- “DCA vs lump sum” is rarely decided by math alone; it’s decided by whether you can stay invested through regret, volatility, and life expenses.

- Lump sum can be rational when your cash buffer and time horizon are strong—but it can fail fast if a drawdown triggers panic selling or “wait to re-enter” paralysis.

- DCA doesn’t magically boost returns; it often boosts survival and consistency by reducing timing regret and keeping your plan alive.

- The right question is not “which wins on average,” but “which has the lowest chance of plan failure for me.”

- Use a 3-step rule: Survival (buffer + debt) → Consistency (income + behavior) → Optimization (hybrid schedule).

- In real households, the biggest risk is not market variance; it’s forced changes—medical bills, layoffs, big repairs, and debt APR shocks.

- Taxes and fees are not footnotes; they are friction that compounds, especially when you change strategies frequently.

- A hybrid (some now, some scheduled) often beats both extremes because it reduces regret without turning the process into market timing.

- If you can’t write your rule in one paragraph, you don’t have a rule—you have a mood.

- Run the same decision through DCA simulator with “bad early years” assumptions to see whether your plan breaks before it wins.

PERSONAL FINANCE · DECISION RULES

“Everyone says lump sum is better… so should I just do it?”

That question can backfire because the real enemy is not an imperfect expected return—it’s regret, pauses, and rule drift when life and volatility hit at the same time.

This guide replaces debate with a 3-step decision rule you can follow: survival → consistency → optimization.

- A decision table (conditions → choice → failure signal) that minimizes failure risk

- Two real scenarios: a windfall and paycheck-based investing

- A stress-test workflow using DCA simulator (no forecasting required)

Scope/limits: No stock/ETF picks and no market predictions. This is about choosing a contribution method you can actually keep.

Most DCA vs lump sum content tries to “win the argument.” Real households need something else: a rule that survives drawdowns, bills, and emotions.

A clean way to think about this is: your outcome is not just the market return you could have earned. It’s the market return you actually captured after interruptions, taxes/fees, and decisions made under stress.

So instead of asking, “Which has the higher expected value?” we’ll ask:

- Which choice is least likely to trigger regret selling?

- Which choice is least likely to force a contribution pause at the worst time?

- Which choice prevents strategy drift (constantly changing the plan)?

