- Seoul vs Gyeonggi vs Incheon becomes easier when you treat it as a risk budget problem, not a taste problem.

- “Safe” is not the same as “less volatile”: safety depends on liquidity, drawdown behavior, and recovery speed under stress.

- In real estate, prices often lag; volume, time-on-market, and rebound patterns tend to move first.

- A region can look stable in price but be fragile in exits if liquidity dries up.

- Your framework should separate volatility (how far it swings) from liquidity (can you act?) and resilience (how it heals).

- Use observable triggers—volume shift, mortgage-rate jumps, and financial conditions—to classify regimes instead of guessing “the top.”

- The same headline can mean different things: in stress, cash and funding dominate; in calm, income and affordability dominate.

- A rules-based plan is not “predicting prices”—it’s defining support vs break conditions you can actually monitor.

- If your plan can’t survive a stress scenario (rate +1%p, volume -30%, sentiment risk-off), it’s not a plan yet.

INVESTING · KOREA REAL ESTATE

“Seoul feels safer,” “Gyeonggi is cheaper,” “Incheon is a wildcard”—most region debates are preference disguised as analysis.

That’s risky because preference doesn’t tell you what breaks first when liquidity disappears or financing tightens.

This post turns region choice into a risk-budget framework: volatility, liquidity, and recovery resilience—then links each axis to observable triggers you can watch on the apartment dashboard.

- A 3-axis map to classify Seoul/Gyeonggi/Incheon by role (defense vs carry vs rebound)

- A dashboard-first checklist that prioritizes volume, recovery signals, and downside defense

- Scenario rules (Base/Stress/Relief) with triggers and cross-asset reactions—so you don’t trade headlines

Scope/limits: no short-term price prediction, no “buy/sell now.” The goal is a repeatable interpretation system: signals → regime → rules.

Most people compare regions as if they’re shopping for a vibe. Investors (and investment-minded real buyers) should compare regions as if they’re allocating risk: where do I expect volatility, where can I exit, and how does recovery behave after drawdowns?

To apply this with real data, you’ll keep one tab open: the Seoul–Gyeonggi–Incheon apartment dashboard at South Korea Apartment Transaction Dashboard. We’ll use it as the “observable layer” that keeps our framework honest.

Turn “region choice” into a risk budget with three axes

Think of Seoul, Gyeonggi, and Incheon as three different portfolios—not three different lifestyles. The goal is to decide which region plays which role in your personal risk budget:

- Volatility: how wide the price swings can be (especially in down markets).

- Liquidity: how quickly and reliably transactions happen (your ability to act).

- Recovery resilience: after a shock, does the market rebound quickly, slowly, or unevenly?

This isn’t theory. It’s a way to answer practical questions like:

- If rates rise suddenly, where does demand freeze first?

- If risk-off hits, where do buyers disappear first?

- If the market stabilizes, where does “recovery” show up first—volume or price?

Table 1) The three-axis framework (definition → observable proxy → why it matters)

| Axis | What it means | Observable proxy you can track | Why it changes decisions |

|---|---|---|---|

| Volatility | Size of swings (up and down) | Peak-to-trough range, spread between price bands, sudden step-downs in medians | Determines your drawdown tolerance and stress survivability |

| Liquidity | Ability to transact without large concessions | Transaction volume trend, time-to-sell signals, “stalled” months | If liquidity breaks, you can’t execute your plan even if you’re “right” |

| Recovery resilience | How the market heals after a shock | Recovery shape (V vs U), speed of volume rebound, stabilization of lower price band | Resilience determines whether “waiting it out” is realistic |

Interpretation:

- Don’t confuse volatility with risk by itself—illiquid markets can be riskier even if prices look “stable.”

- Liquidity is a hidden constraint: many real-life decisions (upgrade, relocation, refinance) are liquidity events.

- Recovery resilience is your stress-test for narratives: strong stories without recovery signals are often just stories.

Mid-read connection: If you want a portfolio-level version of “risk budget” thinking (beyond real estate), use this framework as a template: Build a modern risk budget across stocks, bonds, cash, and gold.

What to read on the dashboard before you read prices

When headlines hit, people stare at price charts. But real estate tends to move through liquidity first. Use the dashboard to keep your attention on what changes early.

Here’s a mini-checklist you can run in under 2 minutes on /en/market/real-estate:

- Distribution: Where is the median, and how wide is the band (top vs bottom)?

