- Global DCA feels uniquely stressful because your USD result is driven by two return streams: the asset’s return and the currency’s return.

- The same “+8% USD return” can mean two very different stories—strong asset performance with FX headwinds, or weak assets masked by a strong foreign currency.

- Currency isn’t something you need to forecast to succeed; it’s something you need to separate, label, and manage with rules.

- Most people don’t quit DCA because the long-term idea is wrong—they quit because short-term volatility triggers panic pauses and “just this month” exceptions.

- A simple decomposition habit (asset vs FX) reduces emotional overreaction because it shifts your attention from blame to diagnosis.

- The safest DCA plan is designed around what you can control: contribution consistency, cash-flow buffers, and rebalancing triggers—not predictions.

- Rebalancing works best when it’s allocation-based (drift rules), not opinion-based (“the dollar looks strong/weak”).

- Your plan is only as good as its assumptions; you should stress-test returns, inflation, fees, and contribution growth to see what actually breaks it.

- If you can explain your month using three lines—asset, FX, and your own contributions—your plan becomes harder to abandon.

- You can validate the entire framework in 10 minutes using the DCA calculator at ETF/Stock DCA Simulator.

PERSONAL FINANCE · DCA · FX DECOMPOSITION

“I’m doing global DCA, but the currency swings make it feel random. I keep wanting to pause until FX ‘calms down.’”

That instinct is expensive: the biggest damage usually comes from panic pauses and rule-drift—not from currency itself. FX adds volatility, but your behavior decides whether that volatility becomes a permanent scar.

This article gives you a practical decomposition framework (asset return + currency return) and a rules-based operating plan (contribution rules, guardrails, and rebalancing triggers) so your strategy survives real-world volatility without relying on forecasts.

- A one-minute method to explain your USD return without guessing what FX will do next

- A contribution rulebook that prevents “just this month” pauses and keeps DCA consistent

- A stress-test workflow using the DCA Calculator to find the assumptions that actually break your plan

Scope: no stock/ETF picks, no currency forecasting. This is about interpretation → rules → consistency.

Why global DCA feels harder than “normal DCA”

If you DCA into something priced in your home currency, you mostly live with one type of uncertainty: the asset’s price movement.

If you DCA into foreign exposure (international stocks, global bonds, non-USD cash flows, overseas real assets), your USD outcome is affected by two different engines:

- Asset return (what the underlying asset did in its local market)

- Currency return (what the USD did versus the local currency)

That second engine (FX) is what turns a normal bad month into a “my plan is broken” month.

But here’s the key point: FX volatility is not a reason to abandon DCA. It’s a reason to upgrade your interpretation and your rules.