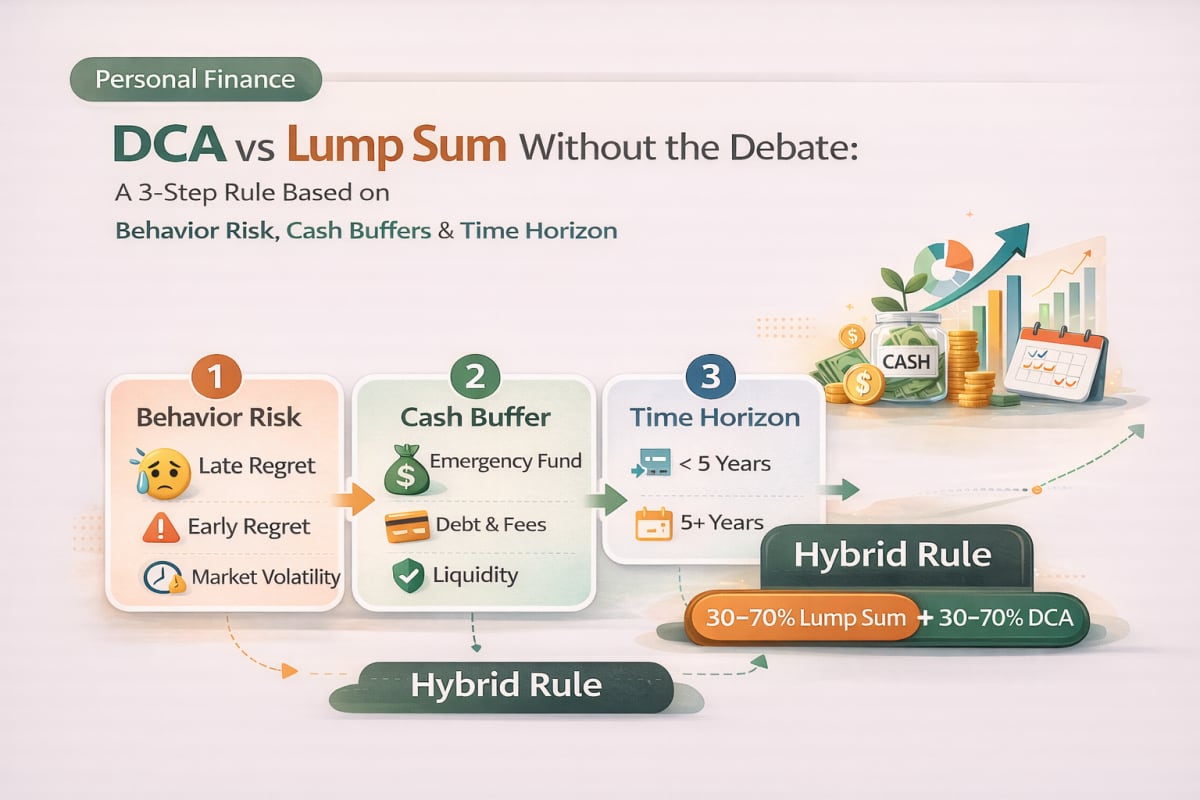

The hidden variable is “behavior risk,” not expected return

Behavior risk is the chance that your plan changes under stress. In practice, it shows up as three repeatable failure patterns:

- Regret: “I put it in right before a drop” (or “I waited and missed the run”)

- Pauses: “I’ll stop contributions for a bit” → the “bit” becomes months

- Rule drift: “I’ll switch methods” → switching repeats, compounding resets

Here is the important reframing: DCA and lump sum are not “better” or “worse” in the abstract. They are tools that reduce different failure modes.

Table 1) What each method protects you from (and what it doesn’t)

| Method | What it reduces | What it can increase | Typical failure pattern |

|---|---|---|---|

| DCA (scheduled contributions) | Timing regret, decision fatigue | “I’ll pause this month” temptation | A pause becomes a habit |

| Lump sum (all at once) | Ongoing contribution discipline needs | Drawdown shock and re-entry paralysis | Sell/stop after a drop, then wait |

| Hybrid (some now + scheduled remainder) | Timing regret and paralysis | Complexity if rules are vague | “Adjusting the schedule” turns into timing |

Interpretation:

- DCA often wins in real life because it improves consistency, not because it raises expected returns.

- Lump sum often wins when you can truly hold through drawdowns without touching the plan.

- Hybrid is powerful when you write the rule once and then stop editing it.

A 3-step rule that minimizes failure risk

This rule is intentionally boring. Boring is good because boring survives.

Step 1) Survival: cash buffer + debt APR

Step 2) Consistency: income stability + behavior tolerance

Step 3) Optimization: choose DCA vs hybrid vs lump sum schedule

You do not “earn the right” to optimize until survival and consistency are solid.

To build Step 1 and Step 2 correctly, it helps to know your household foundation order:

And if your emergency fund target still feels fuzzy:

The required decision table: condition → choice → failure signal

Use this table like a filter. You’re not trying to find the “highest expected return.” You’re trying to avoid the choice that is most likely to break your plan.

Assume you’re choosing between DCA, hybrid, and lump sum for money intended for long-term investing (not near-term spending).

Table 2) Decision table (minimize failure risk)

| Condition (be honest) | Choice (DCA / hybrid / lump sum) | Failure signal (if this appears, change method) |

|---|---|---|

| Cash buffer is thin (you’d struggle with a $2,000–$5,000 surprise) | DCA or hybrid | You start using credit cards for basics or skip bills to invest |

| Cash buffer is strong (you can absorb a few months of higher expenses) | Hybrid or lump sum | A drawdown makes you want to sell or “wait to re-enter” |

| Debt APR is high (credit card APR range, or any debt that stresses cash flow) | DCA (smaller) + prioritize debt rule | You miss contributions for 2–3 straight months due to payments |

| Time horizon is long (10+ years) | Hybrid or lump sum (if behavior tolerance is high) | You check daily and change the plan more than quarterly |

| Time horizon is medium (3–7 years) | DCA or hybrid (more cautious) | You realize you might need the money earlier than planned |

| Income is stable (salary, predictable expenses) | DCA baseline + optional hybrid | You pause “temporarily” during mild volatility |

| Income is variable (commission, freelance, business cycles) | DCA minimum + “surplus-month” hybrid | Your contribution drops to zero and never restarts |

| Behavior tolerance is low (you panic at a -20% headline) | DCA or hybrid | You sell during drawdown or keep moving the schedule |

| Behavior tolerance is high (you can hold through deep drawdowns) | Hybrid or lump sum | You delay investing for months waiting for a “better entry” |

Interpretation:

- This table is not a ranking of returns. It’s a ranking of failure probability.

