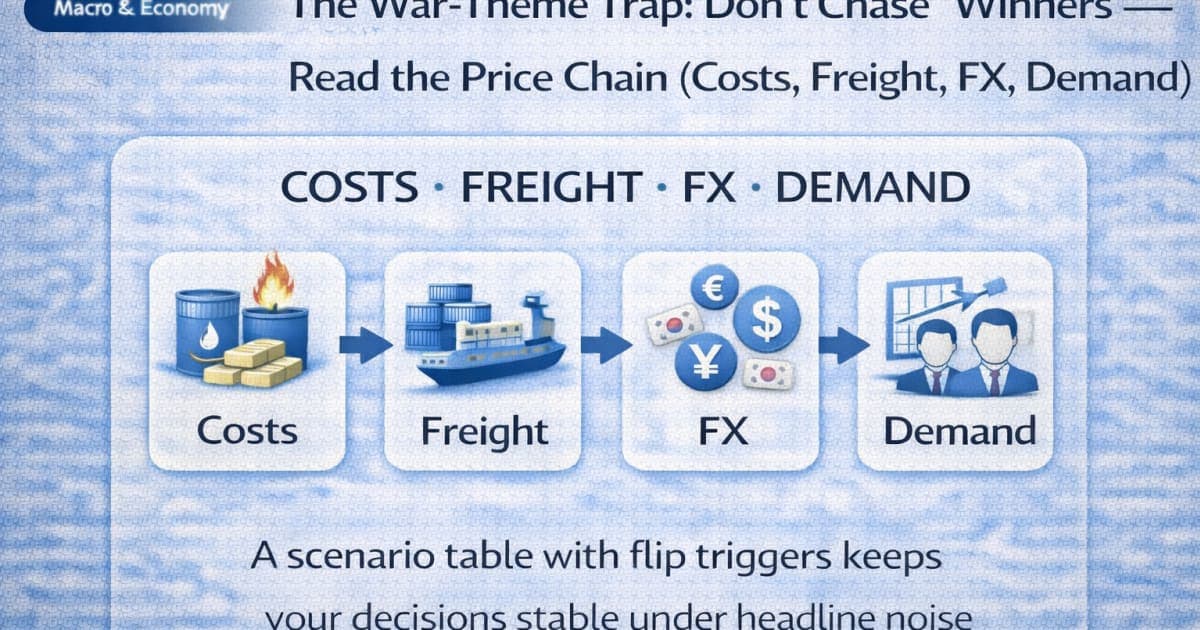

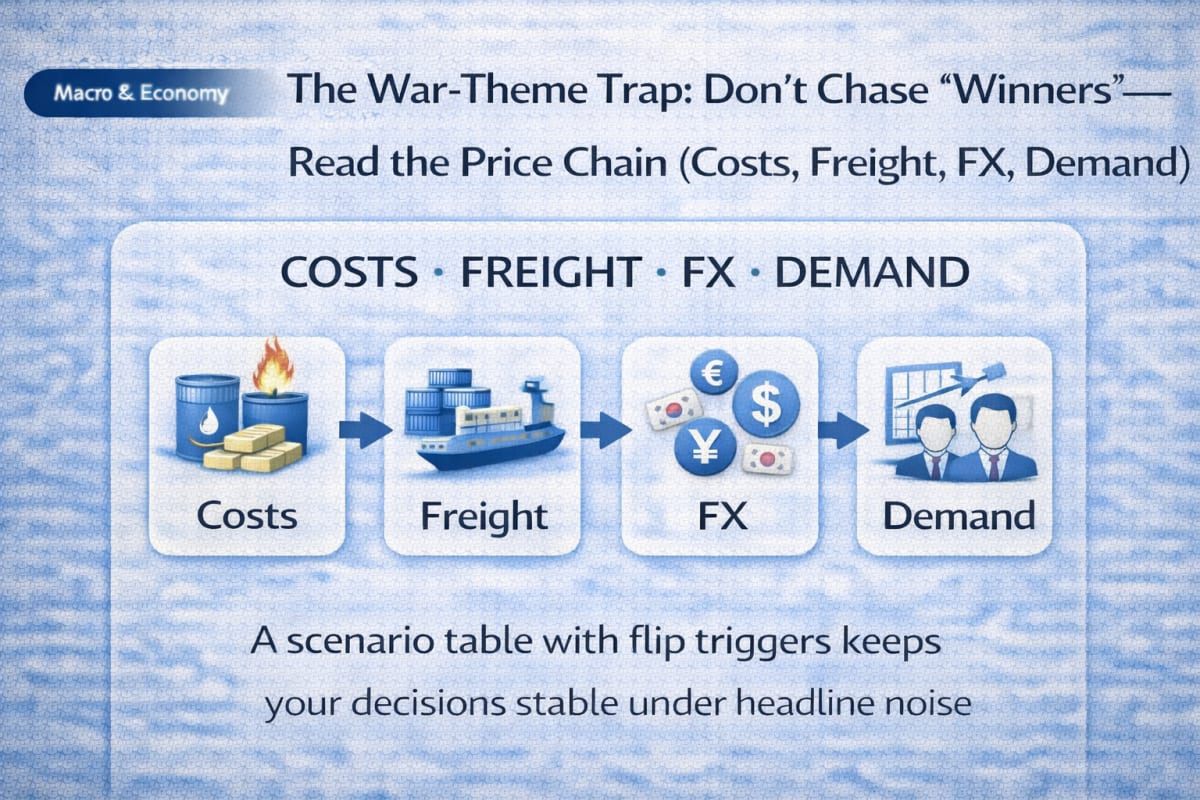

- War headlines don’t create “winners” by sector name; they reprice a cost–freight–FX–demand chain, and the market often moves before earnings do.

- A theme rally can be liquidity + positioning rather than an improvement in margins, so chasing without a chain check is how people get trapped.

- The fastest movers are usually freight/insurance premia and FX volatility; the slowest movers are usually contracts, backlogs, and realized margins.

- “Defense wins” is not a rule: procurement cycles, input costs, FX exposure, and delivery timing can turn a headline into a margin squeeze.

- “Shipping wins” is also not a rule: higher freight rates can come with higher fuel costs, weaker demand, and policy frictions that compress net benefit.

- The most useful decision skill is separating price moves from margin transmission, then updating your view only when “flip triggers” appear.

- In Korea-linked investing, USD/KRW (KRW per USD) can act as a multiplier on the chain, changing who wins even inside the same industry.

- You don’t need a prediction; you need a rules-based reading routine for costs, freight, FX, and demand—then a plan for what you do in each state.

- If you can explain who pays the bill (customers, suppliers, governments, or shareholders), you can avoid most war-theme mistakes.

ECONOMICS · PRICE CHAIN

“There’s a war headline—so which sector is the winner?”

That question is costly because themes can run on narratives while margins move on contracts, freight, FX, and demand—and those don’t reprice on the same clock.

This post gives you a price-chain framework and a rules-based action plan: what to check, in what order, and what signals justify changing your stance.

- A 4-link chain: input costs → freight/insurance → FX → margins & demand

- Tables that separate “theme overheat” vs “real transmission” + flip triggers

- Two case studies (defense vs shipping/commodities) and a checklist you can reuse

Scope/limits: no stock/ETF picks and no short-term predictions. Focus is “mechanism → interpretation → your rules.”

Replace “who benefits?” with “how does the price chain transmit into margins?”

Theme investing often starts with a label: defense, energy, shipping, commodities.

But profits don’t come from labels—they come from margins, and margins come from transmission.

A war-related shock can move four links quickly:

- Input costs (energy, metals, components)

- Freight & insurance premia (war-risk, rerouting, lead times)

- FX and funding (USD strength, local currency weakness, hedging costs)

- Demand & pricing power (how much can be passed on without losing volume)

If you can’t say which link is moving first and who ultimately pays, “winner chasing” is mostly guessing.

Three core variables that simplify war-theme investing

To avoid narrative traps, start with only three variables. Each has a definition, what to observe, and what can mislead you.

