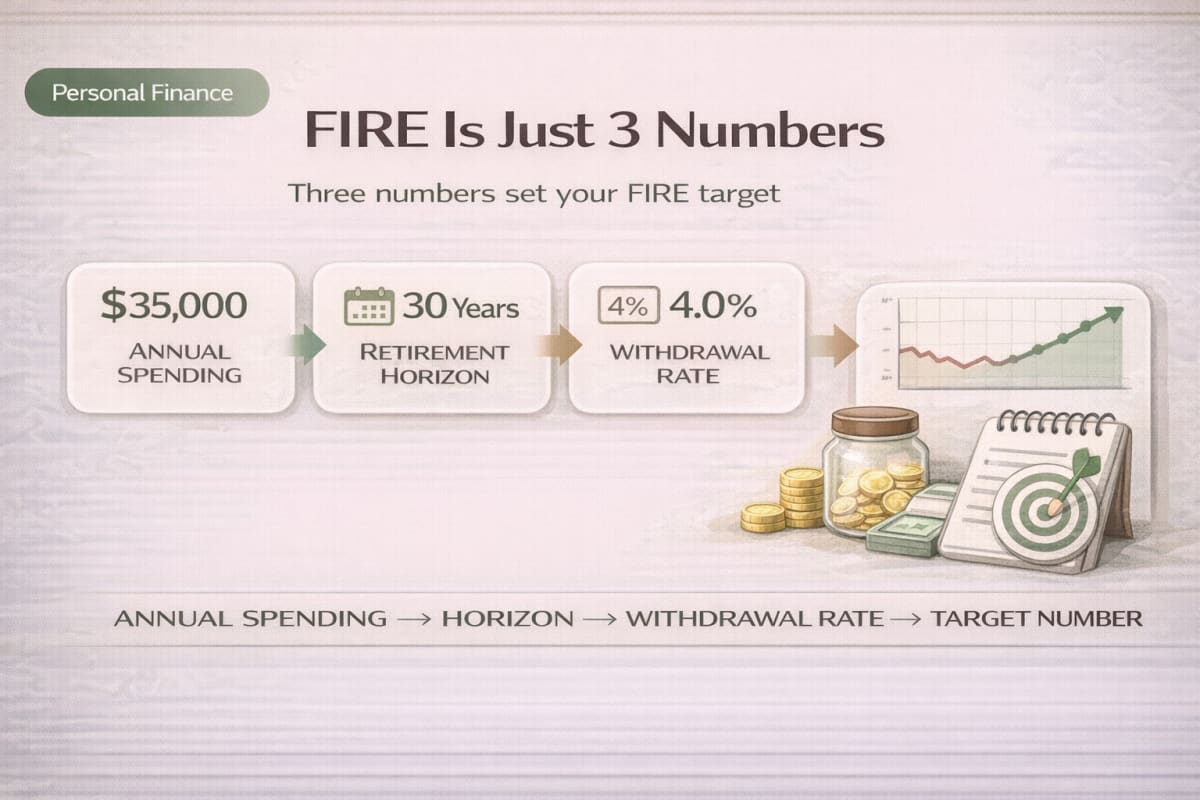

- FIRE is not “a magic net worth.” It’s three numbers: annual spending, retirement horizon, and a withdrawal rate that can survive real-world volatility.

- If your annual spending estimate is off, your FIRE number is off—usually by more than any “return assumption” ever could fix.

- Your horizon is not your lifespan; it’s the number of years you’ll rely on portfolio withdrawals before stable income sources (like Social Security) cover most of your spending.

- A withdrawal rate is not a promise of returns. It’s a probability statement that depends on inflation, portfolio behavior, and sequence-of-returns risk (bad early years can do lasting damage).

- The classic “4% rule” is best treated as a starting point, not a guarantee—especially for 40+ year horizons and higher inflation uncertainty.

- In the U.S., retirement cash flow is a system: 401(k)/IRA withdrawals + taxable accounts + Social Security + healthcare costs (pre-Medicare vs Medicare). Your plan should reflect that system.