- A “failure signal” means your method is pushing you into behavior that destroys compounding.

- The best method is the one that keeps you invested and contributing without drama.

The misconception that fuels endless debate (and how to fix it)

Misconception A: “Lump sum is always best.”

This can be true in some long-run averages, but it assumes you actually hold through drawdowns and do not freeze on re-entry. If a lump sum makes you panic-sell or delay re-investing after a drop, the theoretical edge disappears in real life.

Misconception B: “DCA boosts returns.”

DCA often improves consistency and reduces regret, but it does not magically raise expected return. In rising markets, money invested earlier has more time to grow; DCA can trade some expected return for a higher chance of staying invested.

Instead, check this:

1) Which method has the lowest chance of triggering a pause or a sell for me?

2) Which method fits my cash buffer and debt APR without stress?

Case study 1: A windfall (bonus, inheritance, sale proceeds)

Scenario:

- You receive a $30,000 bonus.

- Your fixed expenses are $4,000/month (rent or mortgage, utilities, insurance, groceries, childcare).

- You have $8,000 in cash savings.

- You also carry some debt with a meaningful APR (even if it’s “manageable”).

This is where people make the biggest mistake: treating a one-time windfall like it has no impact on survival. In reality, a windfall can tempt you into investing too aggressively while your buffer remains fragile.

A rules-based approach looks like this:

Stabilize survival first

- Decide what “enough buffer” means for your risk profile (job stability, dependents, fixed costs).

- If your buffer is thin, a full lump sum is a high failure-risk move.

Run a debt APR threshold rule

- Some debt behaves like a “risk-free return” when you pay it down.

- The point is not maximizing returns; it’s reducing stress-driven plan breaks.

- Use a conceptual framework like:

Compare debt payoff vs investing with a simple threshold rule

Then choose hybrid by default

A common hybrid structure (not a prescription) is:- Invest a portion now to reduce “I missed it” regret

- Schedule the remainder over 6–12 months to reduce “I bought the top” regret

- Lock the schedule date and do not edit it in response to news

Why hybrid works here:

- It lowers both types of regret (late regret and early regret).

- It turns your decision into a calendar, not a mood.

Case study 2: Paycheck-based investing (the “real” DCA use case)

Scenario:

- You invest $500/month from a paycheck.

- Your income is stable but not unlimited.

- Your risk is not “missing a perfect entry.” Your risk is breaking the plan when expenses spike.

This is the DCA environment. The question becomes: how do you keep contributions consistent without relying on willpower?

A practical rule set:

- Base contribution: the amount you can keep even in a bad month

- Minimum contribution: a smaller “never zero” amount for stressful months

- Step-up rule: raise contributions only when cash flow has improved for multiple months

- Pause rule: define what qualifies as a pause (and define the restart trigger)

A common failure pattern is “I’ll pause for one month.” The fix is “never zero unless truly necessary.”

If you want a full rulebook for increasing or pausing contributions without breaking your plan:

Use the DCA calculator to stress-test failure risk (mid-article)

At this point you should have a candidate method: DCA, hybrid, or lump sum. Now you test whether it breaks under realistic stress.

What this validates: compare DCA vs hybrid vs “as-if lump sum” assumptions by adding bad early years and pause periods to see which plan is most likely to break. Open: DCA simulator

What to input: starting balance (windfall or current), monthly contribution (if any), timeline, return assumption (conservative/base), inflation (optional), and fees/taxes as friction (conceptual). Then test pauses (0/3/6 months).

Why this matters:

- Many plans look fine with smooth average returns.

- Most real failures happen when returns are ugly early or expenses spike.

- A plan that survives the ugly path is often “better” than a plan that wins on average but breaks on contact.

A simple hybrid blueprint that avoids market timing

Hybrid is not “half now, half later” by vibe. It’s a schedule you commit to.