Variable 1 — Input cost shock (energy & materials)

- Definition: Changes in the cost of energy and raw materials that feed directly into production.

- How to observe: Oil and key commodities, crack/spread indicators, supplier price signals, and (later) cost-of-goods trends.

- Limit: Inventory buffers, fixed-price contracts, and hedges can delay or hide the impact in reported earnings.

Variable 2 — Freight/insurance premium (logistics risk)

- Definition: Extra cost from higher shipping rates, rerouted lanes, longer lead times, and war-risk insurance.

- How to observe: Freight indices, delivery-time proxies, rerouting headlines, and insurance/friction indicators.

- Limit: Freight can help carriers but hurt manufacturers; the same move can be revenue for one industry and cost for another.

Variable 3 — FX multiplier (USD strength, local currency weakness)

- Definition: Currency moves that amplify costs or revenues when invoices and hedges are USD-linked.

- How to observe: USD strength proxies (like DXY), USD/KRW volatility (for Korea-linked exposure), and hedging cost changes.

- Limit: Company-level hedging and natural offsets (USD revenues vs USD costs) can flip the sign of the effect.

The war-theme price chain in one table (and why timing matters)

Here’s the key: markets can reprice link #2 and #3 quickly, while earnings often reflect link #1 and #4 with a lag.

Table 1 — Price chain map: what moves first, who pays, and what can fool you

| Chain link | What typically reprices fast | Who feels it first | How it shows up in margins | Common “trap” / exception |

|---|---|---|---|---|

| Input costs | Spot oil/commodities, spreads | Cost-heavy manufacturers | COGS up → margin down unless pass-through | Inventory/hedges delay pain; contracts can mute spot moves |

| Freight/insurance | Freight rates, rerouting, war-risk premium | Importers/exporters; carriers | Freight cost up (or carrier revenue up) | Freight up can coincide with weaker volumes later |

| FX multiplier | USD strength, local FX volatility | USD invoicers; unhedged firms | USD costs up in local terms; hedges get expensive | Natural hedges can offset; timing differs by hedge structure |

| Demand & pricing power | End-demand and substitution | Consumers; downstream buyers | Pass-through succeeds or fails → margin outcome | Demand can drop after price rises; “revenue up” ≠ “profit up” |

Interpretation (2–3 lines):

- You’re not trying to forecast; you’re trying to identify which link is currently dominant and which link is still lagging.

- Theme rallies often happen when fast links (freight/FX) move, even before slow links (margins, demand) confirm.

- The trap is buying a label while the cost chain is silently working against margins.

The misconception box you must fix before you touch war themes

Why it’s often wrong: Sector labels don’t pay earnings—margins do. Procurement timing, contract clauses, fuel costs, FX exposure, and demand elasticity can turn the same headline into either a margin tailwind or a margin squeeze.

Theme rallies can also be positioning-driven: prices move because flows move, not because profits are locked in.

Instead, check this first (2 lines):

1) Which chain link is moving now (cost, freight/insurance, FX, demand), and who pays it?

2) What “flip trigger” would prove margins are actually improving (not just prices rising)?

Case study comparison: defense vs shipping/commodities (same headline, different profit clocks)

War themes often cluster into two “popular baskets.” The mistake is treating them as the same trade.

- Defense tends to be contract and backlog driven: slower, lumpy, policy-shaped.

- Shipping/commodities tend to be spot and logistics driven: faster, more cyclical, demand-sensitive.

Table 2 — Defense vs shipping/commodities: the margin transmission difference

| Dimension | Defense (procurement/backlog) | Shipping & commodities (spot/logistics) | What to check first | Frequent mistake |

|---|---|---|---|---|

| Reaction speed | Often fast in price, slow in earnings | Often fast in both price and indicators | Price vs earnings clock mismatch | Treating price pop as earnings certainty |

| Key driver | Orders, delivery schedules, contract terms | Freight rates, spot prices, inventory cycles | Contract clauses vs spot indicators | Ignoring contract constraints or fuel costs |

| Margin risk | Input costs + FX + delivery delays | Fuel costs, demand drop, regulatory friction | Net margin after costs | Assuming “higher price” equals “higher profit” |

| “Who pays the bill” | Ultimately taxpayers/budgets, with timing | End users and global supply chain, quickly | Pass-through vs volume loss | Not asking who absorbs cost increases |

Interpretation (2–3 lines):

- Defense can look like a clean “benefit” story, but realization depends on contract structure and timing.

