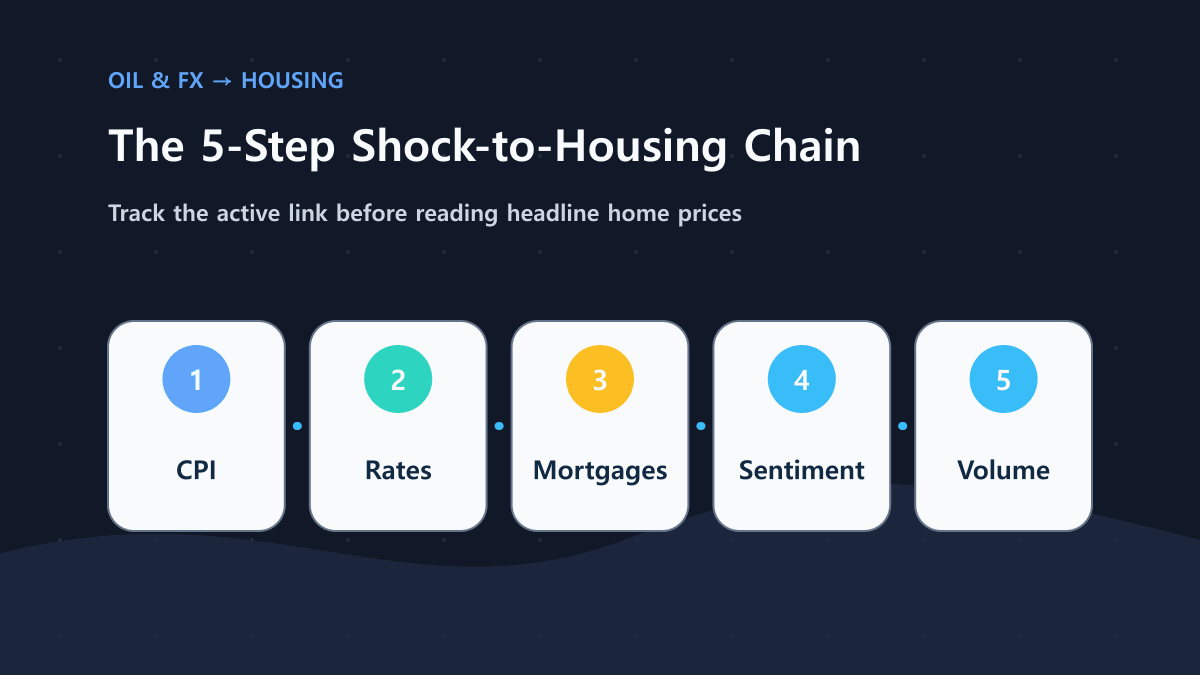

- Housing doesn’t react to geopolitics on impact; it transmits through CPI → rates → mortgages → sentiment → volume, often with lags and regime flips.

- Oil and FX shocks typically hit household budgets and inflation expectations first, then reshape the rate path that lenders price into mortgage offers.

- In housing, transaction volume tends to break before headline prices, because prices are sticky while decisions can pause instantly.

- After volume turns, the next tell is not “average price,” but price distribution shifts: which segments transact, and which vanish.

- The practical question is not “will prices go up or down,” but which link in the chain is tightening and what signal confirms it.

- A shock that raises CPI can still lead to weak housing even if nominal prices don’t fall quickly, because mortgage affordability compresses first.

- The same headline can flip outcomes: when rates peak or FX stabilizes, volume can recover while prices remain range-bound.

- You can replace doom-scrolling with a 10-minute dashboard routine using South Korea Apartment Transaction Dashboard to track volume and distribution.

- This post avoids predictions and recommendations; it provides observable triggers and response rules you can apply to any news cycle.

ECONOMICS · HOUSING TRANSMISSION

“A geopolitical flare-up happened—does that mean Seoul home prices must fall (or must rise)?”

That shortcut creates whiplash because housing rarely moves on one headline. It usually moves through a chain: CPI → rates → mortgages → sentiment → volume, and the first break is often volume, not price.

This guide turns news fear into a transmission map + observable triggers + simple rules, and shows how to monitor the chain in South Korea Apartment Transaction Dashboard.

- A 5-step mechanism you can reuse for oil/FX/geopolitics shocks

- How to separate volume breaks first from price distribution shifts later

- A 10-minute dashboard routine you can repeat without forecasting

Scope/limits: No price targets, no buy/sell calls, and no market timing advice. This is interpretation + monitoring rules.

