- Retirement spending is not one number; it’s a system that must survive “bad months,” not average months.

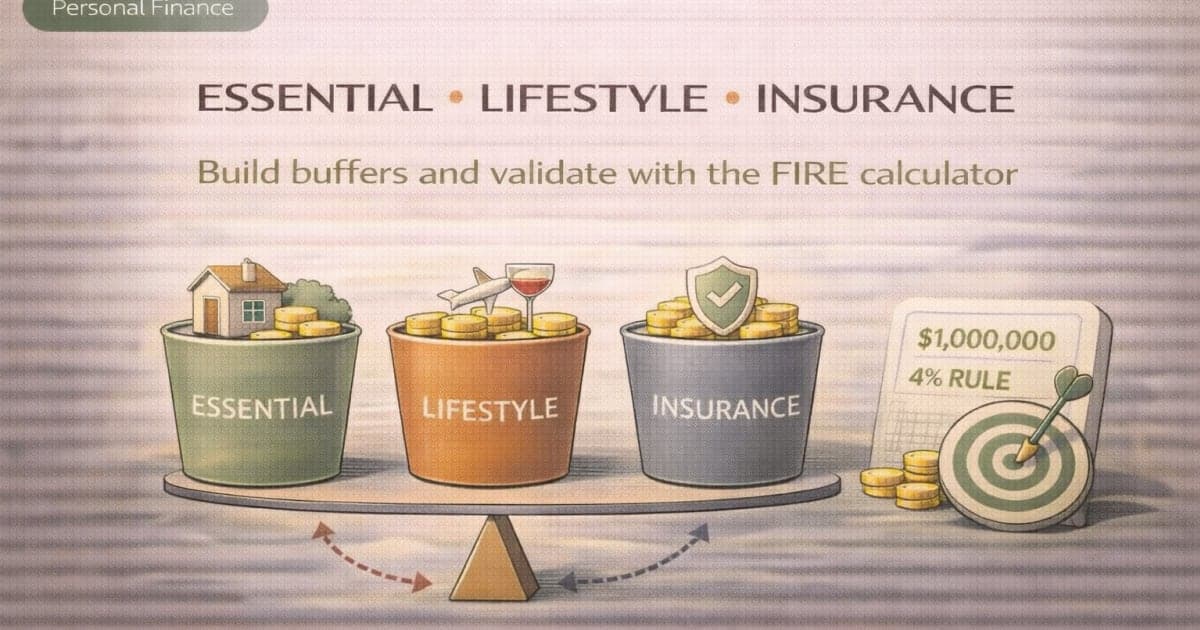

- The simplest stable model is to split spending into Essential / Lifestyle / Insurance (risk costs).