- Wide bands often mean segmentation: “some units sell, others don’t.”

- Trend: How does the last 6–12 months look—flat, grinding down, or stabilizing?

- The shape matters more than the slope; stabilization patterns are signal-rich.

- Volume & recovery signals: Is volume returning? Is it broad-based or concentrated?

- Sharp rebound often looks like a sudden volume jump; bottoming looks like volume stops deteriorating and becomes consistent.

One-line takeaway: In real estate, “support” often shows up as volume stabilization before it shows up as price strength.

Region roles: strengths, weaknesses, and the single metric to watch

This section converts “feelings” into monitoring rules. You’re not trying to crown a winner. You’re deciding which region fits which role in your risk budget.

Table 2) Region → strength → weakness → dashboard metric to watch

| Region | Strength (role in a risk budget) | Weakness (what breaks first) | Dashboard metric to watch most |

|---|---|---|---|

| Seoul | Often behaves as a “quality/defense” anchor in many regimes; tends to retain buyer interest in stress | Entry cost is higher; affordability shocks can freeze marginal demand quickly | Volume stabilization in your target band (does trading continue even in stress?) |

| Gyeonggi | Broad market with mixed sub-cycles; can offer better carry and flexibility for budget-constrained buyers | Can fragment: some areas rebound fast while others stagnate | Recovery breadth: is volume improving across multiple areas or only a few hotspots? |

| Incheon | Can show sharper rebounds in relief regimes; sensitive to improvement in sentiment and financing | Can be more sentiment-driven; risk-off can drain bids quickly | Downside defense: does the lower band keep sliding, or does it stabilize? |

Interpretation:

- This is not about superiority—it’s about matching roles: defense vs flexibility vs rebound sensitivity.

- “Watch one metric” is a discipline trick: it prevents you from drowning in data and chasing the loudest chart.

- Use the dashboard at South Korea Apartment Transaction Dashboard to define your baseline (your band, your region scope), then track the one metric weekly/monthly.

