Korea's DSR rule limits mortgage borrowing capacity by looking at how much annual income can safely support annual debt payments. In a simple DSR 40% example, annual principal-and-interest payments are capped at 40% of recognized annual income, so higher income, lower existing debt, lower interest rates, and longer terms can support a larger mortgage estimate.

This article is educational and simplified. It is not Korean mortgage advice, policy automation, or a lender approval estimate. Actual borrowing limits can differ because of lender review, recognized income, existing debt, credit profile, collateral valuation, location, regulation, and policy changes.

Quick Answer

| Question | Short answer |

|---|---|

| What is DSR? | Debt Service Ratio. It compares annual debt payments with annual income. |

| What does DSR 40% mean here? | In this simplified example, annual debt payments are limited to 40% of annual income. |

| What changes mortgage capacity? | Income, existing debt, interest rate, loan term, repayment method, LTV, cash, and lender rules. |

| Is this a final loan approval? | No. It is an educational estimate only. |

Use the DSR/LTV Calculator to enter your own income, existing debt, cash, LTV, interest rate, and target home price.

How the DSR 40% Rule Works

The basic logic is:

Annual debt payment capacity = Recognized annual income x DSR limit

Monthly payment capacity = Annual debt payment capacity / 12

Mortgage principal estimate = Loan amount supported by that monthly payment

For example, if annual income is KRW 60 million and the DSR limit is 40%, the annual payment room is KRW 24 million. That equals KRW 2 million per month before considering existing debt.

The mortgage principal that this monthly payment can support depends heavily on the interest rate and loan term.

Simple Assumptions for the Table

The table below uses a simplified example:

| Item | Assumption |

|---|---|

| DSR input | 40% |

| Existing debt | KRW 0 |

| Interest rate | 4.0% per year |

| Loan term | 30 years |

| Repayment method | Equal monthly principal-and-interest payment |

| Excluded | LTV, cash on hand, transaction costs, credit review, collateral valuation, location-specific rules |

These figures are for education only. They are not a bank quote and not a guarantee.

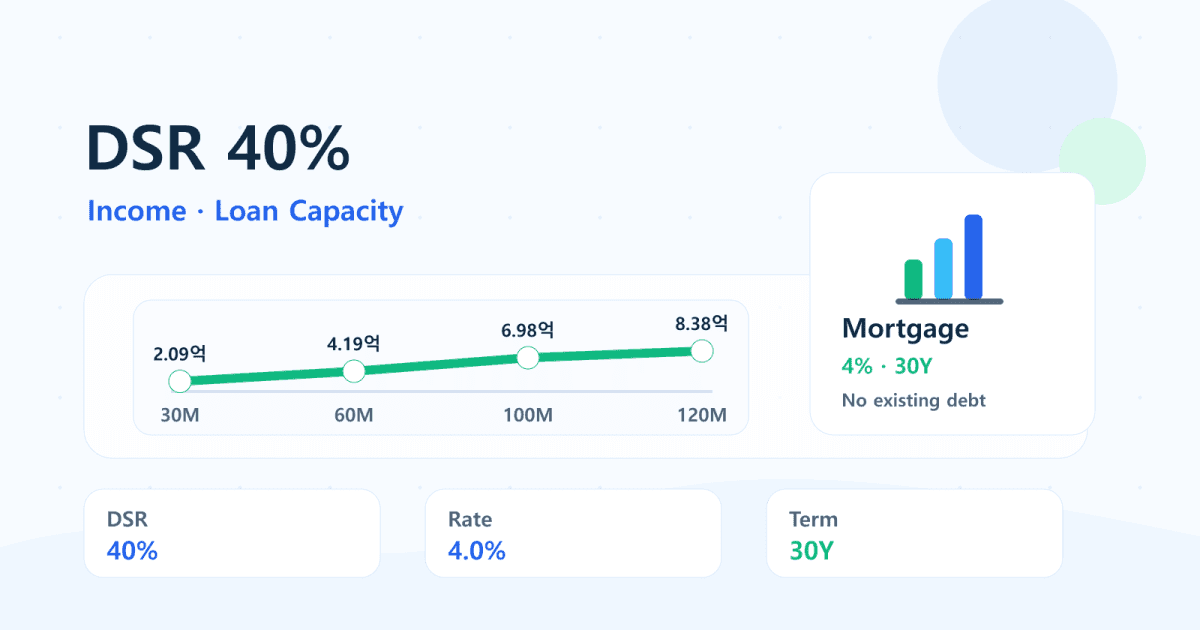

Income Example Table: DSR 40% Mortgage Capacity

| Annual income | Annual payment capacity | Monthly payment capacity | Estimated mortgage principal |