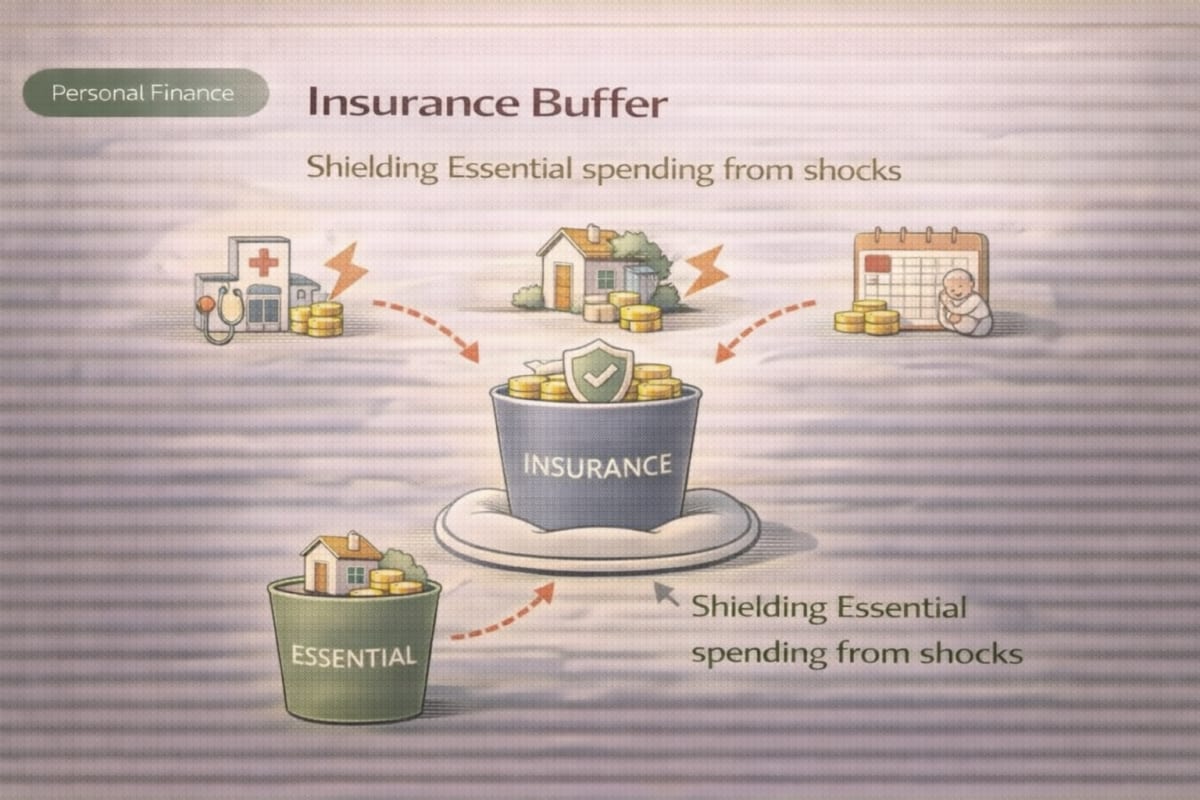

- The “Insurance bucket” is not just premiums—it’s predictable surprises: healthcare gaps, home repairs, taxes, and other high-impact shocks.

- If you don’t pre-fund risk costs, they will invade Essential spending (and that’s where plans break).

- Inflation should be modeled as spending-weighted, not a single CPI headline—especially for housing and healthcare-heavy budgets.

- A good FIRE plan is measured by coverage ratios and buffers, not by a single “net worth target.”

- Guardrails matter: a plan that adjusts spending rules-based is safer than one that assumes constant withdrawals forever.

- Healthcare is a major U.S. retirement variable: the pre-Medicare gap and out-of-pocket volatility belong in the Insurance bucket.

- Housing is more than a mortgage/rent line—property taxes, insurance, maintenance, and repairs are essential + risk costs.

- Use the FIRE calculator to validate: if your buffers are thin, the numbers will reveal it in minutes at FIRE calculator.

PERSONAL FINANCE · FIRE · RETIREMENT SPENDING

Most retirement budgets fail in the same way: they’re built on an “average year” and then get hit by a “stacked year” (medical bills + home repairs + higher insurance + inflation) and suddenly your plan feels fragile.

This post gives you an operating system: split spending into three buckets, attach control levers and failure signals, and then validate your buffers with the FIRE calculator—without relying on market predictions or product picks.

- Essential: the non-negotiables that keep life stable

- Lifestyle: the flexible “quality of life” layer

- Insurance (risk costs): predictable surprises you must pre-fund

Scope note: This is educational and framework-based. It is not tax/legal/medical advice, and it does not recommend specific stocks or funds.

Why “one spending number” is the wrong unit for retirement planning

When people say “I need $X per year in retirement,” they usually mean: “That’s my average lifestyle.”

But retirement risk doesn’t show up as an average. It shows up as clustered costs:

- A roof leak plus an HVAC replacement

- A year with higher health utilization (tests, prescriptions, out-of-pocket maximums)

- Insurance premium increases + property tax reassessments

- A travel-heavy year + family support costs

If your budget is a single blended number, every shock forces a choice between:

- cutting essentials (dangerous), or

- pretending it’s temporary (and hoping it doesn’t repeat), or

- increasing withdrawals (which can compound risk).

The three-bucket approach solves this by giving each type of spending a different rule-set:

- Essential must be protected

- Lifestyle should be adjustable

- Insurance (risk costs) must be pre-funded and replenished

That’s the difference between a plan and a hope.

Define the three buckets (with U.S.-specific examples)

The goal is not perfect categorization. The goal is operational clarity: when something changes, you know what to adjust.

1) Essential bucket (core stability)

Definition: Spending you must keep to maintain a stable baseline life.

Common U.S. examples:

- Housing: rent or mortgage (or HOA/condo fees), basic utilities

- Insurance basics: homeowners/renters, auto (minimum needed), baseline health coverage

- Food (baseline), transportation (baseline), phone/internet (baseline)

- Taxes (conceptually): property tax / required local taxes that are not optional

- Debt minimums (if any remain), required obligations

Rule: Essential is protected first. If Essential is drifting upward, you fix structure—not by “trying harder.”