- The safest FIRE plan is not “maximize returns.” It’s “build guardrails”: spending flexibility bands, cash buffers, and trigger-based adjustments you can execute calmly.

- You can validate your own number in minutes using the FinMap FIRE calculator at Fire Calculator, without making any stock/ETF predictions.

- The goal is not perfect precision. The goal is a plan that is stable under stress and still works when life and markets don’t cooperate.

PERSONAL FINANCE · FIRE

“How much do I need to retire?” sounds like one question, but it’s secretly three.

The dangerous part is not picking the wrong portfolio—it’s guessing your spending, ignoring horizon, and assuming the 4% rule is a guarantee (it isn’t). Conditions and exceptions matter.

This guide gives you a framework + rules: define your three numbers, model inflation-adjusted spending, account for Social Security/Medicare timing at a high level, and add sequence-risk guardrails you can actually follow.

- A practical way to write annual spending as a “retirement version” budget (not just today’s expenses × 12)

- How to set a realistic horizon and choose a withdrawal rate as a survival probability, not a prediction

- A step-by-step, rules-based validation workflow using Fire Calculator (no stock/ETF recommendations)

Scope/limits: This is educational and not tax/legal/medical advice. No security selection, no short-term market forecasts—just “interpretation → rules → execution.”

The whole FIRE plan in one sentence

Your FIRE target is not a vibe and not a meme. It’s one sentence:

“I want to fund $X per year (inflation-adjusted), for Y years, at a withdrawal rate I can survive—while managing sequence risk.”

Everything else is just implementation detail.

- Annual spending tells you the size of your lifestyle.

- Horizon tells you how long the lifestyle must be funded before (or while) other income sources cover more of it.

- Withdrawal rate tells you the speed limit—how aggressively you pull from assets each year.

Here’s the simplest math that’s still useful:

- Portfolio-funded spending (annual) = Annual spending − stable income

(stable income might include Social Security later, a pension for some, or predictable part-time income you’re confident about) - FIRE number (rough) = Portfolio-funded spending ÷ Withdrawal rate

This is not “the answer.” It’s the starting position—then you add stress tests and operating rules so you don’t blow up in the first bear market.

Here’s a one-line takeaway: your FIRE number is mostly a spending decision, not a return decision.

Number 1: Annual spending (the “retirement version,” not today’s)

Most FIRE plans break because spending is defined as “current expenses × 12.” That misses the spending you’ll have in retirement and overweights the expenses that might disappear.

In the U.S., your spending profile often changes across phases:

- Pre-Medicare healthcare (if you retire before 65): premiums + deductibles + out-of-pocket can become a major line item.

- Medicare phase (65+): healthcare cost structure changes again (still meaningful, but different).

- Housing: rent vs mortgage vs property tax/insurance/maintenance.

- Family + support: kids, parents, or other dependents can create “lumpy” costs.

- Taxes: taxable withdrawals and Roth strategies matter, but tax planning is personal—treat it as a range, not a single perfect number (not advice).

A practical rule: write spending as two layers.

- Spending floor (non-negotiable): housing, utilities, groceries, core transport, insurance, baseline healthcare, minimum debt obligations

- Spending flex (adjustable): travel, dining, subscriptions, upgrades, hobby intensity, gifting, big discretionary purchases

This is not just budgeting. It’s what makes your withdrawal rate survivable when sequence risk shows up.

Table 1) Annual spending worksheet (retirement-focused)

| Category (decision) | Examples (U.S. context) | Why it changes in retirement | Input tip (rules-based) |

|---|---|---|---|

| Housing | Rent / mortgage / property tax / insurance / HOA / maintenance | Mortgage may end; taxes/insurance/maintenance remain | Model the housing you’ll actually have in retirement, not today’s |

| Healthcare | Premiums, deductible/out-of-pocket, prescriptions | Pre-Medicare can be the expensive phase; Medicare changes the structure | Use a base + “shock” buffer line item |

| Living essentials | Groceries, utilities, phone/internet | Often stable; inflation matters | Use inflation-adjusted thinking: “today’s dollars” baseline |

| Transportation | Car payments, fuel, repairs, transit | Work commuting may drop; maintenance remains | Include a replacement cycle (lumpy costs averaged annually) |

| Family/support | Child support, college help, elder support | Phase-dependent; can spike | Separate “baseline” and “event budget” |

| Leisure & travel | Trips, hobbies, dining | Often rises early in retirement | Consider “go-go years vs slow-go years” spending |

| Debt obligations | Student loans, personal loans, HELOC | Can shrink or persist | Treat as non-negotiable until proven otherwise |

| Taxes (range) | Federal/state income, cap gains | Depends on withdrawal source | Use a conservative buffer if unsure (not advice) |

