A one percentage point rate move can look small in a headline. In a Korean mortgage affordability calculation, it can move the loan capacity by tens of millions of KRW.

This article compares 3%, 4%, 5%, and 6% rates using KRW 60 million of annual income, a user-entered DSR 40%, no existing debt, and a 30-year equal-payment mortgage. To test your own target apartment, use the DSR/LTV Calculator.

Once you have a safer search range, compare it with actual transaction bands in the Real Estate Dashboard. This is a simulation, not policy automation or lender approval.

Quick Summary

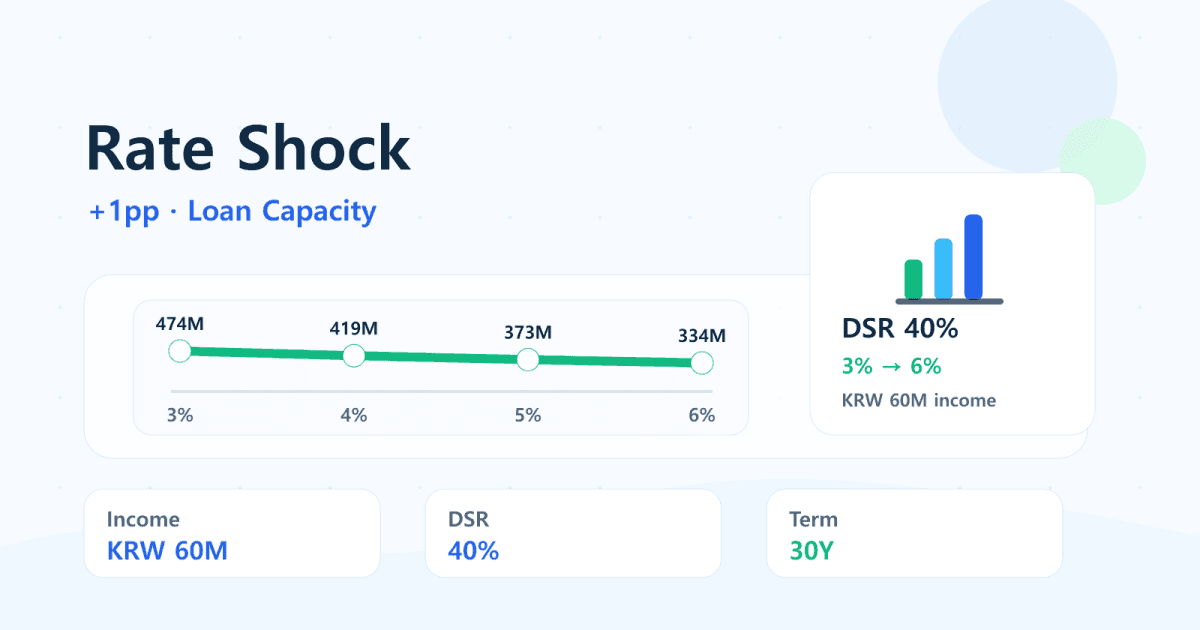

- KRW 60 million of annual income at DSR 40% gives about KRW 2 million of monthly payment capacity.

- At 3%, that supports about KRW 474.38 million of loan principal.

- At 4%, it falls to about KRW 418.92 million.

- A target home that looks close at 4% can become difficult at 5%.

- The FinMap calculator’s sensitivity table lets you compare base, +1pp, and +2pp scenarios using your inputs.

- After the calculation, use the Real Estate Dashboard to check whether that safer range exists in real Seoul, Gyeonggi, or Incheon transactions.

Assumptions

| Item | Input |

|---|---|

| Annual income | KRW 60M |

| DSR | 40% |

| Existing debt | KRW 0 |

| Cash example | KRW 200M |

| Target home example | KRW 600M |

| LTV / closing cost input | 70% / 5% |

| Loan term | 30 years |

| Repayment method | Equal monthly principal-and-interest payment |

The calculator does not automatically update Korean mortgage policy. It uses the DSR, LTV, rate, term, cash, and target price you enter.