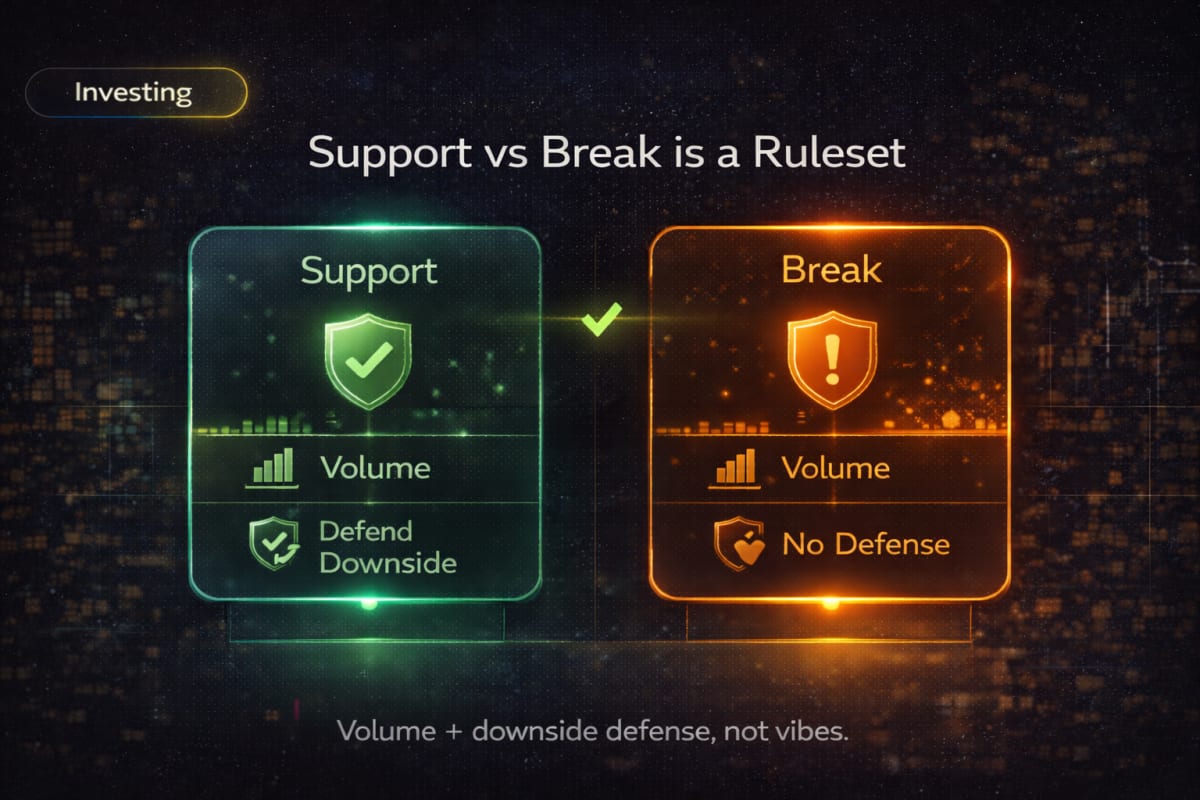

Build a “support vs break” framework using observable triggers

A risk budget needs a simple operating rule: when do you treat the market as supported, and when do you treat it as breaking?

We’ll define “support vs break” using three triggers you can actually observe:

- Mortgage rate impulse: abrupt jumps matter more than the level (buyers respond to change).

- Transaction volume: consistent volume is “oxygen”; volume collapse is “stress.”

- Financial conditions/spreads: when funding stress rises, risk-off spills into FX and sentiment (often hitting liquidity first).

You don’t need perfect data. You need consistent rules:

- If volume is stable and the lower band stops slipping, call it “supported.”

- If volume drops sharply and the lower band accelerates down, call it “breaking.”

Mid-read connection: If you want to understand why global rates can dominate local sentiment (and why regimes flip), keep this reference handy: TNX explained: the global discount rate you feel everywhere.

Table 3) 3 scenarios (Base / Stress / Relief) with triggers and cross-asset reactions

| Scenario | Observable triggers (watch, don’t predict) | Real estate behavior (Seoul/Gyeonggi/Incheon) | Stocks / Bonds / Cash (cross-asset context) |

|---|---|---|---|

| Base (grind) | Mortgage rates stable-ish; volume flat-to-slightly up; no sharp funding stress | Prices range-bound; volume decides “support”; Seoul holds better, Gyeonggi mixed, Incheon selective | Stocks mixed; bonds stable; cash optionality remains valuable |

| Stress (liquidity-first) | Mortgage rate jumps; volume drops; funding stress rises; risk-off tone | Liquidity dries up; lower band slips; weakest segments gap down first; Seoul resists longer but can freeze at the margin | Stocks down (risk-off); bonds may rally or wobble depending on inflation; cash becomes “comfort + optionality” |

| Relief (financing + sentiment) | Rates ease or stop tightening; volume rebounds; spreads/conditions improve | Volume leads; rebound may show up faster in sentiment-sensitive areas; Seoul regains depth, Gyeonggi broadens, Incheon can snap back | Stocks up (risk-on); bonds stabilize; cash becomes redeployable |

Interpretation:

- The point is not “what will happen,” but “what the world looks like when X is true.”

- Real estate regimes are often identified by liquidity conditions first—volume and band stabilization matter more than weekly price noise.

- Cross-asset context matters because risk-off often tightens financing and sentiment simultaneously.

Misconception box: “Seoul is always safer, so it’s always the right answer”

Misconception: “Seoul is always the safest choice, so if you can stretch, you should.”

Why it’s often wrong: “Safety” depends on your financing resilience and your ability to hold through stress. If you stretch too far, your personal liquidity breaks before the market does. In that case, “safe region” becomes irrelevant because your plan is forced to exit.

Check it properly:

- If your plan requires perfect rates and perfect income stability, it’s not safety—it’s fragility.

- If you can’t tolerate a volume freeze (time-to-sell risk), you must prioritize liquidity signals over “brand safety.”

One-line takeaway: A region isn’t “safe” if your personal balance sheet can’t survive the stress scenario.

Case study 1: Same budget, different risk budgets (defense vs flexibility)

Imagine two households with similar income, but different risk budgets:

- Household A prioritizes defense: stable cash flow, low tolerance for drawdowns, needs high confidence in liquidity.

- Household B prioritizes flexibility: can tolerate volatility, expects life changes, values option to adjust.

How the framework changes behavior:

- A uses the dashboard to pick a narrower band with strong volume stability (even if entry price is higher).

- B uses the dashboard to find a broader set of candidates where recovery breadth is improving (even if volatility is higher).