Interpretation (2–3 lines):

Your annual spending estimate is a decision, not a discovery. The point is not perfect precision; it’s to build a plan that stays true even when costs shift across phases (especially healthcare and housing). If you can separate spending into a floor and a flex band, you gain a powerful lever for sequence-risk survival.

Mid-post “connective tissue” (A good piece of writing to read together):

If your cash flow foundation is shaky, FIRE math won’t fix it—these help you build the base system first.

- Set the foundation first: budgeting + emergency fund + long-term investing (a checklist system)

- Size your emergency fund by risk (job/family/debt), not a generic “3–6 months” rule

Number 2: Retirement horizon (it’s a cash-flow horizon, not a lifespan)

“Horizon” sounds like “how long will I live?” That’s the wrong framing. In FIRE planning, horizon is:

How many years will you rely on portfolio withdrawals to cover a meaningful share of spending?

This matters because the same withdrawal rate can look “fine” over 25–30 years and feel much riskier over 40–50 years, especially if the first decade is rough.

A practical way to set horizon:

- Pick a withdrawal start age (when you stop relying on earned income).

- Pick a planning age (not a prediction—just a conservative planning endpoint).

- Horizon = planning age − start age.

- Then overlay income timing: when Social Security begins and how it changes portfolio pressure.

High-level U.S. context notes (not advice):

- Social Security can act as a “future floor,” reducing how much the portfolio must fund later.

- Medicare changes healthcare spending mechanics at 65, so early retirees often face a distinct healthcare phase before that.

One-line takeaway: horizon is what makes early retirement hard—even if your spending is modest.

Number 3: Withdrawal rate (and why the 4% rule gets misunderstood)

Withdrawal rate sounds like a return assumption. It’s not.

A withdrawal rate is a rule about how fast you take money out despite uncertainty:

- inflation,

- market volatility,

- and especially sequence-of-returns risk.

Sequence-of-returns risk is the brutal truth that “average returns” do not protect you if the first few years are bad. A large early drawdown + withdrawals can shrink your base so much that later “good” returns don’t fully repair it.

Misconception box: the 4% rule is not a guarantee

Misconception: “If I withdraw 4% a year, I’m safe forever and my principal won’t really shrink.”

Why it’s wrong: The 4% rule is commonly discussed as a historical rule-of-thumb under specific assumptions. Real life includes different horizons, inflation regimes, taxes, spending shocks, and—most importantly—sequence risk. Even if your long-run average return looks “fine,” bad early years can force painful cuts.

Instead, verify like this:

- □ Test your plan at multiple horizons (e.g., 30 vs 40 years)

- □ Add guardrails (spending flex band, cash buffer, trigger rules) rather than relying on one magic percentage

Here’s the key reframing: the withdrawal rate is only half the plan; the other half is how you react when reality deviates.

Table 2) Withdrawal-rate thinking by horizon (framework, not advice)

| Horizon (years) | What changes | Why 4% can feel different | Practical guardrail focus |

|---|---|---|---|

| 25–30 | Shorter “survival window” | Fewer years exposed to compounding inflation shocks | Rebalance discipline + moderate spending flexibility |

| 35–40 | More sequence exposure | Early bad decade has more time to compound damage | Stronger spending flex band + cash buffer + trigger rules |

| 45+ | “Forever” style risk | Inflation + healthcare shocks dominate outcomes | Conservative planning + multiple income floors + strict guardrails |

Interpretation (2–3 lines):

As horizon extends, the plan becomes less about “picking the perfect rate” and more about building a system that adapts. A long horizon amplifies the cost of early drawdowns and high inflation. The right move is not heroically chasing returns, but adding operational controls you can execute without panic.