Here are three hybrid templates you can actually keep. They are frameworks, not recommendations:

- Calendar split: invest 20–40% now, then invest the rest monthly for 6–12 months.

- Drawdown guardrail: invest a base amount now; schedule the rest; if markets drop sharply, you do not “double down” unless it was pre-written.

- Income-aligned: invest a chunk now; then merge the remainder into your paycheck-based DCA system.

The rule that prevents timing games:

- Choose the schedule before you look at the news.

- Change it only on a preset cadence (quarterly, not daily).

Checklists: choose once, then protect the plan

Checklist 1) Pick the method (10 minutes)

- □ I can cover a $2,000–$5,000 surprise without debt stress (cash buffer check).

- □ I know which debt APR levels cause cash-flow anxiety (debt check).

- □ My time horizon is written down (3–7 years vs 10+ years).

- □ My income is stable or variable—and my rule matches it (income check).

- □ I know how I react to a -20% headline (behavior check).

- □ I picked DCA / hybrid / lump sum based on failure risk, not on debate.

Checklist 2) Keep the method (monthly)

- □ Contributions are automated and occur right after payday (system beats willpower).

- □ I have a “minimum contribution” for stressful months (never zero by default).

- □ I only change the plan on a preset cadence (quarterly review).

- □ Fees/taxes are treated as friction, not ignored (conceptual but consistent).

- □ If I pause, I have a restart trigger (date or cash buffer threshold).

Near the end: run the same stress test again (the “final sanity check”)

Before you lock your method, run one more check with worse assumptions than you want to believe. You’re not forecasting; you’re testing plan integrity.

What this validates: whether your chosen method still survives when you assume a rough first year, a temporary pause, and a lower return—so you minimize failure risk. Open: DCA simulator

What to input: same baseline as before, then lower the return, add fees/taxes as friction (conceptual), and test pause lengths. If the plan breaks, downgrade to the method you can keep.

If you want one extra safety layer, calibrate your “expected return” thinking so you don’t build a fragile plan around optimism:

Continue with these next pieces (to make the rulebook complete)

- Turn “I should invest more” into a monthly number you can actually commit to

- Use a $500/month for 10 years example as a DCA baseline

- Speed up goals by adjusting the right variable (principal vs return vs time)

- If you invest globally, separate asset return vs currency return to prevent panic pauses

FAQs

1) Is lump sum always better than DCA?

Not always. Lump sum can be favored in some long-run averages, but it assumes you hold through drawdowns and don’t freeze on re-entry. If lump sum increases your chance of selling or delaying re-investment after a drop, it can be worse in practice.

2) Does DCA increase returns?

Not reliably. DCA often trades some theoretical edge for a higher chance of staying invested and avoiding regret-driven decisions. Its main value is often plan survival, not return enhancement.

3) What is the simplest way to choose between DCA and lump sum?

Use the decision table: cash buffer, debt APR stress, time horizon, income stability, and behavior tolerance. Choose the method that minimizes your probability of pausing or selling. Then stress-test the choice in DCA simulator.

4) When does hybrid make the most sense?

Hybrid is most useful when you have a windfall and you want to reduce both “I missed it” regret and “I bought the top” regret. It works only when the schedule is written and fixed ahead of time. If you keep editing the schedule, hybrid becomes timing.

5) How do debt and investing interact in this decision?

High-APR debt can behave like a “guaranteed return” when paid down, and it can increase the chance your investing plan breaks due to cash-flow stress. You don’t need perfect math; you need a rule that prevents missed payments, forced selling, or chronic pauses.

6) What should I assume for fees and taxes?

Treat them as friction rather than trying to optimize them perfectly. The key is to be consistent and conservative so your plan is robust. Avoid frequent strategy switching that can increase friction and rule drift.

7) What if my income is variable?

Build a two-tier contribution rule: a minimum contribution you can keep in lean months, and a surplus-month add-on when cash flow is strong. Variable income plans fail when contributions drop to zero and never restart. A restart trigger matters as much as the contribution.

8) How often should I revisit the method?

Quarterly is usually enough for method changes; monthly is enough for checking whether you kept contributions and stayed within your cash buffer rules. Daily reviews tend to increase rule drift. A plan that changes constantly is rarely a plan that compounds.