Practical rule:

- If you’re Household A, your “support condition” must be strict: volume must stay consistent and downside band must stabilize.

- If you’re Household B, your “break condition” should focus on accelerated downside defense failures (lower band sliding + volume evaporating).

Case study 2: Upgrade path—Seoul vs Gyeonggi vs Incheon as role switching

Upgraders often make a hidden mistake: they treat “upgrade” as a status move, not a role switch in a portfolio.

A better way:

- Define your current holding as “asset A” and target as “asset B.”

- Ask: Are you swapping into higher defense or higher rebound sensitivity?

A rules-based upgrade decision might look like this:

- If you need exit certainty (school, job relocation), prioritize liquidity signals even if you compromise on price upside.

- If you can hold through a multi-quarter slow patch, you can accept more volatility and focus on recovery breadth signals.

To make it real, open /en/market/real-estate and write down:

- Your current region’s volume trend (3–6 months)

- Your target region’s downside defense pattern (does the lower band stabilize?)

- Your “fail condition” (what would force a sale or prevent refinancing)

The dashboard-first checklist that keeps you honest

Use this when you feel pulled by narratives.

- □ I can describe my risk budget in one sentence (drawdown, liquidity needs, timeline).

- □ I track one primary metric per region (volume stability / recovery breadth / downside defense).

- □ I have a support condition (what must be true to stay patient).

- □ I have a break condition (what must be true to stop stretching risk).

- □ I can survive a stress scenario without forced selling (income + financing + liquidity).

- □ I won’t “upgrade” unless asset roles improve (not just aesthetics).

A monthly operating routine (so you don’t trade headlines)

A framework is only useful if it becomes a routine. Here is a simple cadence:

- Month-start baseline: Open South Korea Apartment Transaction Dashboard and record (a) your band’s distribution, (b) 6–12 month trend shape, (c) volume direction.

- Mid-month check: Did volume stabilize or deteriorate? Did the lower band accelerate down?

- Decision rule: If “break” triggers appear, reduce exposure to liquidity risk (pause upgrades, widen candidate set, increase cash optionality).

- Execution discipline: Only act when your pre-written triggers fire; otherwise, you’re reacting.

Continue reading to complete the risk map

If you want to extend this framework beyond “regions” into a full Korea market map, these next pieces fit together well:

- Understand how DXY shifts can tighten conditions and ripple into risk assets

- See how USD/KRW connects to earnings, inflation, and foreign flows into KOSPI

- Use a sector checklist for “weak KRW” regimes (who wins, who loses, and why)

One-line takeaway: Your edge is not prediction—it’s a cleaner rule set than the crowd.

FAQ: Seoul vs Gyeonggi vs Incheon as a risk-budget decision

1) Is Seoul always less risky than Gyeonggi or Incheon?

Not always. Seoul can be more resilient in many stress regimes, but if the entry cost forces you into fragile financing, your personal risk rises. “Less risky” must be defined as a combination of drawdown tolerance, liquidity needs, and time horizon.

2) What’s the most important dashboard metric for a real buyer with a tight timeline?

Liquidity signals usually matter most: volume stability and signs the lower band has stopped sliding. If you may need to act within a year, “can I transact?” often dominates “will it recover eventually?”

3) How do I define “support” without predicting prices?

Define it with observable conditions: volume stops declining, downside band stabilizes, and the trend shape stops deteriorating. Support is a behavior pattern, not a price target.

4) What does “recovery resilience” look like in the data?

It often looks like a steady improvement in transactions across a broader set of areas and price bands. A narrow rebound (only one hotspot) is weaker than broad-based stabilization.

5) How should I use this framework if I’m both a buyer and an investor?

Separate objectives: the home is a liability hedged by stability (life needs), while the portfolio is where you express macro views. Use the risk-budget lens to reduce forced-selling risk and keep optionality elsewhere.

6) Can Incheon be “safer” in any regime?

It can be safer if your plan aligns with its risk profile: you can hold through volatility, you prioritize entry affordability, and you monitor downside defense carefully. “Safer” is always relative to the plan.

7) How often should I check the dashboard?

Monthly for baseline and rules, plus a mid-month check if headlines are intense. If you check daily, you’ll overreact to noise and lose the benefit of the framework.

8) What’s the biggest mistake people make when comparing regions?

They compare “prices” without comparing “liquidity under stress.” A region that looks cheap can still be expensive if it traps you in a low-liquidity exit when conditions tighten.