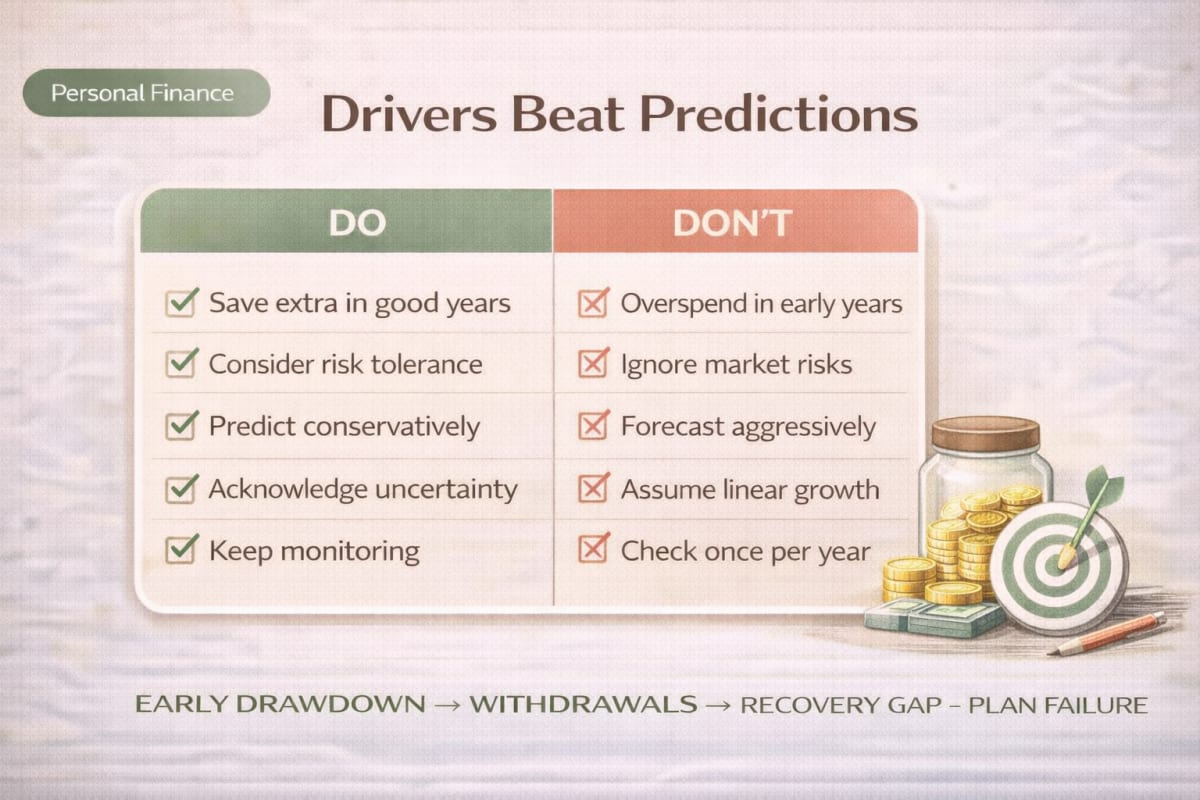

The operating system: inflation-adjusted spending + sequence-risk guardrails

If you want a plan that survives stress, add two mechanics:

Inflation-adjusted spending framing

Think in “today’s dollars” and treat inflation as a force that slowly increases the required withdrawal in nominal terms. Even if investments grow, purchasing power is the real goal.Guardrails for sequence risk

You do not need to predict the market. You need to decide in advance what you do when the portfolio is down.

A simple guardrail set you can personalize (no market prediction required):

- Spending floor stays funded. Flex spending is the shock absorber.

- Cash buffer (a small “runway”) reduces forced selling when markets are down.

- Trigger rules for temporary spending cuts or income bridges (part-time work, delayed big purchases, etc.).

- Annual review at one fixed time, not weekly tinkering.