2) Lifestyle bucket (quality-of-life layer)

Definition: Spending that improves life but is adjustable without breaking stability.

Examples:

- Travel, dining out, hobbies, gifts, experiences

- Upgrades (cars, gadgets), subscriptions above baseline

- “Nice-to-have” services and conveniences

Rule: Lifestyle is your shock absorber. It gets a cap and clear cut rules.

3) Insurance bucket (risk costs)

Definition: Costs that are not monthly essentials but arrive with predictable probability and meaningful size.

This is the most misunderstood bucket. It includes:

- Healthcare volatility: out-of-pocket maximum years, dental/vision needs, prescriptions

- Pre-Medicare gap costs (if retiring before eligibility): higher premiums + higher uncertainty

- Home maintenance and repairs: roof, HVAC, plumbing, appliances

- Insurance changes: homeowners premium spikes, policy gaps, deductibles

- Tax “surprises”: reassessments, escrow shortages, one-time fees

- Family support events and other irregular obligations

Rule: Risk costs should be pre-funded (a buffer) and replenished after use, like a reserve.

The operating system: control levers + failure signals

Buckets become powerful when you attach two things:

- Control levers (what you can change quickly), and

- Failure signals (how you detect drift early).

Bucket → control lever → failure signal (required table)

| Bucket | What belongs here (examples) | Control levers (rules you can actually pull) | Failure signals (early warnings) | Review cadence |

|---|---|---|---|---|

| Essential | Housing + utilities, baseline groceries, baseline insurance, baseline transportation, required taxes/obligations | Fix “big 3” first (housing/insurance/taxes); renegotiate or restructure recurring bills; remove hidden subscription creep from Essential | Essential rising 3 months in a row; housing+tax+insurance share drifting up; using credit to cover baseline | Quarterly |

| Lifestyle | Travel, dining, hobbies, extras, upgrades, premium subscriptions | Set a monthly/quarterly cap; “spend from remaining” (not from checking); pre-commit cut list (what stops first) | Lifestyle exceeds cap repeatedly; lifestyle spending starts pulling from Essential cash | Monthly |

| Insurance (risk costs) | Healthcare volatility, home repairs, deductibles, premium spikes, irregular tax/fee events | Separate reserve account; replenish rule after each event; categorize “known risks” and fund them proactively | Each shock forces higher withdrawals; reserve not replenished; you raid Essential for surprises | Semiannual / Annual |

Interpretation (2–3 lines):

- Essential is not “what you feel you should spend”—it’s what must remain stable when life gets messy. If Essential is drifting, you fix structure.

- Lifestyle is your planned flexibility. Without a cap and cut rules, it becomes silent Essential creep.

- The Insurance bucket prevents repeated shocks from turning into a permanent withdrawal increase.

Misconception box: “If my average spending works, I’m fine”

Why it fails: retirement risk is lumpy. A single “average” hides stacked costs (health + housing + insurance + taxes) that arrive together.

A better test: your plan should survive a year where (1) healthcare spending spikes, (2) a major home repair occurs, and (3) inflation feels higher than average—without breaking Essential spending.

The Insurance bucket is where U.S. retirement reality lives (especially healthcare)

In the U.S., healthcare is a key retirement variable because it is:

- hard to predict precisely,

- often volatile year to year,

- and can be structurally different before and after Medicare eligibility.

You don’t need perfect forecasting to plan well. You need:

- a clear “healthcare volatility” line item inside the Insurance bucket, and

- a replenishment rule.

Think of it like this:

- Some years you spend “normal.”

- Some years you hit higher utilization (tests, procedures, prescriptions).

- Occasionally you hit a near-worst-case year (high out-of-pocket).

The job of your Insurance bucket is to make those years survivable without turning them into permanent lifestyle downgrades or permanent withdrawal increases.

A practical way to size the Insurance bucket (conceptual)

Instead of a single number, define two layers:

- Routine risk costs: the common irregulars (minor repairs, dental/vision, deductibles)

- Shock layer: the “big year” buffer (major repair or high healthcare year)

If your Insurance bucket only covers routine risk costs, you’ll still panic on shock years.

If it covers shock years but isn’t replenished, you’ll panic later.