Housing headlines often create binary thinking: “war means housing down” or “risk means people buy real assets.” Real markets are more mechanical. Seoul–Gyeonggi–Incheon housing responds to affordability, credit conditions, and decision timing. Those variables don’t jump instantly; they transmit.

This post is designed for readers who want a stable framework. The target is not predicting prices. The target is building a rule that answers: “Which link is moving, what should I check next, and what would change my interpretation?”

The 5-step chain: how oil and FX shocks reach housing

A geopolitical event becomes a housing event through intermediate prices and policy expectations. The simplest map is the 5-step chain below.

- CPI channel: oil and FX move import costs and energy costs, shaping inflation prints and expectations

- Rates channel: policy expectations and term premia reprice yields, which feed into lending benchmarks

- Mortgage channel: lenders reprice borrowing costs, tightening affordability and approval psychology

- Sentiment channel: uncertainty shifts buyer and seller behavior (pause, wait, or accept)

- Volume channel: transactions decline or recover first; prices follow later, often as distribution shifts

Three core variables that tell you where the chain is tightening

To keep the chain operational, track three variables early. Each is a “definition / how to observe / limitation” set.

Variable 1: Inflation pressure (CPI vs expectations)

Definition: what households pay today and what markets expect tomorrow.

Observe: CPI prints, energy-sensitive components, and inflation expectations proxies.

Limitation: inflation can rise while real purchasing power falls; the housing impact depends on rates and credit response.

Variable 2: Rates and real borrowing cost

Definition: the path of market rates and how it translates into borrowing costs.

Observe: yield moves, rate volatility, and the gap between “policy narrative” and “market pricing.”

Limitation: “policy rate unchanged” can still mean borrowing costs rise if market rates and spreads widen.

Variable 3: Credit availability and decision timing

Definition: the ease with which households convert intent into a financed purchase.

Observe: approval anecdotes, bank posture, and the housing market’s volume response.

Limitation: credit tightening can show up first as fewer transactions, not lower listed prices.

The dashboard lens: volume breaks first, distribution shifts later

Housing is a slow market with sticky prices. A buyer can pause instantly, but a seller may not cut the ask price quickly. This is why the first break is often volume.

Use South Korea Apartment Transaction Dashboard as a monitoring tool to separate two phases:

Phase A: Volume breaks first

What it means: decision deferral is rising. Buyers step back; sellers hold asks.

What to look for: transaction counts declining across segments or concentrated in riskier segments.

Phase B: Price distribution shifts later

What it means: the market is still transacting, but not evenly. Some segments trade; others disappear.

What to look for: median vs average divergence, fewer high-end prints, more “lower band” transactions, or narrower segment participation.

This separation prevents a common mistake: interpreting a flat average price as “nothing is happening” while the market is quietly freezing.

Table 1) The required mapping: shock → impact → housing channel → dashboard signal

| Shock (oil / FX / rates) | Household / business impact (first) | Housing channel (transmission) | Dashboard signal to watch |

|---|---|---|---|

| Oil spikes (energy costs up) | transportation and utility burden rises; inflation sentiment worsens | CPI pressure → rate path reprices → affordability tightens | Volume softens first; distribution tilts toward “only affordable segments” transacting |

| KRW weakens vs USD (FX pressure) | import costs rise; uncertainty increases; business costs can lift | CPI expectations up → yields/spreads up → mortgage offers reprice | Volume drop precedes price changes; median may move before average |

| Market rates rise (borrowing cost up) | monthly payment shock; pre-approval confidence drops | mortgage affordability compresses → buyer pause → fewer closings | A broad-based volume decline across Seoul/Gyeonggi/Incheon |

| Rate volatility rises (uncertainty up) | decision deferral increases even if rate level stable | sentiment pause → fewer bids/closings | Volume falls while prices look sticky; time-to-close perception worsens |

| FX/oil stabilize (pressure eases) | budget shock eases; expectations calm | sentiment improves → volume returns → distribution broadens | Volume recovers first; distribution widens before headline prices move |

Interpretation:

- The table is not a prediction engine; it is a “next check” engine.

- If you see the volume signal, you treat it as an early confirmation that the chain has reached housing decisions.

- If distribution shifts but volume is stable, the market may be segmenting rather than collapsing.

A second table to keep you from over-reading average prices

Average prices are fragile in thin markets. When volume drops, averages can be biased by which transactions still happen.