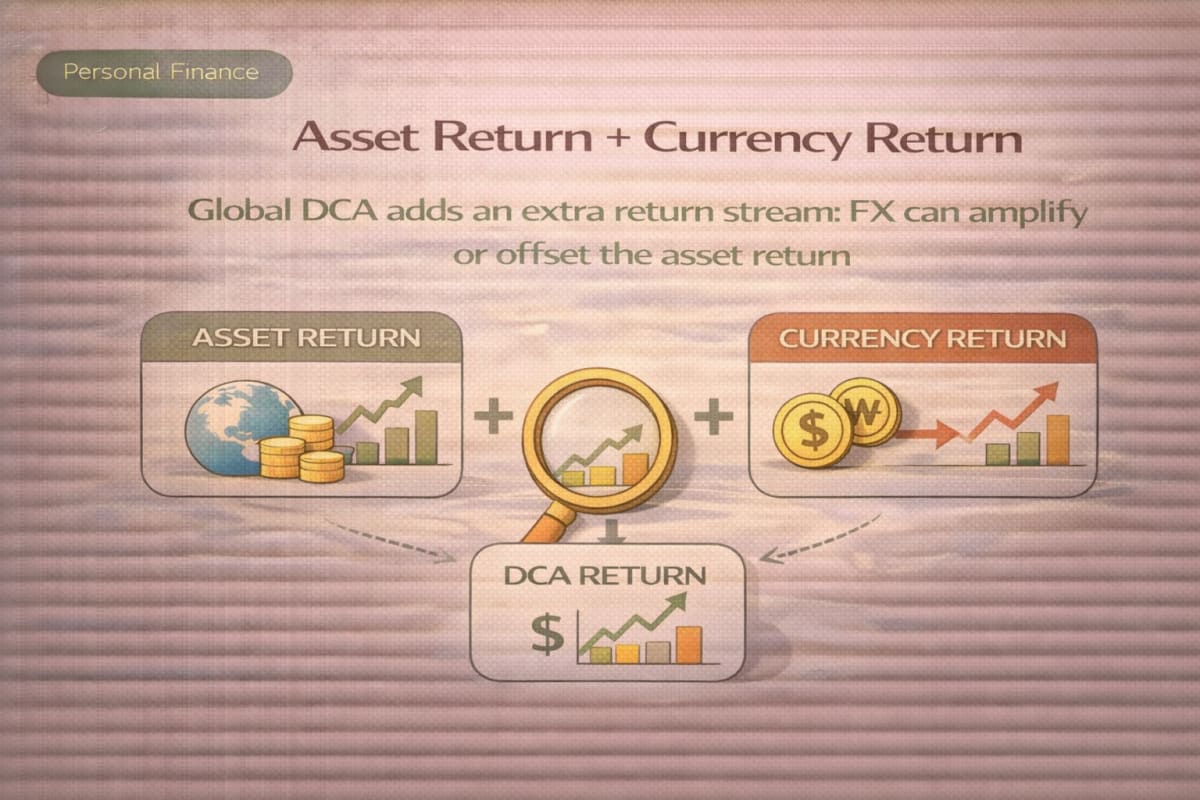

The two-stream return model you can use every month

A useful mental model for USD-based investors:

- USD return ≈ local asset return + FX return (plus a small interaction term)

More precisely (still intuitive):

- USD return = (1 + local return) × (1 + FX return) − 1

Where:

- Local return is the asset’s performance in the local currency (EUR, JPY, GBP, etc.).

- FX return is the change in the exchange rate in USD terms (how much that foreign currency strengthened/weakened versus USD).

This isn’t about finding the “right” number to the decimal. It’s about answering a different question:

“Was this month mostly an asset story, mostly an FX story, or both?”

That single shift reduces panic because it replaces narrative (“I’m losing because global investing doesn’t work”) with diagnosis (“FX headwind masked asset gains”).

A one-minute decomposition habit that reduces panic

Most people look at one number: USD performance.

Instead, keep a simple “two-line log”:

- Asset: What did the underlying market do (in local terms)?

- FX: Did the foreign currency strengthen or weaken versus USD?

- Action: Did I follow my rulebook this month?

That’s it. You don’t need to predict next month. You need to explain this month.

Table 1) Read your USD result without guessing the future

| What you see in USD | What often happened | Why your emotions spike | The operating conclusion |

|---|---|---|---|

| USD up, feels “too easy” | Asset flat/down, FX helped | “Did I get lucky? Should I add more?” | Keep contributions rule-based; don’t chase good FX months |

| USD down, but local market was fine | Asset up, FX headwind | “Global is broken / USD is too strong” | Treat as FX noise; avoid pause-by-forecast |

| USD down, local market also down | Double headwind | “This is failing” | This is where consistency matters most; rely on buffers + triggers |

| USD up, local market also up | Double tailwind | “I should accelerate” | Guard against overconfidence; stick to planned step-ups only |

Interpretation (2–3 lines):

- The same USD outcome can come from completely different drivers, so reacting to “USD return” alone invites rule drift.

- When FX is the main driver, your plan usually shouldn’t change—because FX is hard to forecast and easy to overreact to.

- The goal is not to remove volatility; it’s to keep volatility from changing your behavior.

Misconception that breaks global DCA: “I should pause until the dollar weakens”

Why it’s wrong: pausing requires a forecast (“when will FX reverse?”). Forecasting turns DCA into a timing strategy—and timing strategies usually fail because they’re hard to execute consistently. You often end up pausing during the exact months you needed consistency most.

Check instead (2 lines): (1) Only pause for cash-flow reasons (job loss, emergency buffer breached), not for FX opinions. (2) Use allocation drift triggers for rebalancing; never use “FX feels expensive/cheap.”

Your operating plan: contribution rules that survive FX volatility

A global DCA plan succeeds when it’s operated, not “hoped.”