Table 3) Scenario triggers and what to do (Base / Escalation / De-escalation)

| Scenario | What’s happening | Observable triggers (examples) | Rules-based response |

|---|---|---|---|

| Base | Normal volatility | Spending near plan; portfolio moves within typical ranges | Keep withdrawals steady; review once per year |

| Escalation | Sequence-risk zone | Early-retirement drawdown + withdrawals feel heavy; unexpected healthcare or family costs | Temporarily cut flex spending; use buffer first; pause non-essential “lumpy” spending; re-check withdrawal rate |

| De-escalation | Stabilizing | Spending normalizes; income floor grows (e.g., Social Security begins) | Restore flex spending gradually; rebuild buffer; keep rules intact |

Interpretation (2–3 lines):

This is the missing piece most FIRE discussions skip: an “if-then” playbook. You’re not trying to be right about markets—you’re trying to be consistent when the plan is tested. When you pre-commit to actions, your withdrawal rate becomes a managed system, not a fragile bet.

Validate your number in 10 minutes with the FIRE calculator (mid-CTA)

At this point, you have the only inputs that matter. Now validate them with the tool—not to “predict returns,” but to see how sensitive your plan is to each number.

In the calculator, start with annual spending in today’s dollars and your retirement horizon (how many years withdrawals must cover meaningful costs).

If the tool asks for return/inflation assumptions, keep them conservative and focus on sensitivity: change spending / horizon / withdrawal rate first, then interpret the output (tool: Fire Calculator).

Case studies: same income, different outcomes (because the three numbers differ)

These are simplified examples to show how the framework works. They are not prescriptions and ignore personal tax/legal specifics.

Case A: W-2 employee aiming for a “clean” FIRE number

- Age now: 38

- Retirement start: 50 (early retirement)

- Annual spending target (today’s dollars): $60,000

- Flex vs floor: $45k floor, $15k flex

- Accounts: 401(k) + IRA + taxable (details omitted)

- Income floor later: Social Security planned as a future baseline (timing varies; treat conservatively)

Interpretation:

The key risk isn’t “returns.” It’s the 15-year bridge before typical retirement ages, where sequence-of-returns risk is concentrated. The plan becomes dramatically more stable if the retiree can cut the $15k flex band during drawdowns and maintain a buffer for healthcare and shocks.

Rules that make it survivable:

- If portfolio is down materially in the first 5–7 years, reduce flex spending first.

- Delay “lumpy” purchases (cars, major renovations).

- Rebuild buffer during good years instead of upgrading lifestyle permanently.

Case B: Self-employed household with higher variability and healthcare uncertainty

- Age now: 42

- Retirement start: 55

- Annual spending target: $75,000

- Higher healthcare uncertainty before Medicare

- Retirement savings: SEP-IRA/solo 401(k) style mix (high-level), taxable savings for bridge

Interpretation:

The spending number is higher and the pre-Medicare phase creates a bigger “shock band.” This doesn’t mean FIRE is impossible—it means the plan must be more conservative in guardrails: bigger buffer, stronger flex band, and a clear rule for what happens in the first bear market.

Rules that make it survivable:

- Treat healthcare and family support as non-negotiable; treat travel/upgrades as the first lever.

- Increase buffer size or plan for a small, reliable income bridge.

- Avoid designing a plan that requires perfect market conditions in the first decade.

One-line takeaway: the same portfolio can feel “safe” or “fragile” depending on your spending floor and your horizon.

Checklist 1: Lock the three numbers without overthinking

- □ My annual spending is written as a retirement version budget (not just current spending × 12)

- □ I separated spending into floor (must pay) and flex (adjustable)

- □ I explicitly modeled a healthcare phase: pre-Medicare vs Medicare (high level)

- □ I set a clear horizon (years withdrawals must fund meaningful costs)

- □ I understand that withdrawal rate is a survival rule, not a return forecast

- □ I have at least one sequence-risk guardrail (buffer or trigger rules)

Checklist 2: Turn FIRE into an operating plan (the “rules” that keep you calm)

- □ I have a written rule for what I cut first when markets are down (flex spending list)

- □ I review the plan once per year at a fixed time (not during panic weeks)

- □ I have a “lumpy spending” rule (cars, renovations, big trips) that pauses during drawdowns

