Mortgage affordability is not only an income question. In the Korean housing market, a buyer can have enough DSR room and still be limited by cash, LTV, and transaction costs.

Assumptions used throughout this article: KRW 100M, 200M, and 300M of cash, 70% LTV, and a 5% transaction-cost rate. DSR must be checked separately using income and existing debt, and the estimates may differ from an actual purchase budget.

This article compares KRW 100 million, KRW 200 million, and KRW 300 million of cash using the same DSR/LTV simulation logic used by the DSR/LTV Calculator. Enter your own cash, reserve cash, LTV, DSR, and target apartment price there before using these numbers as a reference.

Once you have a safer search range, open the Real Estate Dashboard and compare it with actual Seoul, Gyeonggi, and Incheon transaction prices. The figures below are examples, not policy automation or lender approval.

Quick Summary

- Passing DSR does not mean the apartment is affordable if cash or LTV fails.

- With 70% LTV and 5% transaction costs, a buyer needs roughly 35% of the home price in cash.

- In this example, KRW 100M of cash supports about KRW 286M of purchase price.

- KRW 200M of cash supports about KRW 571M, but a KRW 600M target is still tight.

- KRW 300M of cash shifts the bottleneck from cash/LTV to DSR under the same income assumption.

- The safer search range is 80-90% of the calculated maximum purchase price.

Assumptions

| Item | Input |

|---|---|

| Annual income | KRW 60M |

| Existing monthly debt | KRW 0 |

| Interest rate / term | 4.0% / 30 years |

| DSR / LTV entered by user | 40% / 70% |

| Extra transaction cost rate | 5% |

| Repayment method | Equal monthly principal-and-interest payment |

| Reserve cash | KRW 0 |

FinMap does not automatically apply Korean mortgage policy changes. The calculator uses the DSR and LTV values you enter and estimates an equal-payment loan. Actual lender review can differ because of credit profile, income recognition, collateral valuation, local rules, and bank-specific policy.

Purchase Budget by Cash on Hand

Use this as a quick cash-based reference. To include income, existing debt, and DSR, use the DSR/LTV Calculator.

| Cash on hand | Cash/LTV price limit | DSR price limit | Estimated price limit | Bottleneck |

|---|---|---|---|---|

| KRW 100M | KRW 285.71M | KRW 598.46M | KRW 285.71M | Cash/LTV |

| KRW 200M | KRW 571.43M | KRW 598.46M | KRW 571.43M | Cash/LTV |

| KRW 300M | KRW 857.14M | KRW 598.46M | KRW 598.46M | DSR |

Recalculate with your own constraints: Enter cash, income, existing debt, and LTV in the DSR/LTV Calculator.

The first jump, from KRW 100M to KRW 200M of cash, increases the estimated purchase budget sharply. But the next KRW 100M does not keep adding budget at the same pace, because DSR becomes the binding limit.

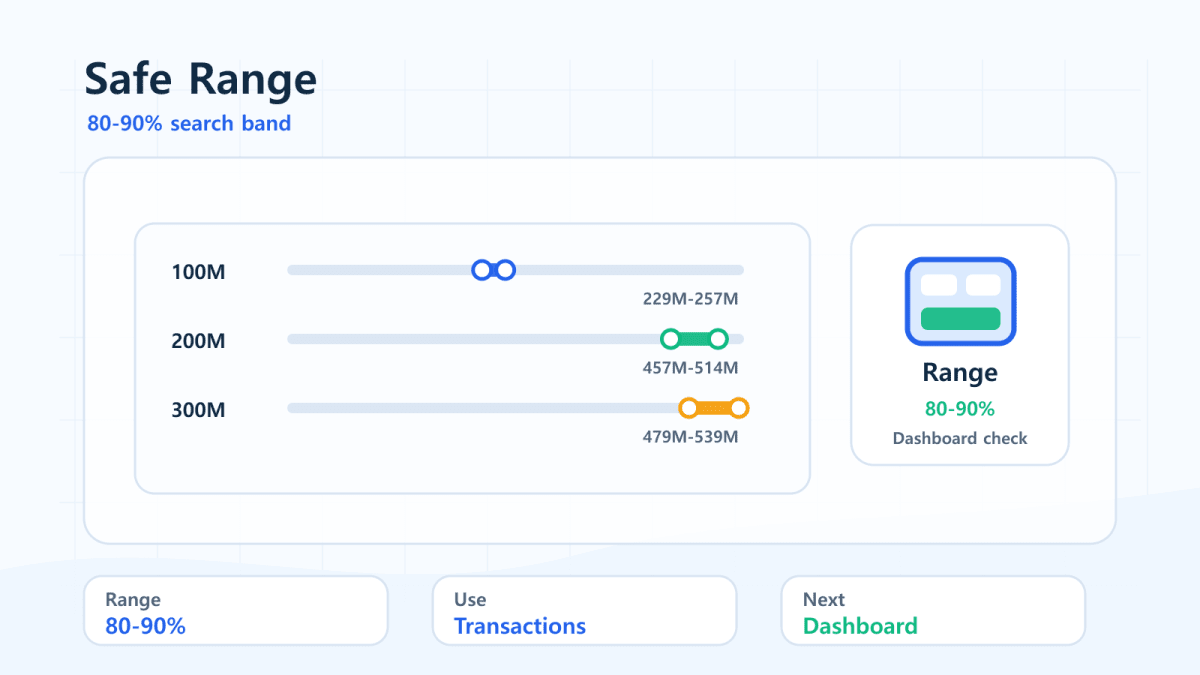

Safer Search Range

The calculator's safer search range is 80-90% of the estimated price limit. It is meant to give room for price negotiation, fees, maintenance costs, taxes, and underwriting differences.