Here’s a practical rulebook that avoids panic and prevents “just this month” exceptions:

- Contribution rule (the default)

- Contributions happen on schedule (paycheck-based or calendar-based), regardless of FX headlines.

- Pause rule (the exception)

- Pauses are allowed only if your cash-flow buffer is threatened (emergency fund below your minimum, unexpected medical bill, income disruption).

- Pauses are not allowed because “USD is strong” or “currency feels wrong.”

- Step-up rule (planned growth)

- Increase contributions using a pre-set policy (e.g., when income rises or once per year during financial review).

- Never step up because a currency move “feels like an opportunity.”

- Rebalancing rule (drift-based)

- Rebalance when your target allocation drifts beyond a threshold (e.g., 5–10% relative drift or a fixed band).

- Rebalance does not require a currency view; it’s a mechanical risk-control tool.

- Behavior rule (the real edge)

- You don’t “win” global DCA by being right about FX.

- You win by staying consistent while others pause and chase.

Checklist 1) A “no-panic” DCA setup you can finish today

- □ My contribution date is automated (payday + 24 hours, or a fixed monthly day)

- □ I have a written pause rule: “Only for cash-flow emergencies, never for FX opinions”

- □ I track monthly notes in three lines: Asset / FX / Did I follow the rulebook?

- □ My step-up policy is scheduled (annual review), not emotional (market-driven)

- □ I have a drift threshold for rebalancing (so I’m not improvising under stress)

Midpoint stress-test: find which assumption breaks your plan first

Once you adopt decomposition, the next upgrade is to identify what your plan is actually sensitive to:

- returns,

- inflation,

- fees/taxes (conceptually),

- contribution size and growth,

- and how long you can stay consistent.

This is where the calculator turns anxiety into clarity.

Use ETF/Stock DCA Simulator to input starting amount and monthly contribution, then set a base annual return and inflation assumption.

Next, add fees and any tax/drag assumptions conceptually, plus an optional contribution growth rate if you plan to increase contributions over time.

Internal reads that fit here (midpoint 1–2 links):

- Use CAGR to avoid “average return” illusions (so your assumptions stay realistic)

- DCA fails more from consistency than math—here are 7 repeatable failure patterns

A scenario playbook: what to do in three common regimes

Decomposition is interpretation. A playbook is execution.

The simplest way to avoid rule drift is to pre-write your actions for the regimes you’ll inevitably face.

Table 2) Three regimes, observable triggers, and the default action

| Regime | What’s happening | Observable trigger (not feelings) | Default action |

|---|---|---|---|

| Base regime | Normal volatility | Contributions are affordable; allocation drift stays within band | Keep contributions steady; log Asset/FX monthly |

| FX shock regime | USD swings vs foreign currency | Your USD return diverges sharply from local market performance | Do not pause by forecast; keep schedule; rebalance only by drift |

| Asset selloff regime | The underlying market drops | Drawdown exceeds your comfort range; headlines intensify | Use pause rule only if buffer breaks; consider drift-based rebalance if planned |

Interpretation (2–3 lines):

- The playbook uses triggers you can observe (allocation drift, buffer levels), not predictions you can’t control.

- FX shock regimes are where most people pause; the plan’s job is to prevent that default mistake.

- Asset selloffs are where consistency matters most; your pause rule should protect your life, not your emotions.

Two case studies: same USD outcome, totally different meaning

These are simplified examples. The purpose is not precision—it’s learning to separate drivers.

Case study 1) USD result is flat, but the asset did great

- You buy a foreign market exposure. In local terms, the market is +10%.

- Over the same period, that currency weakens −9% versus USD.

- Approx USD return: (1.10 × 0.91) − 1 ≈ +0.1% (basically flat)

What many people feel: “Global didn’t work.”

What actually happened: the asset worked, FX offset it.

Operating takeaway: don’t punish the plan for FX noise. If your rulebook is consistent, this is just a normal outcome of global exposure.