- □ I have a buffer restoration rule during good years (rebuild first, upgrade later)

- □ I treat Social Security as a future floor conservatively (no over-optimism)

- □ I can explain my plan in one sentence using the three numbers

The “10-minute loop”: how to iterate without falling into prediction mode

Use this loop whenever your FIRE number feels too high or too fragile:

Adjust spending structure, not just spending level

Reduce the floor by changing commitments; keep flex as the shock absorber.Adjust horizon assumptions realistically

If you plan to do partial work or have future income floors, reflect them conservatively.Adjust withdrawal rate by adding guardrails

Instead of chasing returns, strengthen flexibility, buffer, and trigger rules.Only then touch return/inflation assumptions

Treat them as sensitivity checks, not levers to “force” the plan to work.

The goal is a plan that “still works” under less-friendly conditions.

Near the end: validate one more time with the FIRE calculator (second CTA)

You’re ready to validate again—this time focusing on your guardrails and sensitivity, not a single-point estimate.

Enter (1) your annual spending (today’s dollars), (2) your horizon (years of reliance on withdrawals), and (3) your withdrawal approach (or conservative proxy).

Then run a quick sensitivity pass: change spending by ±10% and horizon by ±5–10 years to see what truly moves the result (tool: Fire Calculator).

Conclusion: FIRE becomes easy when you stop arguing with math

FIRE isn’t complicated. It’s uncomfortable—because it forces three decisions:

- How much you want to spend (and what is truly non-negotiable)

- How long your portfolio must carry you

- How aggressively you withdraw, knowing inflation and sequence risk exist

Once those numbers are written down, the plan becomes a rules-based system:

- inflation-adjusted spending framing,

- guardrails for bad early years,

- and an annual review rhythm you can stick to.

You don’t need perfect forecasts. You need a plan that survives imperfect reality.

Continue reading to make the plan easier to execute (A good piece of writing to read together)

- Debt vs investing without regret: a simple threshold rule you can actually follow

- Inflation-proof your cash flow: restructure fixed costs and protect spending power

- Compound interest fundamentals: why long-term plans fail when you misunderstand growth

- Reality-check “7% a year”: how return assumptions distort FIRE math

FAQ (common FIRE questions)

1) What’s the simplest FIRE formula?

A useful starting point is: FIRE number ≈ (annual spending − stable income) ÷ withdrawal rate. It’s a rough baseline. Then you add guardrails for inflation, healthcare, and sequence-of-returns risk.

2) Is the 4% rule safe for early retirement?

Treat it as a starting point, not a guarantee. Early retirement usually means a longer horizon and more sequence-risk exposure. The safer move is adding guardrails (flex spending + buffer + trigger rules) rather than relying on one percentage.

3) How do I include Social Security in FIRE planning?

At a high level, Social Security can be modeled as a future income floor that reduces how much your portfolio must fund later. Because timing and benefits vary, use conservative assumptions and avoid building a plan that requires best-case outcomes.

4) Why does sequence-of-returns risk matter so much?

Because withdrawals during a downturn can permanently shrink your base, making later recoveries less effective. Two plans with the same “average return” can have very different outcomes depending on the first 5–10 years.

5) Should I plan in nominal dollars or inflation-adjusted dollars?

Use inflation-adjusted (“today’s dollars”) for clarity, then recognize that actual withdrawals rise in nominal terms over time. Your goal is purchasing power, not a nominal number.

6) How do I estimate retirement healthcare costs (pre-Medicare vs Medicare)?

Model healthcare as a phase-based line item: one estimate before Medicare eligibility and another after. You don’t need precision—use a conservative base and include a shock buffer. This is not medical or legal advice.

7) What if my FIRE number feels too high?

Don’t force the plan by assuming higher returns. Start by lowering the spending floor, adding spending flexibility, adjusting horizon assumptions realistically, and strengthening guardrails. Then validate sensitivity with the calculator.

8) How often should I update my FIRE plan?

Once per year is usually enough for a rules-based plan, plus updates after major life changes (housing, family support, healthcare, income). Avoid constant tinkering during market noise.