|---|---|---|---|

| KRW 30M | KRW 12.00M | KRW 1.00M | KRW 209.46M |

| KRW 40M | KRW 16.00M | KRW 1.33M | KRW 279.28M |

| KRW 50M | KRW 20.00M | KRW 1.67M | KRW 349.10M |

| KRW 60M | KRW 24.00M | KRW 2.00M | KRW 418.92M |

| KRW 70M | KRW 28.00M | KRW 2.33M | KRW 488.74M |

| KRW 80M | KRW 32.00M | KRW 2.67M | KRW 558.56M |

| KRW 100M | KRW 40.00M | KRW 3.33M | KRW 698.20M |

| KRW 120M | KRW 48.00M | KRW 4.00M | KRW 837.84M |

The table shows why income-based borrowing capacity rises with recognized income. But it still only captures the DSR side. A buyer can pass DSR and still be limited by LTV, cash, transaction costs, or lender review.

Why Existing Debt Can Reduce the Limit

Existing debt payments consume DSR room before a new mortgage is added.

Using annual income of KRW 60 million, DSR 40%, 4.0% rate, and a 30-year term:

| Existing monthly debt payment | Remaining mortgage payment room | Estimated new mortgage principal |

|---|---|---|

| KRW 0 | KRW 2.00M | KRW 418.92M |

| KRW 0.50M | KRW 1.50M | KRW 314.19M |

| KRW 1.00M | KRW 1.00M | KRW 209.46M |

| KRW 1.50M | KRW 0.50M | KRW 104.73M |

This is why a buyer with the same income can have a very different mortgage capacity if they already have credit loans, auto loans, student loans, or other monthly debt obligations.

DSR Is Not the Same as LTV

DSR tests income-based repayment capacity. LTV tests the loan amount relative to the property value.

| Constraint | What it checks | Example question |

|---|---|---|

| DSR | Can income support the annual debt payment? | Can this income support the monthly mortgage payment? |

| LTV | Is the loan too large relative to the home price? | If the home costs KRW 600M, how much can be borrowed? |

| Cash | Is there enough cash for down payment and costs? | Does the buyer have enough cash after fees and reserves? |

| Lender review | Does the borrower and property pass underwriting? | How does the bank recognize income, debt, credit, and collateral? |

If you want to check all three major constraints together, use the DSR/LTV Calculator.

Example: Income, Cash, LTV, and Home Price

Assume:

- annual income: KRW 60M

- cash on hand: KRW 200M

- DSR input: 40%

- LTV input: 70%

- rate and term: 4.0%, 30 years

- transaction cost buffer: simplified

| Item | Result |

|---|---|

| DSR-based mortgage capacity | KRW 418.92M |

| Maximum home price from 70% LTV alone | about KRW 598.46M |

| Home price if cash is the main constraint | lower after transaction costs and reserves |

| Main lesson | DSR may pass while cash/LTV still limits the purchase |

After estimating a safer home-price range, compare it with actual transaction data in the Korean Real Estate Dashboard.

Related guides:

- How Much Can a 1pp Rate Increase Reduce Korean Mortgage Capacity?

- Passing DSR but Still Blocked? Understanding LTV, Cash, and Cost Bottlenecks

- Mortgage Risk Checklist Before Buying a Korean Apartment

- Cash KRW 100M, 200M, 300M: What Apartment Budget Can It Support in Korea?

Calculator Workflow

Use this sequence after reading the table:

- Enter recognized annual income.

- Add existing monthly debt payments.

- Set the DSR input.

- Set the interest rate and loan term.

- Add available cash and LTV.

- Compare the result with target home prices.

- Check actual transaction ranges in the Real Estate Dashboard.

Start here: DSR/LTV Calculator.

Bottom Line

Korea's DSR 40% rule is best understood as an income-based repayment capacity test. It can estimate how much mortgage principal a given income may support, but it is only one part of affordability. Existing debt, interest rates, loan term, LTV, cash, property value, and lender review can all change the final outcome.

FAQ

What does DSR mean in Korea?

DSR means Debt Service Ratio. It compares annual debt payments with annual income. In this article, DSR 40% is used as a simplified input example.

Is DSR 40% a guaranteed mortgage limit?

No. The table is educational and simplified. Actual mortgage limits can differ because of recognized income, existing debt, credit review, collateral valuation, lender policy, and regulation.

Why does a higher interest rate reduce borrowing capacity?

At the same monthly payment capacity, a higher interest rate leaves less room for principal repayment. That lowers the estimated mortgage principal.

How does existing debt affect DSR?

Existing debt payments use part of the annual debt-payment room first. The remaining room is what can support a new mortgage payment.

Which matters more, DSR or LTV?

Both can matter. DSR can be the binding limit for income, while LTV and cash can be the binding limits for the property price and down payment.