhat higher. In high-rate eras, uncertainty itself is a cost.

The hidden boss fight: emergency cash determines whether your plan survives

Most “debt vs invest” arguments ignore the real killer: one unexpected bill.

If you don’t have a buffer, you can end up doing the worst cycle: pay down → surprise expense → borrow again → repeat.

A good rule:

- If you have no buffer, build a starter cushion first (even a small one)

- Then apply the threshold rule with confidence

If you want a risk-based way (instead of “X months”), this post connects well:

When the decision feels “too close,” splitting is not weakness—it’s strategy

The middle bucket (3–6%) is where people spiral: “I should do one thing perfectly.”

But in real life, split strategies reduce regret and protect behavior.

- If you pay down 100% and markets rise, you regret and chase.

- If you invest 100% and rates stay high, you stress and quit.

Splitting prevents whiplash.

Three split templates (lock for 90 days)

- Payoff-tilted: 70/30

- Balanced: 50/50

- Invest-tilted: 30/70

Pick one based on APR bucket and cash flow stress. Then freeze it.

The 90-day lock: how you stop renegotiating your life every week

High-rate eras increase noise: headlines, central bank meetings, market swings. If your plan updates weekly, it’s not a plan—it’s anxiety.

Here’s the fix:

- Choose your bucket and split

- Automate transfers on payday

- Lock for 90 days

- Review once: has APR changed? has cash flow changed? has your buffer changed?

Most people don’t need more information. They need fewer decision points.

A practical script: turn your plan into seven sentences

Copy this and fill the blanks. If you can’t write it, you can’t execute it.

- My highest debt APR is ___% and it sits in the ___ bucket.

- My starter emergency buffer target is $___ (or I will maintain $___).

- For the next 90 days, my paycheck split is ___% paydown / ___% investing.

- I keep investing at least $___ per month to protect the habit.

- I only review monthly cash flow and debt APR once per month (not daily).

- If a life event hits (job loss / medical / family), I pause extra investing before I miss payments.

- My goal is not max return—it’s a plan I can keep without breaking.

Common edge cases: when you should override the rule

If you’re missing payments or near it

Priority is stability. Pay down and restructure. Investing can resume after you’re stable.

If your employer matches retirement contributions

Often the match is an immediate, high “return.” Even if you’re paying down debt, consider contributing enough to capture the match.

If your investing habit is fragile

If you tend to stop investing in drawdowns, keep a minimum contribution even while paying debt down. Your long-term outcome is driven by staying in the game.

If you want to understand “why people fail at consistency,” this is relevant:

Korea context: why the same rule still applies (just watch the rate channel)

If you’re Korea-based, the mechanism changes but the logic doesn’t:

- Household borrowing costs can be sensitive to global rates (e.g., U.S. 10Y) and FX conditions

- “Policy moves” don’t always translate into lower real borrowing costs immediately

- Variable-rate structures can raise the importance of the “rate shock premium”

If you track one macro indicator to understand rate pressure:

This isn’t about predicting. It’s about understanding the risk that your debt cost stays high longer than you expect.

Use tools to make the rule tangible

If you want your rule to feel real, run the numbers once:

- Compound interest to understand what “investing return” could mean over time

- Goal simulator to translate goals into required monthly contributions

- DCA calculator to set a contribution you can keep in bad months

If you want the next layer: linking payoff to lifetime goals

Debt payoff is not just math—it’s optionality.

- Less payment stress increases your ability to invest consistently

- Lower fixed costs reduce the “forced selling” risk

- Psychological relief is a real asset in high-rate eras

If you want to compare growth rates more realistically (instead of headline returns):

FAQs

Q1) In a high-rate era, should I always pay debt first?

Not always. But the higher your APR, the more debt payoff behaves like a strong, risk-free return. The threshold rule helps you decide without relying on market forecasts.

Q2) Why use 3% / 6% / 9%? Are those “magic numbers”?

They’re not magic. They’re practical buckets that match how most people actually behave. At very high APRs, payoff dominates. In the middle, splitting reduces regret and prevents plan failure.

Q3) If I pay down debt and the market rallies, won’t I regret it?

Regret usually comes from going all-in. Keeping a minimum investment contribution (even small) protects the habit and reduces the urge to chase returns later.

Q4) Should I invest while carrying credit card balances?

If it’s revolving high-interest debt, payoff is usually the priority—especially if balances persist month to month. At minimum, stabilize cash flow and stop the balance from compounding.

Q5) What if my debt is low-rate but I feel anxious?

Anxiety is often a signal of cash flow fragility or low emergency buffer. Build a buffer, then follow the rule. If anxiety remains extreme, a slightly payoff-tilted split can be a valid “sleep premium.”

Q6) How do taxes and fees change the comparison?

They reduce your realized investing return. That’s why comparing debt APR to a conservative, behavior-adjusted investing return is safer than comparing to optimistic headline returns.

Q7) What about variable-rate debt?

Add a “rate shock premium.” If your rate can reset higher, treat it as riskier than its current number. In high-rate eras, uncertainty itself can be expensive.

Q8) What’s the most beginner-proof default plan?

If you’re unsure, use a 90-day 50/50 split (paydown/investing), keep a starter emergency buffer, and review once. Consistency beats constant optimization.