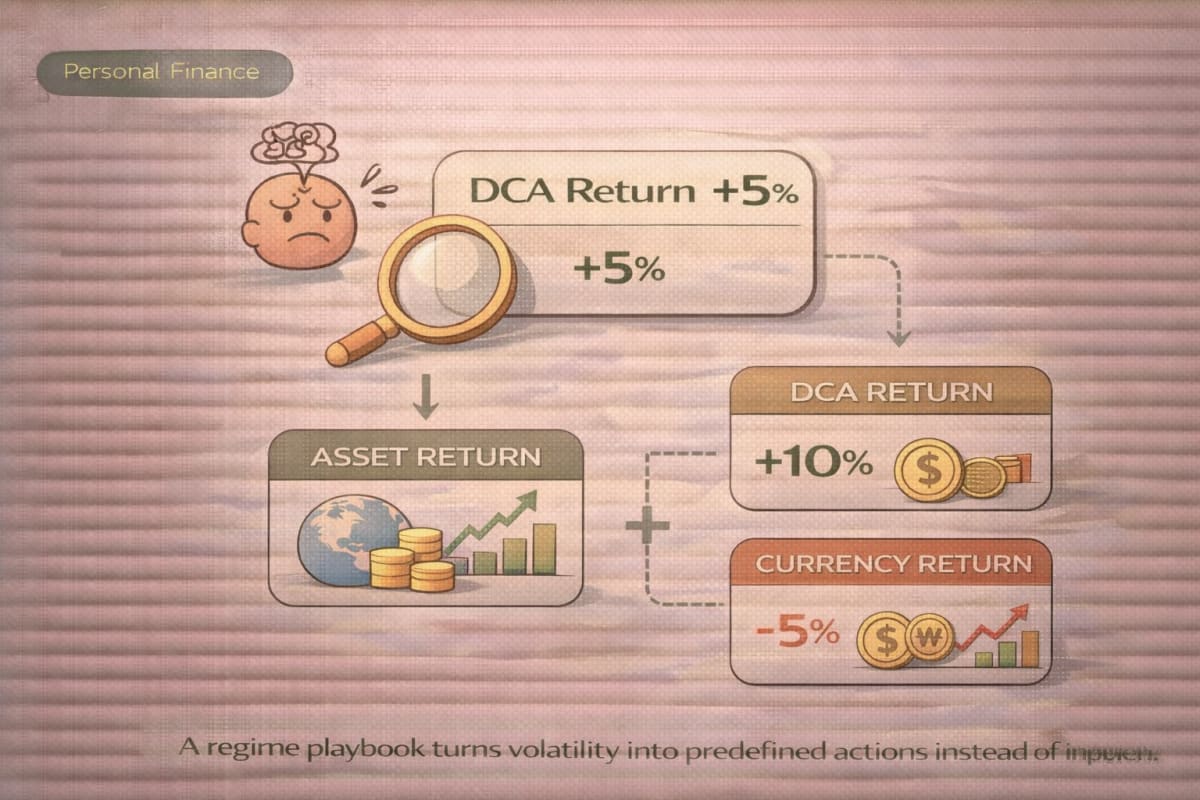

Case study 2) USD result is positive, but the asset struggled

- Local asset return is −6%.

- The foreign currency strengthens +10% versus USD.

- Approx USD return: (0.94 × 1.10) − 1 ≈ +3.4%

What many people feel: “My global exposure is great—let’s accelerate.”

What actually happened: FX tailwind masked weak asset performance.

Operating takeaway: don’t chase FX-driven wins. Step-ups should be scheduled, not reactive.

Rebalancing without FX opinions: drift rules beat narratives

Rebalancing becomes dangerous when it’s driven by “stories”:

- “USD is too strong.”

- “This currency looks cheap.”

- “I’ll wait for a better FX entry.”

Those statements are forecasts. Forecasts are fragile under stress.

Instead, rebalancing should be a risk-control mechanic that uses allocation drift:

Table 3) A rules library that prevents panic and rule-drift

| Situation | Don’t do this | Do this instead | Trigger you can measure | Review timing |

|---|---|---|---|---|

| FX moves sharply | Pause contributions “until it settles” | Keep schedule; log Asset/FX | Contribution affordability unchanged | Monthly (2 minutes) |

| USD return looks “too good” | Over-allocate impulsively | Follow planned step-up policy only | Annual review date arrives | Annual |

| Market drawdown hits | Panic sell or stop DCA | Use buffer rule; rebalance only by drift | Emergency buffer breached OR drift threshold hit | Quarterly |

| You feel confusion | Make a new rule mid-stress | Use the playbook; write one sentence | “I can’t explain this month in 3 lines” | Monthly |

Interpretation (2–3 lines):

- The rule library is designed to reduce “in-the-moment invention,” which is where most bad decisions happen.