Loan Capacity by Rate

| Rate | Monthly payment capacity | Estimated loan capacity | Drop from prior rate | Drop rate |

|---|---|---|---|---|

| 3% | KRW 2.00M | KRW 474.38M | - | - |

| 4% | KRW 2.00M | KRW 418.92M | KRW 55.46M | 11.7% |

| 5% | KRW 2.00M | KRW 372.56M | KRW 46.36M | 11.1% |

| 6% | KRW 2.00M | KRW 333.58M | KRW 38.98M | 10.5% |

With the same monthly payment capacity, a higher rate leaves less room for principal. That is why rate sensitivity matters before a home search becomes too specific.

Same KRW 300M Loan, Different Monthly Payments

| Rate | Monthly payment | Annual payment |

|---|---|---|

| 3% | KRW 1.27M | KRW 15.18M |

| 4% | KRW 1.43M | KRW 17.19M |

| 5% | KRW 1.61M | KRW 19.33M |

| 6% | KRW 1.80M | KRW 21.58M |

The difference between 3% and 6% is about KRW 530,000 per month for the same KRW 300 million loan. That is real household cash flow, not just a spreadsheet detail.

Target Home Check: KRW 600M Apartment

Assume KRW 200 million of cash, 70% LTV, 5% closing costs, and a KRW 600 million target home.

| Rate | DSR loan capacity | Required target loan | LTV max loan | Decision |

|---|---|---|---|---|

| 3% | KRW 474.38M | KRW 430.00M | KRW 420.00M | Caution |

| 4% | KRW 418.92M | KRW 430.00M | KRW 420.00M | Caution |

| 5% | KRW 372.56M | KRW 430.00M | KRW 420.00M | Not possible |

| 6% | KRW 333.58M | KRW 430.00M | KRW 420.00M | Not possible |

At 4%, the case is close but short on DSR, LTV, and cash. At 5%, the DSR shortfall becomes much larger. In the calculator, “Caution” is not a lender signal; it simply means the input-based shortfall is within 5%.

Misunderstanding Box: Lower Home Prices Do Not Automatically Offset Higher Rates

Misunderstanding: “If rates rise, home prices may fall, so the payment problem fixes itself.”

Not necessarily. Your borrowing capacity can fall before the market price adjusts enough. Also, cash, LTV, and closing-cost constraints may still block the target home even if the price is slightly lower.

The safer workflow is to run the DSR/LTV Calculator under +1pp and +2pp rate assumptions, then compare the safer price range in the Real Estate Dashboard.

Rate Sensitivity Checklist

- Check the base rate, +1pp, and +2pp scenarios.

- Include existing monthly debt payments.

- Enter the target home price and read the Possible / Caution / Not possible decision.

- Compare the 80-90% safer range with real transaction prices.

- Do not treat DSR approval as household comfort.

- If the mortgage rate can reset, understand the reset period and discount conditions.

Related Reading

- DSR 40% by Income: Korean Mortgage Capacity Table

- How to Use the Apartment Dashboard for a Home-Buying Goal

- Cash KRW 100M, 200M, 300M: What Apartment Budget Can It Support?

Bottom Line

A 1pp mortgage rate move can change both loan capacity and target-home feasibility. For DSR-constrained buyers, rate sensitivity is part of the home budget, not a separate macro topic.

Run your assumptions in the DSR/LTV Calculator, then open the Real Estate Dashboard to see whether your safer range matches real KRW apartment transactions.

FAQ

Why does a 1pp rate increase reduce loan capacity?

Because the same monthly payment must cover more interest, leaving less room for principal.

Does the FinMap sensitivity table apply Korean policy automatically?

No. It recalculates the same formula from the DSR, LTV, rate, term, cash, and target price you enter.

What does Caution mean?

It means at least one DSR, LTV, or cash check fails, but the maximum shortfall is within 5% in the simulation. It is not a lender approval signal.

Should a higher rate always lower my search budget?

Often it does, but the bottleneck can be DSR, LTV, or cash depending on your inputs. Run the calculator instead of assuming one answer.

Why use the dashboard after the calculator?

The calculator gives your budget range. The dashboard shows whether real Seoul, Gyeonggi, or Incheon transactions exist in that range.