Inflation: model it as “spending-weighted,” then add buffers

Inflation adjustment is not optional in long retirements. But a single inflation rate can mislead because your retirement spending isn’t evenly distributed.

If housing + insurance + healthcare are a large share of your budget, your “felt inflation” can differ from headline CPI.

Inflation lens table (spending-weighted)

| Inflation lens | What it represents | Where it matters most | How to use it in planning |

|---|---|---|---|

| Headline inflation (single rate) | A broad average | Quick back-of-napkin projections | Use for initial sizing, but don’t stop here |

| Spending-weighted inflation | Your personal mix (housing/insurance/healthcare heavier) | Essentials and Insurance bucket | Apply more conservative assumptions to Essential + Insurance |

| Shock inflation (event years) | A year where multiple costs spike | “Stacked year” stress tests | This is what buffers are for—plan to survive it |

Interpretation (2–3 lines):

- A constant inflation rate is fine for starting, but you need a second lens: what happens when the categories you rely on most rise faster.

- Buffers should be thicker where your spending is least flexible: Essential + Insurance.

- Lifestyle can flex; Essential should not.

Mid-point stress test: validate your buffers with the FIRE calculator

At this point, you have enough to run a useful test. Don’t try to “optimize.” Just validate stability.

Go to FIRE calculator and start with these inputs:

Set Annual Spending as (Essential + Lifestyle + Insurance) and set Inflation to your planning assumption; then test different horizons and return assumptions to see how sensitive your plan is.

What to look for in the results

- If small changes in inflation or returns break the plan, your structure is under-buffered.

- If the plan survives but only by cutting Essentials, your bucket design is wrong.

- If the plan survives by trimming Lifestyle first, that’s what you want: controlled flexibility.

Guardrails: how to adjust spending without turning every dip into panic

A stable plan needs “if-then rules,” not constant willpower.

Guardrails make your spending adjustments predictable and bounded.

Here’s a conceptual guardrail model using buckets:

- Essential: protected (don’t cut unless structural)

- Lifestyle: adjustable (the primary lever)

- Insurance: maintained (replenish after use)

Example guardrails table (conceptual)

| Trigger condition | What it means | Rule-based response (bucket-level) | What you avoid |

|---|---|---|---|

| Portfolio / plan margin deteriorates | Your plan is trending tighter | Freeze Lifestyle upgrades; apply a temporary Lifestyle cap reduction | Panic selling; cutting Essentials |

| Insurance bucket is drawn down | A shock occurred | Replenish reserve over the next X months before expanding Lifestyle again | “Pretending it’s a one-off” and repeating the shock |

| Essential drift (housing/taxes/insurance up) | Structural baseline is rising | Address structure: shop insurance, review housing costs, remove recurring creep | Repeatedly trimming Lifestyle forever |

| Inflation feels higher than assumed | Your spending-weighted inflation is higher | Increase buffer contributions; adjust future Lifestyle expectations | Underestimating long-run drag |

Interpretation (2–3 lines):

- Guardrails are not about predicting markets; they’re about controlling what you can control.

- The “correct” adjustment is usually a Lifestyle cap change, not an Essential cut.

- Replenishment rules stop one shock from turning into a permanent plan downgrade.

Case study A: Retiring at 55 (pre-Medicare gap) — why the Insurance bucket must be thicker

Profile (illustrative):

- Retiring before Medicare eligibility

- Housing is stable, but healthcare costs are uncertain

- Lifestyle goals are meaningful (travel, hobbies), but not worth risking Essential stability

Bucket implications:

- Essential: housing + utilities + baseline living remain steady

- Lifestyle: can flex and be capped

- Insurance bucket: must explicitly include the healthcare gap risk layer

Rules that keep the plan stable:

- Treat healthcare volatility as a risk cost, not a lifestyle tradeoff.

- Cap Lifestyle spending until the Insurance bucket is adequately funded.

- If you hit a high-cost health year, replenish first—then re-expand Lifestyle.

This is why a single “annual spending number” is misleading: the same total can be safe or unsafe depending on how much is pre-funded for the healthcare gap.

Case study B: Homeowner retirement — property tax + insurance + maintenance as Essential + Insurance

Profile (illustrative):

- House is paid off (or nearly)

- Monthly housing payment looks low, but true housing cost is not

- A few large repairs can arrive close together (roof/HVAC/plumbing)

Bucket implications:

- Essential: property taxes + baseline homeowners insurance + utilities + baseline upkeep

- Insurance: repairs, deductible events, premium spikes, major maintenance cycles

Rules that keep the plan stable:

- Track housing as a system: taxes + insurance + maintenance, not “mortgage only.”