- Your best global DCA edge is not finding the perfect FX moment—it’s keeping your plan intact when volatility tries to rewrite it.

- Drift-based triggers preserve consistency because they don’t depend on being right about the next move.

Taxes and accounts (US framing, high-level)

This article is not tax advice, but the operating reality is simple:

- In employer plans and tax-advantaged accounts (like 401(k) / IRA), automation is easier—and automation protects consistency.

- In taxable accounts, rebalancing and selling can create tax consequences; that’s another reason to rely on contribution routing and drift thresholds rather than frequent tinkering.

- For global exposure, you may see differences in distributions and foreign withholding; treat “tax drag” as an assumption to stress-test rather than a surprise.

The key: build a plan that survives after-tax reality without needing perfect markets.

Near the end: run a “break test” so your rules match your real life

A decomposition framework lowers panic, but a stress-test prevents unrealistic optimism.

Here’s a simple break test:

- Set a base scenario you believe you can stick to.

- Make it worse on purpose (lower returns, higher inflation, higher fees/drag, slower contribution growth).

- Ask: “Do my rules still work? Does my contribution size still feel survivable?”

Open ETF/Stock DCA Simulator and enter starting balance, monthly contribution, expected return, and inflation to create your base plan.

Then run sensitivity checks by changing return / inflation / fees (and optional tax drag) / contribution growth rate to see what variable breaks your plan first.

A simple action plan: 15 minutes, 60 minutes, 1 week

In 15 minutes

- Write your pause rule (cash-flow only), pick one contribution date, and start the 3-line monthly log.

In 60 minutes

- Define your target allocation and drift threshold; write your regime playbook (Base / FX shock / Selloff).

In 1 week

- Stress-test assumptions using the calculator and adjust contribution size or buffer targets until the plan feels survivable under conservative inputs.

Reads that make this framework stick

- Build the foundation first: budget + emergency fund + long-term investing (the “order of operations”)

- Size your emergency fund by risk (not a generic months number)

- Inflation-proof your household plan: cut fixed costs and protect cash flow

- Debt vs investing: a rule-based threshold approach that reduces anxiety

FAQ

1) What does “asset return + currency return” mean in practice?

It means your USD outcome reflects both the underlying market’s movement and the exchange-rate movement between USD and the foreign currency. When you separate those drivers, you can interpret results without turning every month into a “should I pause?” decision.

2) If FX adds volatility, shouldn’t I avoid global exposure altogether?

Not necessarily. FX volatility is a feature of global exposure, but volatility alone is not the decision variable—behavior is. The practical approach is to operate with rules that prevent panic and keep contributions consistent.

3) Should I pause DCA when the dollar is strong?

Pausing requires a forecast about when the dollar will weaken. That forecast-driven behavior is exactly what DCA is meant to avoid. A safer rule is: pause only when cash flow requires it (buffer breached), not when FX headlines feel uncomfortable.

4) Do I need to track local-currency returns to do this decomposition?

You don’t need perfect tracking. Even a simple monthly note—“local market up/down; currency up/down”—helps you avoid overreacting to a single USD number. The goal is clarity, not precision.

5) How often should I rebalance global allocations?

A common approach is to review on a schedule (quarterly or semiannually) and act only when allocation drift exceeds a threshold. The key is to rebalance by drift rules—not by currency opinions.

6) What’s the biggest behavioral risk in global DCA?

Rule drift: pausing “just this month,” chasing FX-driven wins, or inventing new rules mid-stress. A written playbook and a strict pause rule are the most effective protections.

7) How do inflation and fees interact with global DCA planning?

Inflation affects your real purchasing power, while fees (and any tax drag) reduce compounding. If your plan only works under optimistic assumptions, it will break psychologically even if it “works” mathematically.

8) How do I use the DCA calculator without overfitting assumptions?

Use it to test robustness, not to predict. Run a base case, then deliberately make it worse (lower returns, higher inflation, higher fees, slower contribution growth). If your plan survives conservative inputs, it’s more likely to survive real life.