| Cash on hand | Estimated price limit | Safer search range |

|---|---|---|

| KRW 100M | KRW 285.71M | KRW 228.57M - KRW 257.14M |

| KRW 200M | KRW 571.43M | KRW 457.14M - KRW 514.29M |

| KRW 300M | KRW 598.46M | KRW 478.77M - KRW 538.61M |

After calculating your own range in the DSR/LTV Calculator, use the Real Estate Dashboard to check whether recent transactions actually cluster inside that range.

KRW 100M Cash: Check Transactions in the KRW 200M Range

Under this article's assumptions, the safer search range is about KRW 228.57M-KRW 257.14M. Compare that range with actual transactions and transaction volume by area and complex.

Check actual apartment transactions in this price range: Open the dashboard with a KRW 228M-KRW 257M median-price filter.

KRW 200M Cash: Compare Transactions Around KRW 450M-KRW 510M

The safer search range is about KRW 457.14M-KRW 514.29M in this example. Because cash and LTV remain binding, recalculate income and existing debt before comparing real transactions.

Check actual apartment transactions in this price range: Open the dashboard with a KRW 457M-KRW 514M median-price filter.

KRW 300M Cash: Check the DSR Bottleneck First

More cash does not raise the range without limit. In this example, DSR caps the safer search range at about KRW 478.77M-KRW 538.61M, so check DSR before reviewing actual complexes.

Check actual apartment transactions in this price range: Open the dashboard with a KRW 479M-KRW 539M median-price filter.

Example: Testing a KRW 600M Target Apartment

Assume the target apartment price is KRW 600M, LTV is 70%, and extra costs are 5%.

| Cash on hand | Required loan | Max loan by LTV | Required cash | Cash surplus or gap | Result |

|---|---|---|---|---|---|

| KRW 100M | KRW 530M | KRW 420M | KRW 210M | -KRW 110M | Not viable |

| KRW 200M | KRW 430M | KRW 420M | KRW 210M | -KRW 10M | Near limit |

| KRW 300M | KRW 330M | KRW 420M | KRW 210M | +KRW 90M | Passes input checks |

KRW 200M looks close, but it is still short under the LTV/cash check. A small change in price, reserve cash, LTV input, or transaction cost rate can move the result from "near limit" to "not viable."

What If You Keep Reserve Cash?

Leaving emergency cash outside the purchase budget reduces the cash available to the calculator. This is usually more realistic than putting every won into the home purchase.

| Gross cash | Reserve cash | Cash used in calculation | Cash/LTV price limit |

|---|---|---|---|

| KRW 200M | KRW 0 | KRW 200M | KRW 571.43M |

| KRW 200M | KRW 30M | KRW 170M | KRW 485.71M |

| KRW 300M | KRW 50M | KRW 250M | KRW 714.29M |

Use the reserve cash field in the DSR/LTV Calculator when you want the result to reflect liquidity after closing.

Easy Mistake

"If my income passes DSR, the rest should be fine."

Not necessarily. DSR tests repayment capacity. LTV tests the loan-to-home-price ratio. The cash check tests whether you can cover down payment and transaction costs. A Korean apartment purchase needs all three to work together.

Practical Checklist

- Enter annual income, current debt, DSR, and LTV manually.

- Enter cash on hand after subtracting emergency reserve.

- Add a transaction cost rate instead of assuming the purchase price is the only cost.

- Test one target apartment price, then lower it until the result is no longer tight.

- Use the safer search range in the Real Estate Dashboard, not only the absolute maximum price.

- Treat the result as a pre-check, not as a lending promise or investment recommendation.

Related Reading

- How to use the apartment dashboard for a home-buying goal

- Mortgage risk checklist before buying

- Passing DSR but still blocked by LTV and cash

FAQ

What apartment price can KRW 100M of cash support?

Under this article's 70% LTV and 5% transaction-cost assumptions, the cash/LTV price limit is about KRW 285.71M. Income, existing debt, DSR, and actual costs still need separate review.

Does a higher LTV always mean I can buy a more expensive apartment?

No. A higher LTV does not remove DSR, income, existing debt, cash, collateral, or lender-review constraints. Another condition may become the binding limit.

What happens if I do not pass the DSR check?

If repayment capacity is insufficient under the DSR input, available cash or LTV room may not support the required mortgage. A lower target price or a review of the actual applicable conditions may be necessary.

Why should transaction costs be calculated separately?

Acquisition tax, brokerage fees, moving, repairs, and other costs may require cash beyond the purchase price. Ignoring them can understate the cash needed after closing.

Why can the table differ from the actual purchase budget?

The table is a simulation using fixed LTV, cost, income, and DSR inputs. Actual affordability can differ because of existing debt, recognized income, rates, collateral valuation, lender review, and actual costs.

Bottom Line

Run your own numbers in the DSR/LTV Calculator, then compare the safer search range in the Real Estate Dashboard. The useful workflow is not "Can I borrow the maximum?", but "Which price band still leaves room after debt, cash, LTV, costs, and real market prices?"