Table 2) “What you see” vs “what it can mean” in the volume-first phase

| What you see | What it can mean | What to confirm next (dashboard-first) |

|---|---|---|

| Volume down, average price flat | sticky asks; fewer transactions; not enough data to move averages | Check distribution or median indicators; see which segments stopped trading |

| Volume down, median down but average flat | high-end prints disappeared; lower band dominates | Confirm share of lower-price bands; watch segment participation |

| Volume stable, distribution narrows | market is selective; only certain properties transact | Check which regions/segments still trade; note widening vs narrowing trend |

| Volume up, distribution broadens | confidence returning; more segments participating | Confirm it’s broad-based, not just one niche |

Interpretation:

- Thin volume makes “average price” noisy; distribution signals often tell the truth earlier.

- The practical approach is sequential: volume → distribution → price level interpretation.

A 3-scenario table with flip triggers (required for economic-info posts)

The same geopolitical headline can land differently depending on whether the economy is in a tightening phase, a peak-rate phase, or a stabilization phase. You don’t need to forecast which scenario will win. You need flip triggers.

Table 3) Base / Escalation / Stabilization (with observable triggers)

| Scenario | What dominates | Observable flip triggers | Housing path (typical order) | Dashboard expectation |

|---|---|---|---|---|

| Base (contained shock) | mild CPI pressure, limited rate repricing | oil/FX volatility normalizes; yields stable | sentiment cautious → volume soft but not collapse | modest volume dip; limited distribution shift |

| Escalation (inflation + rates bite) | CPI pressure + borrowing cost repricing | oil stays elevated; FX weak; yields/spreads rise | mortgage shock → sentiment pause → volume break | volume breaks first; distribution shifts toward cheaper bands |

| Stabilization (pressure eases) | uncertainty down; affordability stops worsening | FX/oil stabilize; yields peak/roll; spreads calm | sentiment improves → volume recovers → distribution broadens | volume rebounds before headline prices re-rate |

Interpretation:

- Your job is labeling the scenario from triggers, not guessing price direction.

- If mortgage costs and volatility keep rising, the market tends to freeze before it reprices.

- If volatility eases and borrowing costs stop worsening, volume can recover even if prices do not surge.

Misconception box: “war means housing must fall (or must rise)”

Misconception: “Geopolitics automatically means housing down” or “geopolitics automatically means people rush into housing.”

Why it fails: Housing is mediated by CPI, rates, and mortgage affordability. A shock can be inflationary, tightening borrowing costs and freezing decisions, or it can fade quickly, leaving volume intact. The first reaction is often decision timing, not price repricing.

Check this instead:

1) Did borrowing costs worsen, or did volatility just rise?

2) Did volume break first, and is distribution shifting?

Case study 1: Oil + FX shock, rates reprice, volume freezes before prices move

Setup (illustrative, not a forecast):

- Oil rises and FX weakens, lifting import and energy cost concerns.

- Market rates and mortgage offers adjust upward.

- Buyers step back to avoid “buying into uncertainty,” while sellers hesitate to cut asks.

Expected housing sequence in this regime:

- Mortgage affordability becomes the constraint.

- Sentiment shifts from “shop” to “wait.”

- Transactions fall; closing becomes selective.

- Distribution shifts appear (fewer high-end transactions; more activity in lower/“affordable” bands).

Dashboard application:

- In South Korea Apartment Transaction Dashboard, start with volume: does it drop across Seoul/Gyeonggi/Incheon or only in specific segments?

- Then check distribution: does the market narrow into certain price bands, or does participation stay broad?

Practical response rule:

- If volume breaks but distribution is stable, treat it as a pause regime and monitor for stabilization triggers.

- If volume breaks and distribution shifts toward lower bands, treat it as a tightening regime and prioritize affordability and buffer checks.

Case study 2: Volatility fades, rates stop worsening, volume recovers while prices remain sticky

Setup (illustrative, not a forecast):

- Oil volatility eases; FX stabilizes; rates stop rising.

- Buyers regain confidence that “the worst of the rate shock may be past.”

- Sellers still anchor to past prices, so headline prices do not jump.

Expected housing sequence:

- Volume returns first.

- Distribution broadens as more segments transact again.

- Price levels may remain range-bound for a while because repricing takes time.

Dashboard application:

- In South Korea Apartment Transaction Dashboard, look for volume improvement first.

- Then look for distribution broadening: more segments participating is stronger than a single “average price” tick.

What to read next (mid-article internal links that make the chain click)

These two pieces help you interpret the rates link in the chain without relying on headlines:

- Understand how policy rates, market rates, and borrowing costs connect (so you track the right rate)

- See why the U.S. 10Y yield (TNX) acts as a discount-rate backbone that can spill into global conditions

A practical monitoring plan: weekly signals vs monthly confirmations

You don’t need daily monitoring. Housing reacts slowly; your monitoring should be structured.