- Shipping/commodities can validate quickly, but the cycle can also reverse quickly if demand weakens.

- Your framework should change by basket: backlog logic vs spot-cycle logic.

Two mini case studies you can reuse as templates (no prediction required)

Case A — Defense rallies, but margins lag

A defense theme can rally on “expected orders,” but margins can lag because:

- delivery is months/years away,

- costs rise faster than contract adjustment clauses,

- FX moves change imported input costs.

If you can’t identify the margin-protection mechanism (indexation, pass-through clauses, natural hedges), treat the rally as a theme move, not a margin lock-in.

Case B — Shipping/freight spikes, but net benefit is capped

Freight rates can spike on rerouting risk, but net benefit can be capped when:

- fuel costs rise at the same time,

- demand softens (volumes drop),

- policy constraints create friction that delays cashflow.

In this template, the “right question” is not “freight up?” but “freight up relative to costs and volume?”

Scenario table with flip triggers: a state machine, not a forecast

Instead of betting on outcomes, define states and update only when observable triggers appear.

Table 3 — Base / Escalation / De-escalation with flip conditions (rules-based)

| State (definition) | Dominant link | What you often see first | Flip trigger (what must change) | Your action rule |

|---|---|---|---|---|

| Base: tense but functioning | Freight/FX volatility | FX and freight move; earnings unchanged | Volatility cools + freight normalizes | Avoid chasing; check chain confirmation weekly |

| Escalation: real supply/logistics strain | Costs + freight together | Input costs rise + lead times worsen | Demand indicators weaken enough to cap pass-through | Prioritize margin resilience over headline winners |

| De-escalation: risk premium fades | Freight/FX mean reversion | Freight falls; FX stabilizes | A second confirmation in demand/pricing power | Reduce theme exposure; return to process-driven allocation |

Interpretation (2–3 lines):

- These are not predictions; they are “if–then” buckets so you don’t improvise under stress.

- Flip triggers prevent emotional updates: you change your stance when the chain changes, not when a headline repeats.

- “De-escalation” is typically the disappearance of stress symptoms, not one announcement.

Theme overheat vs real transmission (the table that stops you from chasing)

War themes feel urgent. This is where rules protect you.

Table 4 — Is it a narrative squeeze or real margin transmission?

| Checkpoint | Narrative/flow-driven overheat | Real transmission (chain confirms) | Default rule |

|---|---|---|---|

| Breadth | Everything “war-related” rises | Mostly names with aligned chain exposure | Don’t buy weakly related tickers |

| Data alignment | Costs/freight/FX don’t confirm | At least 1–2 chain links confirm | No confirmation → no chasing |

| Time horizon | Move happens in hours/days | Evidence builds over weeks/months | Use time-matched data (spot vs earnings) |

| Reversals | One headline reverses the whole move | Reversal follows chain turning | Flip on triggers, not emotions |

Interpretation (2–3 lines):

- Overheat looks like “price without proof.” Transmission looks like “price with chain alignment.”

- You don’t need perfect certainty—just enough confirmation to avoid the worst traps.

- If the chain doesn’t confirm, default to patience.

Korea overlay: why USD/KRW can decide who wins inside the same theme

For Korea-linked investors (KOSPI, Korea exporters/importers), USD/KRW (KRW per USD) often acts as an amplifier:

- USD costs (energy, components, freight) rise in KRW terms when KRW weakens.

- USD revenues can benefit in KRW terms, but only if the company’s USD costs and hedges don’t offset it.

If you want a practical way to map “who benefits / who suffers” when KRW weakens, use these mid-post guides as your checklist layer:

- Who wins/loses when KRW weakens (a sector checklist)

- WTI → Korea macro chain (inflation, FX, rates, earnings)

Two checklists: a 15-minute routine and a “no-chase” gate

Use these when the headline hits and your brain wants a shortcut.