- Keep a dedicated home reserve inside the Insurance bucket.

- Don’t finance predictable repairs with Lifestyle cuts plus credit—pre-fund and replenish.

Checklists you can use today

Checklist 1: Build your bucket budget (30–60 minutes)

- Pull the last 3–6 months of spending and label each item Essential / Lifestyle / Insurance (risk costs)

- For Essential: identify your “big 3” drivers (housing, insurance, taxes/obligations)

- For Lifestyle: set a monthly or quarterly cap you can stick to

- For Insurance: list your top 5 risk costs (healthcare volatility, home repairs, deductibles, premium spikes, irregular taxes/fees)

- Create a separate reserve (or sub-account) and set an automatic contribution

- Write one replenishment rule: “After a shock, replenish before Lifestyle expands again”

Checklist 2: Annual review (60 minutes, once a year)

- Recalculate Essential drift (housing + insurance + taxes/obligations)

- Update Insurance risks (health changes, home age, premium trends, deductibles)

- Re-check spending-weighted inflation (is your mix changing?)

- Re-validate your plan with a stress test and adjust guardrails if needed

Final validation: run a simple stress test (and interpret it correctly)

Here’s the cleanest way to use the FIRE calculator without overthinking:

- Enter your bucketed annual spending (Essential + Lifestyle + Insurance).

- Stress test inflation and return assumptions.

- Observe which bucket would change first under pressure (it should be Lifestyle).

Open FIRE calculator and input:

Use Annual Spending (bucket total), Retirement Horizon (years), plus Return and Inflation assumptions; then compare a baseline run vs a “higher inflation / lower return” run to see whether your buffers are thick enough.

Related reads (internal)

Mid-post links (context + setup):

- The Three Pillars of Personal Finance: Budgeting, Emergency Funds, and Long-Term Investing

- Household Survival in an Inflation Era: Cut Fixed Costs, Control Spending, and Protect Cash Flow

Near the end (buffers + decision rules):

- Your Emergency Fund Isn’t a ‘Months’ Number — It’s a Risk Number (Job, Family, Debt)

- High-Rate Era: Should You Pay Down Debt or Invest First? (The Interest-Rate Threshold Rule)

- How to Reach Your Target Amount Faster: Balancing Principal, Return, and Time

FAQs

Q1. Is the “Insurance bucket” just insurance premiums?

No. In this framework, it’s risk costs: predictable surprises with meaningful impact—healthcare volatility, deductibles, home repairs, premium spikes, irregular taxes/fees, and other lumpy costs.

Q2. Where do healthcare costs go—Essential or Insurance?

Baseline coverage and routine predictable costs can be treated as Essential. Volatile, lumpy, and high-variance costs belong in the Insurance bucket—especially the pre-Medicare gap and out-of-pocket spike years.

Q3. Are property taxes Essential?

Conceptually, yes—because they’re required to maintain housing stability. The volatility (reassessments, escrow shortages) is better handled as an Insurance bucket component.

Q4. How do I adjust for inflation in withdrawals?

Use inflation-adjusted spending as a planning baseline, but pair it with guardrails: if your plan margin tightens, you adjust Lifestyle caps first rather than mechanically increasing withdrawals forever.

Q5. What’s the single biggest reason bucket plans work better?

They create controlled flexibility. Instead of cutting everything or increasing withdrawals blindly, you know which layer moves first (Lifestyle) and which layer is protected (Essential).

Q6. How big should the Insurance bucket be?

There’s no universal number. A practical approach is to define two layers: routine risk costs + a shock layer (for a “stacked year”). Then stress-test using the FIRE calculator to see if your plan survives without breaking Essentials.

Q7. What’s a clear failure signal that my plan is under-buffered?

When shocks repeatedly force you to (1) raid Essential cash, (2) increase withdrawals permanently, or (3) use credit for baseline stability. Those are signals the Insurance bucket is too thin or not replenished.

Q8. How often should I review bucket assignments?

Lifestyle caps are best reviewed monthly; Essential drift quarterly; Insurance bucket risks semiannually or annually. The point is to catch drift early—before it becomes permanent.