Weekly signals (fast-moving):

- oil and FX volatility tone (shock intensity)

- rate momentum (worsening vs stabilizing)

- the first housing tell: volume trend

Monthly confirmations (slow-moving):

- distribution shifts (participation narrowing or broadening)

- persistence of affordability pressure

- whether volume decline is broad-based or localized

Checklist: a quick “shock-to-housing” triage

- □ Identify the shock: oil, FX, or rates (or a combo)

- □ Label the active link: CPI pressure, rate repricing, mortgage shock, sentiment pause

- □ Check volume first in South Korea Apartment Transaction Dashboard

- □ If volume is down, check distribution next (median vs average, participation breadth)

- □ Write one sentence: “The chain is currently at step ___, so I will monitor ___ next.”

Conclusion: the 10-minute dashboard routine (mandatory)

When a scary headline hits, you don’t need a forecast. You need a routine that turns noise into signals.

Use this 10-minute flow with South Korea Apartment Transaction Dashboard:

- □ Open South Korea Apartment Transaction Dashboard and select Seoul, Gyeonggi, and Incheon views (one by one, not averaged together).

- □ Check the last 1–6 months: did transaction volume break first (downtrend) or recover first (uptrend)?

- □ If volume is down, ask: is it broad-based or limited to certain segments/areas?

- □ Then check price distribution: are fewer segments trading, is the market narrowing into lower bands, or is participation broadening?

- □ Avoid “average-price anchoring” when volume is thin; prioritize distribution and participation signals.

- □ Map the observation back to the chain: CPI → rates → mortgages → sentiment → volume.

- □ Write a response rule: “If volume keeps falling for 2–3 readings, I will re-check my cash buffer and debt stress before making big decisions.”

- □ Repeat weekly, not daily, unless conditions are clearly escalating.

To make the routine more complete, connect the macro inputs that often drive the first two links in the chain:

- Learn how USD/KRW moves can shape Korea risk sentiment and spill into financial conditions

- See how WTI oil shocks typically transmit into Korea markets and inflation tone

- Set a cash buffer by risk (so a shock doesn’t force bad timing decisions)

Optional official references (for verification)

- Bank of Korea (policy rate, monetary policy materials): https://www.bok.or.kr

- Korea Real Estate Board (market statistics and reference materials): https://www.reb.or.kr

- Statistics Korea (CPI and related datasets): https://kostat.go.kr

FAQs

1) Does geopolitics directly move Seoul home prices?

Usually not directly. Housing tends to react through intermediate steps: CPI pressure, rate repricing, mortgage affordability, sentiment, and then transaction volume. This is why volume can move first while headline prices look unchanged.

2) Why does transaction volume often break before prices?

Prices are sticky due to listing anchors and seller resistance, while buyers can pause instantly when uncertainty rises or financing costs jump. Volume is the market’s quickest “decision timing” indicator. Distribution changes often come next.

3) What does “price distribution shift” mean in housing?

It means the market is still trading, but not evenly. Certain segments transact while others disappear, which can distort averages. Looking at medians, participation breadth, and band concentration often reveals the shift earlier than headline prices.

4) How do oil shocks influence housing in Korea?

Oil can raise energy and import costs, shaping CPI and inflation expectations. That can influence the rate path and mortgage pricing, which affects affordability and sentiment. The housing impact often appears first as volume softness rather than immediate price moves.

5) How does FX (USD/KRW) connect to housing transmission?

FX pressure can influence import costs and risk sentiment, which can affect inflation tone and financial conditions. Housing is affected when those conditions translate into mortgage affordability and decision pauses. The key is observing which step is active, not predicting FX.

6) What’s the most important dashboard signal to check first?

Start with transaction volume. If volume is stable, price interpretation is more reliable. If volume is thin, treat averages cautiously and check distribution and participation next.

7) Can housing volume recover while prices stay flat?

Yes. When volatility fades and borrowing costs stop worsening, buyers can return first, lifting volume. Prices can remain sticky because repricing is slower and depends on negotiation and inventory. Distribution broadening can be an early sign of normalization.

8) How often should I run the 10-minute routine?

Weekly is usually enough because housing responds slowly. Daily checks often increase anxiety without adding signal. Increase frequency only if triggers suggest escalation, such as persistent rate repricing and broad-based volume deterioration.