Checklist 1 — The 15-minute “price chain” read

- □ Write the event in one neutral sentence (no adjectives, no outcome guessing).

- □ Identify the first moving link: input costs, freight/insurance, FX, or demand.

- □ Decide “who pays the bill” (customers, suppliers, government budgets, or shareholders).

- □ Check whether the move is faster than earnings can plausibly respond (theme risk).

- □ Define one flip trigger that would confirm margins (not just prices).

Checklist 2 — The no-chase gate (enter only if 3 are true)

- □ At least one chain link confirms (cost, freight/insurance, FX, or demand evidence).

- □ Your time horizon matches the evidence (spot data for short-term; margin data for longer-term).

- □ You can explain the company/industry’s pass-through power in one sentence.

- □ You know the key “risk to the story” (demand drop, contract lag, FX shock).

- □ Your position size assumes you might be early (because themes overshoot).

Turn war headlines into your own numbers (so narratives don’t run your plan)

Theme investing is noisy; your results are measured over years. A simple discipline is to translate any theme idea into a long-horizon performance question:

- “If I’m wrong for a year, does this still fit my plan?”

- “What annualized return would justify the risk I’m taking?”

That’s why CAGR is useful: it compresses multi-year performance into one comparable number, which helps you stop treating headlines like destiny.

Related calculator: Open CAGR calculator

If you want the full macro context, read these next (near-end chain builders)

Official sources to sanity-check the chain (optional, for verification)

- IEA / EIA: energy supply, inventory, and market summaries

- BIS / central banks: funding stress context and cross-border liquidity notes

- IMF / OECD: macro demand and trade cycle context

(These are references for verification, not “trade signals.”)

FAQs (search-style)

Are war themes basically just defense stocks?

No. A defense headline is a narrative; profit depends on contract timing, delivery schedules, cost clauses, and FX exposure. Defense can benefit in some setups, but margins can lag or compress if inputs and delivery friction rise. Treat the theme as a chain, not a label.

Why do shipping and freight names move so fast on geopolitical headlines?

Freight and rerouting risk is a fast-moving link in the chain, so prices can reprice quickly. But net benefit depends on fuel costs, volumes, and demand durability. Fast price action is not the same as durable margin improvement.

How do I know if a theme rally is overheat or real transmission?

Use the overheat vs transmission table: overheat is broad “war-related” buying without chain confirmation. Transmission shows at least one or two confirming links (cost, freight/insurance, FX, demand) aligning with a plausible margin story. If confirmation is absent, default to patience.

Where does FX (like USD/KRW) fit in the war-theme chain?

FX can multiply both costs and revenues when invoices and hedges are USD-linked. In Korea-linked investing, KRW weakness can raise USD-denominated input costs (energy, components, freight) even when revenues look supportive. Always map USD revenues vs USD costs and hedges.

Can higher commodity prices be “good” for commodity-related equities but still bad for the economy?

Yes. Higher input prices can lift commodity producers while simultaneously tightening conditions for consumers and downstream manufacturers. That can eventually weaken demand and pressure broader risk sentiment. Separate sector earnings from macro demand effects.

What is the single most important question to ask before buying a war theme?

“Who pays the bill?” If customers can absorb pass-through, margins can hold. If demand breaks or contracts block pass-through, shareholders often pay through lower margins or lower volumes. This question forces you into mechanism, not narrative.

Should long-term investors do anything when war headlines hit?

Long-term investors benefit most from avoiding impulsive resets. Use a checklist to prevent chasing, define flip triggers, and keep position sizing consistent with uncertainty. If you act, prefer rule-based additions (like scheduled investing) over headline-timed bets.

Why include TNX and DXY when the topic is “war themes”?

Because the price chain doesn’t live inside one sector: USD strength (DXY) and the global discount rate (TNX) can tighten conditions and change the market’s tolerance for risk. They don’t predict the headline outcome, but they help you interpret the regime you’re in.